Tom Toomey became the CEO of UDR, Inc. (NYSE:UDR) in 2001. This report will, first, examine the CEO compensation levels in comparison to CEO compensation at other big companies. After that, we will consider the growth in the business. And finally we will reflect on how common stockholders have fared in the last few years, as a secondary measure of performance. This process should give us an idea about how appropriately the CEO is paid.

Check out our latest analysis for UDR

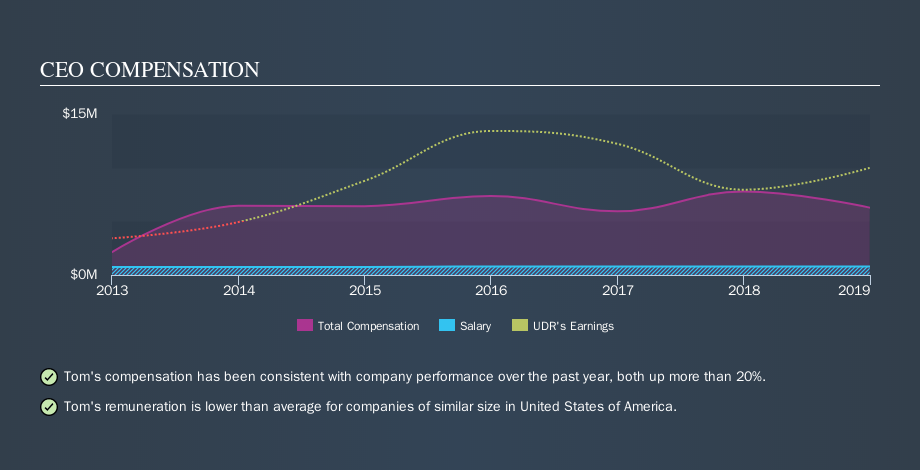

How Does Tom Toomey's Compensation Compare With Similar Sized Companies?

At the time of writing, our data says that UDR, Inc. has a market cap of US$16b, and reported total annual CEO compensation of US$6.3m for the year to December 2018. While we always look at total compensation first, we note that the salary component is less, at US$800k. Importantly, there may be performance hurdles relating to the non-salary component of the total compensation. We took a group of companies with market capitalizations over US$8.0b, and calculated the median CEO total compensation to be US$11m. Once you start looking at very large companies, you need to take a broader range, because there simply aren't that many of them.

A first glance this seems like a real positive for shareholders, since Tom Toomey is paid less than the average total compensation paid by other large companies. Though positive, it's important we delve into the performance of the actual business. It could be important to check this free visual depiction of what analysts expect for the future.

You can see, below, how CEO compensation at UDR has changed over time.

Is UDR, Inc. Growing?

Over the last three years UDR, Inc. has shrunk its earnings per share by an average of 19% per year (measured with a line of best fit). In the last year, its revenue is up 7.9%.

Sadly for shareholders, earnings per share are actually down, over three years. And the modest revenue growth over 12 months isn't much comfort against the reduced earnings per share. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO.

Has UDR, Inc. Been A Good Investment?

Boasting a total shareholder return of 62% over three years, UDR, Inc. has done well by shareholders. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

In Summary...

UDR, Inc. is currently paying its CEO below what is normal for large companies.

Tom Toomey is paid less than CEOs of other large companies. While the company isn't growing on our analysis, shareholder returns have been good in recent years. So, while it would be nice to have EPS growth, on our analysis the CEO compensation is not an issue. Whatever your view on compensation, you might want to check if insiders are buying or selling UDR shares (free trial).

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NYSE:UDR

UDR

UDR, Inc. (NYSE: UDR), an S&P 500 company, is a leading multifamily real estate investment trust with a demonstrated performance history of delivering superior and dependable returns by successfully managing, buying, selling, developing and redeveloping attractive real estate communities in targeted U.S.

6 star dividend payer with solid track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion