Advertisement

- India

- /

- Basic Materials

- /

- NSEI:ORIENTALTL

Is Oriental Trimex (NSE:ORIENTALTL) Using Too Much Debt?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Oriental Trimex Limited (NSE:ORIENTALTL) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Oriental Trimex

What Is Oriental Trimex's Net Debt?

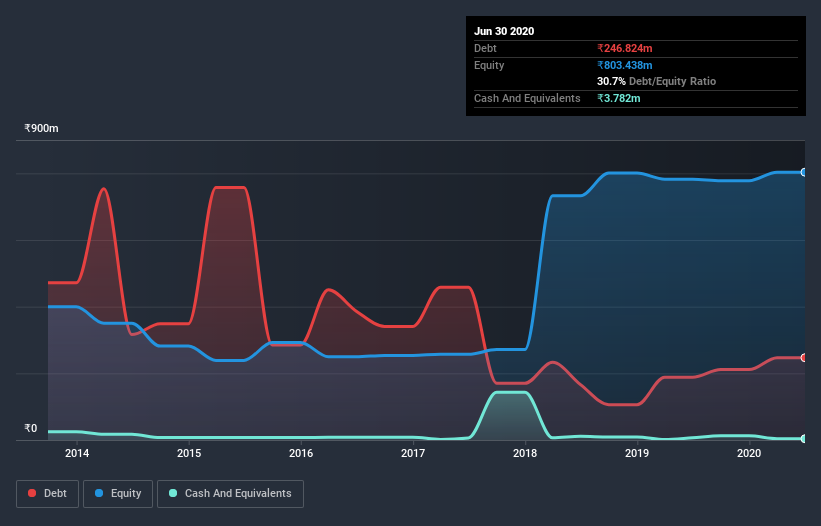

As you can see below, at the end of March 2020, Oriental Trimex had ₹246.8m of debt, up from ₹188.1m a year ago. Click the image for more detail. Net debt is about the same, since the it doesn't have much cash.

A Look At Oriental Trimex's Liabilities

According to the last reported balance sheet, Oriental Trimex had liabilities of ₹394.8m due within 12 months, and liabilities of ₹185.5m due beyond 12 months. On the other hand, it had cash of ₹3.78m and ₹403.4m worth of receivables due within a year. So its liabilities total ₹173.1m more than the combination of its cash and short-term receivables.

Oriental Trimex has a market capitalization of ₹325.6m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While Oriental Trimex's debt to EBITDA ratio (3.2) suggests that it uses some debt, its interest cover is very weak, at 1.2, suggesting high leverage. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. The good news is that Oriental Trimex grew its EBIT a smooth 97% over the last twelve months. Like a mother's loving embrace of a newborn that sort of growth builds resilience, putting the company in a stronger position to manage its debt. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Oriental Trimex will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. During the last three years, Oriental Trimex burned a lot of cash. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

To be frank both Oriental Trimex's interest cover and its track record of converting EBIT to free cash flow make us rather uncomfortable with its debt levels. But at least it's pretty decent at growing its EBIT; that's encouraging. Once we consider all the factors above, together, it seems to us that Oriental Trimex's debt is making it a bit risky. Some people like that sort of risk, but we're mindful of the potential pitfalls, so we'd probably prefer it carry less debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Oriental Trimex is showing 3 warning signs in our investment analysis , and 1 of those is potentially serious...

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

If you decide to trade Oriental Trimex, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:ORIENTALTL

Oriental Trimex

Engages in importing and processing of natural stones in India.

Excellent balance sheet with acceptable track record.

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Unicycive Therapeutics ·

Looking to be second time lucky with a game-changing new product

Fair Value:US$21.5369.5% undervalued

62 followersusers have followed this narrative

0 commentsusers have commented on this narrative

10 likesusers have liked this narrative

HE

HegelBayeBagel on PlaySide Studios ·

PlaySide Studios: Market Is Sleeping on a Potential 10M+ Unit Breakout Year, FY26 Could Be the Rerate of the Decade

Fair Value:AU$0.8460.7% undervalued

12 followersusers have followed this narrative

2 commentsusers have commented on this narrative

7 likesusers have liked this narrative

AN

AnimalDoctorKwon on Inotiv ·

Inotiv NAMs Test Center

Fair Value:US$1.276.8% undervalued

20 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

TH

TheValueDetector on Cognyte Software ·

This isn’t speculation — this is confirmation.A Schedule 13G was filed, not a 13D, meaning this is passive institutional capital, not acti

Fair Value:US$95.6793.4% undervalued

43 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

NA

Nat32 on NIKE ·

My long-term take on Nike: A global sports brand with steady growth potential but margin challenges to solve.

Fair Value:US$48.2730.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Manuka Resources ·

30 Baggers Silver Miner with Gold/VTM Optionality

Fair Value:AU$4.7997.2% undervalued

1 followerusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.887.7% undervalued

61 followersusers have followed this narrative

5 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59635.5% undervalued

1297 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

TA

Talos on Tesla ·

The "Physical AI" Monopoly – A New Industrial Revolution

Fair Value:US$665.3639.9% undervalued

49 followersusers have followed this narrative

19 commentsusers have commented on this narrative

22 likesusers have liked this narrative