Advertisement

- United Kingdom

- /

- Specialized REITs

- /

- LSE:BYG

Is Big Yellow Group Plc (LON:BYG) A Healthy REIT?

Big Yellow Group Plc is a UK£1.7b mid-cap, real estate investment trust (REIT) based in Bagshot, United Kingdom. REITs own and operate income-generating property and adhere to a different set of regulations. This impacts how BYG’s business operates and also how we should analyse its stock. In this commentary, I'll take you through some of the things I look at when assessing BYG.

Check out our latest analysis for Big Yellow Group

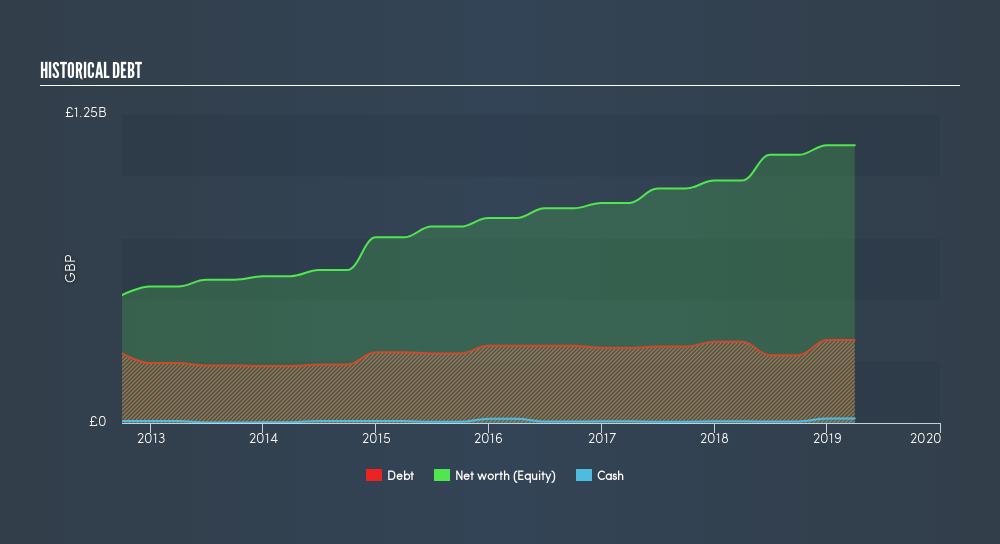

A common financial term REIT investors should know is Funds from Operations, or FFO for short, which is a REIT's main source of income from its portfolio of property, such as rent. FFO is a cleaner and more representative figure of how much BYG actually makes from its day-to-day operations, compared to net income, which can be affected by one-off activities or non-cash items such as depreciation. For BYG, its FFO of UK£72m makes up 77% of its gross profit, which means the majority of its earnings are high-quality and recurring.

Robust financial health can be measured using a common metric in the REIT investing world, FFO-to-debt. The calculation roughly estimates how long it will take for BYG to repay debt on its balance sheet, which gives us insight into how much risk is associated with having that level of debt on its books. With a ratio of 20%, the credit rating agency Standard & Poor would consider this as aggressive risk. This would take BYG 4.94 years to pay off using operating income alone. Given that long-term debt is a multi-year commitment this is not unusual, however, the longer it takes for a company to pay back debt, the higher the risk associated with that company.

I also look at BYG's interest coverage ratio, which demonstrates how many times its earnings can cover its yearly interest expense. This is similar to the concept above, but looks at the upcoming obligations. The ratio is typically calculated using EBIT, but for a REIT stock, it's better to use FFO divided by net interest. With an interest coverage ratio of 6.41x, it’s safe to say BYG is generating an appropriate amount of cash from its borrowings.

I also use FFO to look at BYG's valuation relative to other REITs in United Kingdom by using the price-to-FFO metric. This is conceptually the same as the price-to-earnings (PE) ratio, but as previously mentioned, FFO is more suitable. In BYG’s case its P/FFO is 23.27x, compared to the long-term industry average of 16.5x, meaning that it is overvalued.

Next Steps:

Big Yellow Group can bring diversification into your portfolio due to its unique REIT characteristics. Before you make a decision on the stock today, keep in mind I've only covered one metric in this article, the FFO, which is by no means comprehensive. I'd strongly recommend continuing your research on the following areas I believe are key fundamentals for BYG:

- Future Outlook: What are well-informed industry analysts predicting for BYG’s future growth? Take a look at our free research report of analyst consensus for BYG’s outlook.

- Valuation: What is BYG worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether BYG is currently mispriced by the market.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About LSE:BYG

Big Yellow Group

Big Yellow Group Plc is the UK's brand leader in self-storage and operates from a platform of 111 stores.

Good value with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

63 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5296.9% undervalued

4 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

Faltaren on AmpliTech Group ·

AmpliTech Group Will Triple Revenue by 2030 with O-RAN Expansion

Fair Value:US$3078.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Polaris Holdings ·

Share gains to fuel earnings momentum

Fair Value:JP¥211.166.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

66 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative