Advertisement

- Australia

- /

- Consumer Services

- /

- ASX:GEM

Is It Time To Consider Buying G8 Education Limited (ASX:GEM)?

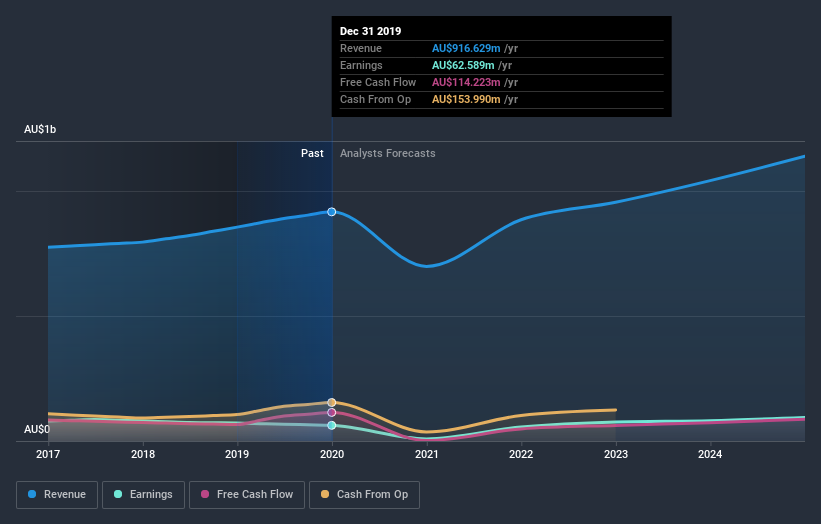

While G8 Education Limited (ASX:GEM) might not be the most widely known stock at the moment, it saw significant share price movement during recent months on the ASX, rising to highs of AU$1.12 and falling to the lows of AU$0.78. Some share price movements can give investors a better opportunity to enter into the stock, and potentially buy at a lower price. A question to answer is whether G8 Education's current trading price of AU$0.81 reflective of the actual value of the small-cap? Or is it currently undervalued, providing us with the opportunity to buy? Let’s take a look at G8 Education’s outlook and value based on the most recent financial data to see if there are any catalysts for a price change.

See our latest analysis for G8 Education

What is G8 Education worth?

Good news, investors! G8 Education is still a bargain right now according to my price multiple model, which compares the company's price-to-earnings ratio to the industry average. In this instance, I’ve used the price-to-earnings (PE) ratio given that there is not enough information to reliably forecast the stock’s cash flows. I find that G8 Education’s ratio of 5.89x is below its peer average of 13.48x, which indicates the stock is trading at a lower price compared to the Consumer Services industry. Although, there may be another chance to buy again in the future. This is because G8 Education’s beta (a measure of share price volatility) is high, meaning its price movements will be exaggerated relative to the rest of the market. If the market is bearish, the company’s shares will likely fall by more than the rest of the market, providing a prime buying opportunity.

What does the future of G8 Education look like?

Future outlook is an important aspect when you’re looking at buying a stock, especially if you are an investor looking for growth in your portfolio. Buying a great company with a robust outlook at a cheap price is always a good investment, so let’s also take a look at the company's future expectations. With profit expected to grow by 21% over the next couple of years, the future seems bright for G8 Education. It looks like higher cash flow is on the cards for the stock, which should feed into a higher share valuation.

What this means for you:

Are you a shareholder? Since GEM is currently below the industry PE ratio, it may be a great time to accumulate more of your holdings in the stock. With a positive outlook on the horizon, it seems like this growth has not yet been fully factored into the share price. However, there are also other factors such as capital structure to consider, which could explain the current price multiple.

Are you a potential investor? If you’ve been keeping an eye on GEM for a while, now might be the time to make a leap. Its buoyant future profit outlook isn’t fully reflected in the current share price yet, which means it’s not too late to buy GEM. But before you make any investment decisions, consider other factors such as the track record of its management team, in order to make a well-informed investment decision.

In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. Our analysis shows 4 warning signs for G8 Education (2 make us uncomfortable!) and we strongly recommend you look at these before investing.

If you are no longer interested in G8 Education, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

If you’re looking to trade G8 Education, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About ASX:GEM

G8 Education

Provides early childhood education and care services in Australia.

Undervalued with moderate growth potential.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.558.3% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.1% undervalued

54 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56053.2% undervalued

62 followersusers have followed this narrative

2 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.3% undervalued

32 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

AN

AntonioS on REA Group ·

Is REA Group a Good Value Opportunity?

Fair Value:AU$1489.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

John_Eric on ServiceNow ·

The Company Nobody Brags About

Fair Value:US$165.6943.4% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AntonioS on ASX ·

ASX Limited

Fair Value:AU$4320.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9638.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17060.0% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative