Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:PSK

Is PrairieSky Royalty Ltd.'s (TSE:PSK) CEO Overpaid Relative To Its Peers?

In 2014, Andrew Phillips was appointed CEO of PrairieSky Royalty Ltd. (TSE:PSK). This report will, first, examine the CEO compensation levels in comparison to CEO compensation at companies of similar size. After that, we will consider the growth in the business. Third, we'll reflect on the total return to shareholders over three years, as a second measure of business performance. The aim of all this is to consider the appropriateness of CEO pay levels.

Check out our latest analysis for PrairieSky Royalty

How Does Andrew Phillips's Compensation Compare With Similar Sized Companies?

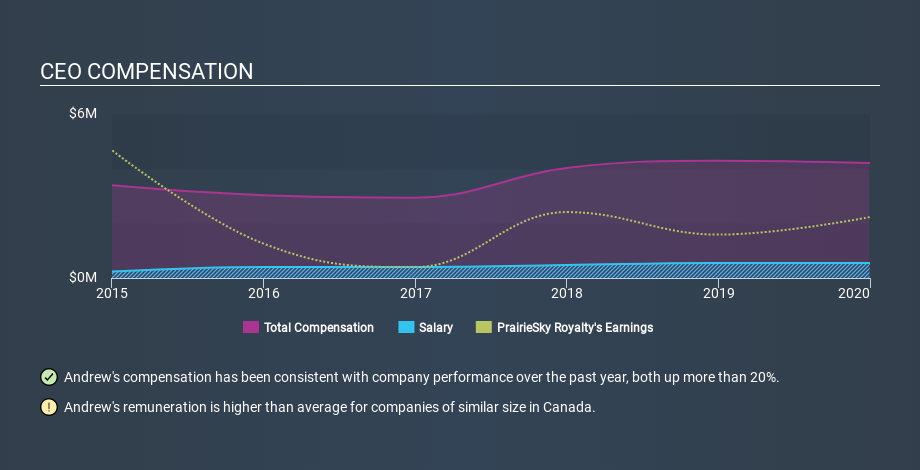

Our data indicates that PrairieSky Royalty Ltd. is worth CA$2.3b, and total annual CEO compensation was reported as CA$4.2m for the year to December 2019. That's actually a decrease on the year before. While this analysis focuses on total compensation, it's worth noting the salary is lower, valued at CA$550k. We further remind readers that the CEO may face performance requirements to receive the non-salary part of the total compensation. When we examined a selection of companies with market caps ranging from CA$1.3b to CA$4.3b, we found the median CEO total compensation was CA$2.9m.

Pay mix tells us a lot about how a company functions versus the wider industry, and it's no different in the case of PrairieSky Royalty. Talking in terms of the sector, salary represented approximately 55% of total compensation out of all the companies we analysed, while other remuneration made up 45% of the pie. It's interesting to note that PrairieSky Royalty allocates a smaller portion of compensation to salary in comparison to the broader industry.

Thus we can conclude that Andrew Phillips receives more in total compensation than the median of a group of companies in the same market, and of similar size to PrairieSky Royalty Ltd.. However, this doesn't necessarily mean the pay is too high. We can get a better idea of how generous the pay is by looking at the performance of the underlying business. You can see a visual representation of the CEO compensation at PrairieSky Royalty, below.

Is PrairieSky Royalty Ltd. Growing?

Over the last three years PrairieSky Royalty Ltd. has seen earnings per share (EPS) move in a positive direction by an average of 7.1% per year (using a line of best fit). In the last year, its revenue is down 9.5%.

I would argue that the lack of revenue growth in the last year is less than ideal, but it is good to see EPS growth. These two metric are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. Shareholders might be interested in this free visualization of analyst forecasts.

Has PrairieSky Royalty Ltd. Been A Good Investment?

Given the total loss of 63% over three years, many shareholders in PrairieSky Royalty Ltd. are probably rather dissatisfied, to say the least. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

We compared total CEO remuneration at PrairieSky Royalty Ltd. with the amount paid at companies with a similar market capitalization. As discussed above, we discovered that the company pays more than the median of that group.

The growth in the business has been uninspiring, but the shareholder returns have arguably been worse, over the last three years. Shareholders may wish to consider further research. Although we don't think the CEO pay is too high, it is probably more on the generous side of things. CEO compensation is an important area to keep your eyes on, but we've also identified 3 warning signs for PrairieSky Royalty (2 are a bit concerning!) that you should be aware of before investing here.

If you want to buy a stock that is better than PrairieSky Royalty, this free list of high return, low debt companies is a great place to look.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About TSX:PSK

PrairieSky Royalty

PrairieSky Royalty Ltd. holds crude oil and natural gas royalty interests in Canada.

Good value with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor