Advertisement

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. In light of that, when we looked at ILPRA (BIT:ILP) and its ROCE trend, we weren't exactly thrilled.

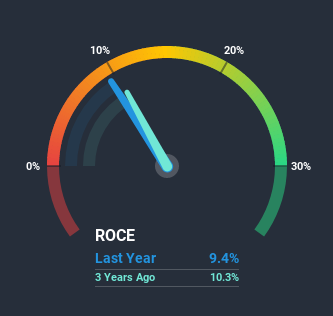

Return On Capital Employed (ROCE): What is it?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. Analysts use this formula to calculate it for ILPRA:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.094 = €2.3m ÷ (€42m - €17m) (Based on the trailing twelve months to December 2019).

Therefore, ILPRA has an ROCE of 9.4%. On its own that's a low return, but compared to the average of 6.1% generated by the Machinery industry, it's much better.

View our latest analysis for ILPRA

In the above chart we have a measured ILPRA's prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering ILPRA here for free.

What The Trend Of ROCE Can Tell Us

In terms of ILPRA's historical ROCE trend, it doesn't exactly demand attention. Over the past three years, ROCE has remained relatively flat at around 9.4% and the business has deployed 62% more capital into its operations. This poor ROCE doesn't inspire confidence right now, and with the increase in capital employed, it's evident that the business isn't deploying the funds into high return investments.

Another thing to note, ILPRA has a high ratio of current liabilities to total assets of 41%. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. While it's not necessarily a bad thing, it can be beneficial if this ratio is lower.What We Can Learn From ILPRA's ROCE

In conclusion, ILPRA has been investing more capital into the business, but returns on that capital haven't increased. And investors appear hesitant that the trends will pick up because the stock has fallen 11% in the last year. Therefore based on the analysis done in this article, we don't think ILPRA has the makings of a multi-bagger.

If you'd like to know more about ILPRA, we've spotted 4 warning signs, and 2 of them make us uncomfortable.

While ILPRA may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

If you decide to trade ILPRA, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account.Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About BIT:ILP

ILPRA

Engages in the design, production, and sale of packaging machines worldwide.

High growth potential and good value.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2542.9% undervalued

64 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$487.1% overvalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5446.8% undervalued

50 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$829.5% undervalued

25 followersusers have followed this narrative

2 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

YO

youwakeup on Strategy ·

MSTR Is a Leveraged Accumulator of Bitcoin

Fair Value:US$1.894.8k% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HM

Hmdlsk on Circus ·

Circus SE's AI-driven food systems will augment global food service

Fair Value:€3082.3% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BR

Bravosatya on Meta Platforms ·

Meta Platforms - Zuckerberg’s investment decisions are impulsive or Prudent?

Fair Value:US$730.0216.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75030.3% undervalued

80 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9634.1% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7441.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative