- India

- /

- Healthcare Services

- /

- NSEI:LOTUSEYE

Lotus Eye Hospital and Institute Limited (NSE:LOTUSEYE) P/E Isn't Throwing Up Surprises

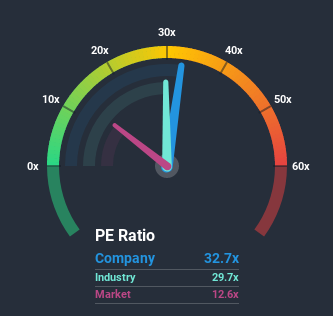

When close to half the companies in India have price-to-earnings ratios (or "P/E's") below 12x, you may consider Lotus Eye Hospital and Institute Limited (NSE:LOTUSEYE) as a stock to avoid entirely with its 32.7x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Lotus Eye Hospital and Institute certainly has been doing a great job lately as it's been growing earnings at a really rapid pace. It seems that many are expecting the strong earnings performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Lotus Eye Hospital and Institute

Does Lotus Eye Hospital and Institute Have A Relatively High Or Low P/E For Its Industry?

An inspection of average P/E's throughout Lotus Eye Hospital and Institute's industry may help to explain its particularly high P/E ratio. The image below shows that the Healthcare industry as a whole also has a P/E ratio significantly higher than the market. So we'd say there is merit in the premise that the company's ratio being shaped by its industry at this time. Some industry P/E's don't move around a lot and right now most companies within the Healthcare industry should be getting a strong boost. Ultimately though, it's going to be the fundamentals of the business like earnings and growth that count most.

Is There Enough Growth For Lotus Eye Hospital and Institute?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Lotus Eye Hospital and Institute's to be considered reasonable.

If we review the last year of earnings growth, the company posted a terrific increase of 211%. The latest three year period has also seen an excellent 199% overall rise in EPS, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing earnings over that time.

Weighing the recent medium-term upward earnings trajectory against the broader market's one-year forecast for contraction of 6.7% shows it's a great look while it lasts.

With this information, we can see why Lotus Eye Hospital and Institute is trading at a high P/E compared to the market. Investors are willing to pay more for a stock they hope will buck the trend of the broader market going backwards. However, its current earnings trajectory will be very difficult to maintain against the headwinds other companies are facing at the moment.

The Bottom Line On Lotus Eye Hospital and Institute's P/E

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Lotus Eye Hospital and Institute maintains its high P/E on the strength of its recentthree-year growth beating forecasts for a struggling market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident earnings aren't under threat. Our only concern is whether its earnings trajectory can keep outperforming under these tough market conditions. Otherwise, it's hard to see the share price falling strongly in the near future if its earnings performance persists.

Before you settle on your opinion, we've discovered 2 warning signs for Lotus Eye Hospital and Institute (1 shouldn't be ignored!) that you should be aware of.

If you're unsure about the strength of Lotus Eye Hospital and Institute's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

When trading Lotus Eye Hospital and Institute or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account.Promoted

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:LOTUSEYE

Lotus Eye Hospital and Institute

A specialty eye care hospital, provides eye care and related services in India.

Flawless balance sheet with questionable track record.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)