- United Kingdom

- /

- Communications

- /

- LSE:SPT

How Does Spirent Communications's (LON:SPT) P/E Compare To Its Industry, After Its Big Share Price Gain?

Spirent Communications (LON:SPT) shareholders are no doubt pleased to see that the share price has had a great month, posting a 31% gain, recovering from prior weakness. That brought the twelve month gain to a very sharp 62%.

All else being equal, a sharp share price increase should make a stock less attractive to potential investors. In the long term, share prices tend to follow earnings per share, but in the short term prices bounce around in response to short term factors (which are not always obvious). The implication here is that deep value investors might steer clear when expectations of a company are too high. One way to gauge market expectations of a stock is to look at its Price to Earnings Ratio (PE Ratio). A high P/E ratio means that investors have a high expectation about future growth, while a low P/E ratio means they have low expectations about future growth.

View our latest analysis for Spirent Communications

How Does Spirent Communications's P/E Ratio Compare To Its Peers?

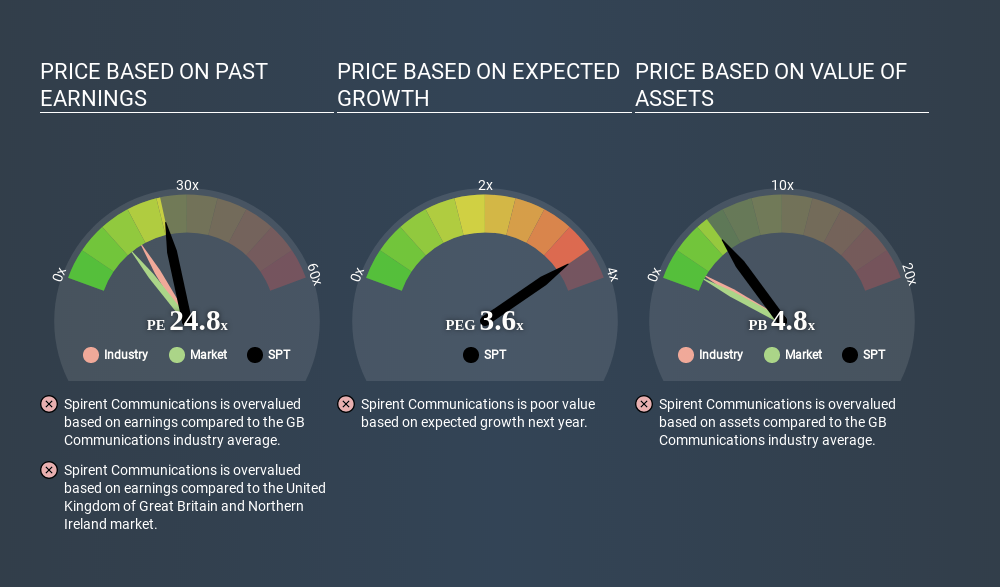

We can tell from its P/E ratio of 24.77 that there is some investor optimism about Spirent Communications. As you can see below, Spirent Communications has a higher P/E than the average company (17.9) in the communications industry.

Its relatively high P/E ratio indicates that Spirent Communications shareholders think it will perform better than other companies in its industry classification. The market is optimistic about the future, but that doesn't guarantee future growth. So further research is always essential. I often monitor director buying and selling.

How Growth Rates Impact P/E Ratios

P/E ratios primarily reflect market expectations around earnings growth rates. If earnings are growing quickly, then the 'E' in the equation will increase faster than it would otherwise. Therefore, even if you pay a high multiple of earnings now, that multiple will become lower in the future. Then, a lower P/E should attract more buyers, pushing the share price up.

It's nice to see that Spirent Communications grew EPS by a stonking 40% in the last year. And its annual EPS growth rate over 5 years is 31%. So we'd generally expect it to have a relatively high P/E ratio.

Remember: P/E Ratios Don't Consider The Balance Sheet

Don't forget that the P/E ratio considers market capitalization. That means it doesn't take debt or cash into account. Hypothetically, a company could reduce its future P/E ratio by spending its cash (or taking on debt) to achieve higher earnings.

While growth expenditure doesn't always pay off, the point is that it is a good option to have; but one that the P/E ratio ignores.

How Does Spirent Communications's Debt Impact Its P/E Ratio?

The extra options and safety that comes with Spirent Communications's US$183m net cash position means that it deserves a higher P/E than it would if it had a lot of net debt.

The Verdict On Spirent Communications's P/E Ratio

Spirent Communications trades on a P/E ratio of 24.8, which is above its market average of 13.7. Its net cash position is the cherry on top of its superb EPS growth. So based on this analysis we'd expect Spirent Communications to have a high P/E ratio. What we know for sure is that investors have become much more excited about Spirent Communications recently, since they have pushed its P/E ratio from 18.9 to 24.8 over the last month. For those who prefer to invest with the flow of momentum, that might mean it's time to put the stock on a watchlist, or research it. But the contrarian may see it as a missed opportunity.

Investors have an opportunity when market expectations about a stock are wrong. People often underestimate remarkable growth -- so investors can make money when fast growth is not fully appreciated. So this free visualization of the analyst consensus on future earnings could help you make the right decision about whether to buy, sell, or hold.

You might be able to find a better buy than Spirent Communications. If you want a selection of possible winners, check out this free list of interesting companies that trade on a P/E below 20 (but have proven they can grow earnings).

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About LSE:SPT

Spirent Communications

As of October 15, 2025, operates as a subsidiary of Keysight Technologies, Inc..

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Cheap if able to sustain revenue, and a potential bargain if able to turn store openings into revenue growth

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)