Advertisement

- United States

- /

- Biotech

- /

- NasdaqGS:GILD

Is Gilead Sciences, Inc. (NASDAQ:GILD) A Strong Dividend Stock?

Is Gilead Sciences, Inc. (NASDAQ:GILD) a good dividend stock? How can we tell? Dividend paying companies with growing earnings can be highly rewarding in the long term. If you are hoping to live on your dividends, it's important to be more stringent with your investments than the average punter. Regular readers know we like to apply the same approach to each dividend stock, and we hope you'll find our analysis useful.

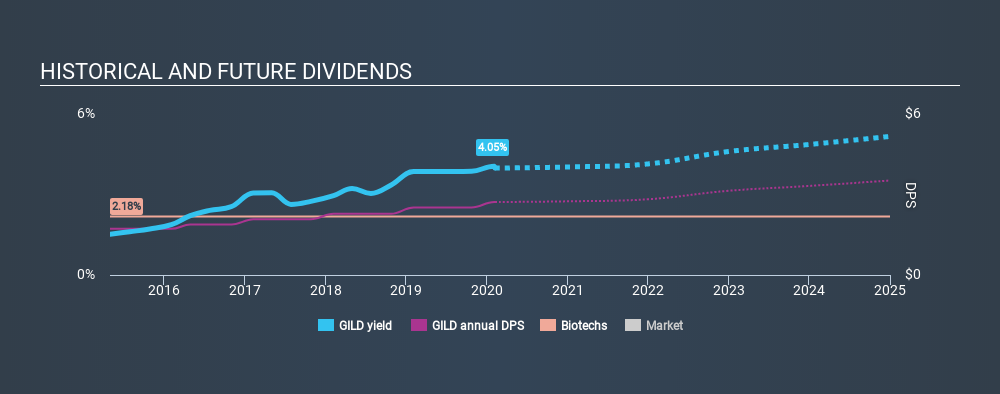

In this case, Gilead Sciences likely looks attractive to dividend investors, given its 4.0% dividend yield and five-year payment history. It sure looks interesting on these metrics - but there's always more to the story . The company also bought back stock during the year, equivalent to approximately 2.8% of the company's market capitalisation at the time. Some simple analysis can reduce the risk of holding Gilead Sciences for its dividend, and we'll focus on the most important aspects below.

Click the interactive chart for our full dividend analysis

Payout ratios

Companies (usually) pay dividends out of their earnings. If a company is paying more than it earns, the dividend might have to be cut. As a result, we should always investigate whether a company can afford its dividend, measured as a percentage of a company's net income after tax. Gilead Sciences paid out 59% of its profit as dividends, over the trailing twelve month period. A payout ratio above 50% generally implies a business is reaching maturity, although it is still possible to reinvest in the business or increase the dividend over time.

We update our data on Gilead Sciences every 24 hours, so you can always get our latest analysis of its financial health, here.

Dividend Volatility

Before buying a stock for its income, we want to see if the dividends have been stable in the past, and if the company has a track record of maintaining its dividend. Looking at the data, we can see that Gilead Sciences has been paying a dividend for the past five years. During the past five-year period, the first annual payment was US$1.72 in 2015, compared to US$2.72 last year. Dividends per share have grown at approximately 9.6% per year over this time.

Gilead Sciences has been growing its dividend at a decent rate, and the payments have been stable despite the short payment history. This is a positive start.

Dividend Growth Potential

While dividend payments have been relatively reliable, it would also be nice if earnings per share (EPS) were growing, as this is essential to maintaining the dividend's purchasing power over the long term. Gilead Sciences's EPS have fallen by approximately 12% per year during the past five years. A sharp decline in earnings per share is not great from from a dividend perspective, as even conservative payout ratios can come under pressure if earnings fall far enough.

Conclusion

To summarise, shareholders should always check that Gilead Sciences's dividends are affordable, that its dividend payments are relatively stable, and that it has decent prospects for growing its earnings and dividend. First, we think Gilead Sciences has an acceptable payout ratio. Second, earnings per share have been in decline, and the dividend history is shorter than we'd like. While we're not hugely bearish on it, overall we think there are potentially better dividend stocks than Gilead Sciences out there.

Given that earnings are not growing, the dividend does not look nearly so attractive. See if the 22 analysts are forecasting a turnaround in our free collection of analyst estimates here.

We have also put together a list of global stocks with a market capitalisation above $1bn and yielding more 3%.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:GILD

Gilead Sciences

A biopharmaceutical company, discovers, develops, and commercializes medicines in the areas of unmet medical need in the United States, Europe, and internationally.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1947.9% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7719.6% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9218.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$19017.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

TH

TheTurntTomato on Constellium ·

CSTM: A High-Barrier Aerospace and EV Materials Leader Trading at Just 9x Earnings

Fair Value:US$37.1625.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TH

TheTurntTomato on PicS ·

A Fast-Growing Fintech Priced Like a Slow-Growth Bank

Fair Value:US$20.442.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TH

TheTurntTomato on Canadian Solar ·

Why CSIQ Could Be One of the Market's Most Misunderstood Renewable Energy Stocks

Fair Value:US$18.0515.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75027.0% undervalued

96 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5457.4% undervalued

64 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6512.6% undervalued

65 followersusers have followed this narrative

2 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

2

|0

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0