Advertisement

- United Kingdom

- /

- Chemicals

- /

- LSE:ZTF

How Do Zotefoams plc’s (LON:ZTF) Returns Compare To Its Industry?

Today we'll evaluate Zotefoams plc (LON:ZTF) to determine whether it could have potential as an investment idea. In particular, we'll consider its Return On Capital Employed (ROCE), as that can give us insight into how profitably the company is able to employ capital in its business.

Firstly, we'll go over how we calculate ROCE. Then we'll compare its ROCE to similar companies. Finally, we'll look at how its current liabilities affect its ROCE.

Understanding Return On Capital Employed (ROCE)

ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. All else being equal, a better business will have a higher ROCE. Overall, it is a valuable metric that has its flaws. Author Edwin Whiting says to be careful when comparing the ROCE of different businesses, since 'No two businesses are exactly alike.'

So, How Do We Calculate ROCE?

Analysts use this formula to calculate return on capital employed:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

Or for Zotefoams:

0.097 = UK£11m ÷ (UK£140m - UK£21m) (Based on the trailing twelve months to June 2019.)

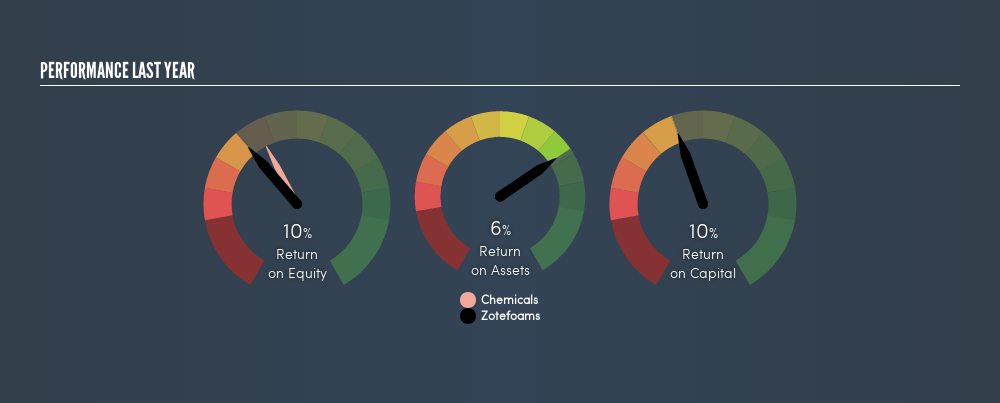

So, Zotefoams has an ROCE of 9.7%.

View our latest analysis for Zotefoams

Is Zotefoams's ROCE Good?

When making comparisons between similar businesses, investors may find ROCE useful. Using our data, Zotefoams's ROCE appears to be significantly below the 12% average in the Chemicals industry. This performance could be negative if sustained, as it suggests the business may underperform its industry. Regardless of where Zotefoams sits next to its industry, its ROCE in absolute terms appears satisfactory, and this company could be worth a closer look.

When considering this metric, keep in mind that it is backwards looking, and not necessarily predictive. ROCE can be deceptive for cyclical businesses, as returns can look incredible in boom times, and terribly low in downturns. ROCE is, after all, simply a snap shot of a single year. What happens in the future is pretty important for investors, so we have prepared a free report on analyst forecasts for Zotefoams.

What Are Current Liabilities, And How Do They Affect Zotefoams's ROCE?

Current liabilities include invoices, such as supplier payments, short-term debt, or a tax bill, that need to be paid within 12 months. The ROCE equation subtracts current liabilities from capital employed, so a company with a lot of current liabilities appears to have less capital employed, and a higher ROCE than otherwise. To counter this, investors can check if a company has high current liabilities relative to total assets.

Zotefoams has total assets of UK£140m and current liabilities of UK£21m. As a result, its current liabilities are equal to approximately 15% of its total assets. Low current liabilities are not boosting the ROCE too much.

What We Can Learn From Zotefoams's ROCE

This is good to see, and with a sound ROCE, Zotefoams could be worth a closer look. Zotefoams shapes up well under this analysis, but it is far from the only business delivering excellent numbers . You might also want to check this free collection of companies delivering excellent earnings growth.

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About LSE:ZTF

Zotefoams

Manufactures, distributes, and sells polyolefin foams in the United Kingdom, rest of Europe, North America, and internationally.

Very undervalued with flawless balance sheet.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.552.0% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$58013.6% overvalued

25 followersusers have followed this narrative

3 commentsusers have commented on this narrative

24 likesusers have liked this narrative

TH

TheBestInvestor on Lockheed Martin ·

Orbit + Aero + Defense

Fair Value:US$673.8821.4% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on Steppe Gold ·

A case for Steppe Gold, bear case CAD $4, base case CAD $15, bull case CAD $25

Fair Value:CA$2594.4% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

DE

DENYAPE on Paragon Technologies ·

Deep Analysis of Paragon Technologies Inc. (PGNT): A Forensic Examination of Governance, Valuation, and Strategic Recovery

Fair Value:US$16.3472.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AB

abdulhayee on MCB Bank ·

MCB Bank is aiming for a fair value target of 276 with growth in sight

Fair Value:PK₨27647.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

andre_santos on CTT - Correios De Portugal ·

CTT - A Fundamental Valuation

Fair Value:€10.6740.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3955.3% overvalued

52 followersusers have followed this narrative

3 commentsusers have commented on this narrative

43 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.234.6% undervalued

65 followersusers have followed this narrative

1 commentusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$579.5728.3% undervalued

1384 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

TA

Taurustunez88 on Dangote Sugar Refinery ·

With the N500b rights issue, I believe Dangote sugar refinery’s loss due to FX pressures will be dra...

1

|0