Advertisement

- New Zealand

- /

- Software

- /

- NZSE:GEO

Here's Why We're Watching Geo's (NZSE:GEO) Cash Burn Situation

We can readily understand why investors are attracted to unprofitable companies. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

So should Geo (NZSE:GEO) shareholders be worried about its cash burn? For the purpose of this article, we'll define cash burn as the amount of cash the company is spending each year to fund its growth (also called its negative free cash flow). The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

Check out our latest analysis for Geo

Does Geo Have A Long Cash Runway?

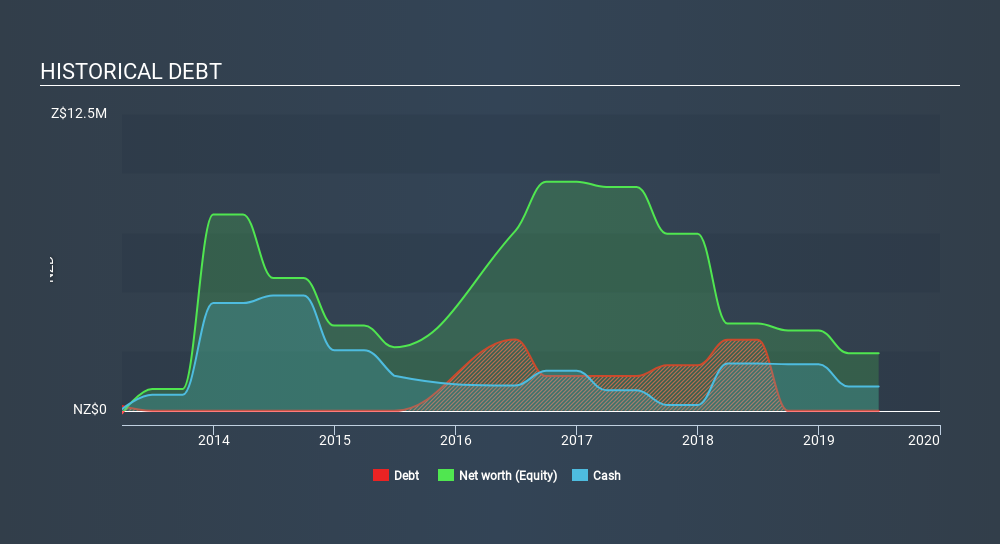

You can calculate a company's cash runway by dividing the amount of cash it has by the rate at which it is spending that cash. When Geo last reported its balance sheet in June 2019, it had zero debt and cash worth NZ$1.0m. In the last year, its cash burn was NZ$2.1m. That means it had a cash runway of around 6 months as of June 2019. That's a very short cash runway which indicates an imminent need to douse the cash burn or find more funding. The image below shows how its cash balance has been changing over the last few years.

How Well Is Geo Growing?

It was fairly positive to see that Geo reduced its cash burn by 25% during the last year. Revenue also improved during the period, increasing by 18%. Considering the factors above, the company doesn’t fare badly when it comes to assessing how it is changing over time. In reality, this article only makes a short study of the company's growth data. This graph of historic earnings and revenue shows how Geo is building its business over time.

Can Geo Raise More Cash Easily?

Given Geo's revenue is receding, there's a considerable chance it will eventually need to raise more money to spend on driving growth. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash to fund growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Since it has a market capitalisation of NZ$7.4m, Geo's NZ$2.1m in cash burn equates to about 29% of its market value. That's not insignificant, and if the company had to sell enough shares to fund another year's growth at the current share price, you'd likely witness fairly costly dilution.

Is Geo's Cash Burn A Worry?

On this analysis of Geo's cash burn, we think its revenue growth was reassuring, while its cash runway has us a bit worried. Summing up, we think the Geo's cash burn is a risk, based on the factors we mentioned in this article. While we always like to monitor cash burn for early stage companies, qualitative factors such as the CEO pay can also shed light on the situation. Click here to see free what the Geo CEO is paid..

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies, and this list of stocks growth stocks (according to analyst forecasts)

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NZSE:GEO

Geo

Geo Limited develops and deploys cloud-based mobile workforce productivity technologies in New Zealand and internationally.

Slightly overvalued with worrying balance sheet.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.562.8% undervalued

23 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

73 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56052.2% undervalued

64 followersusers have followed this narrative

4 commentsusers have commented on this narrative

30 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2780.9% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

RO

RockeTeller on Orezone Gold ·

Orezone Gold Could 3X–5X, Bomboré Ramp + Casa Berardi Quebec Asset Delivers 160-180Koz in 2026

Fair Value:CA$10.6878.4% undervalued

11 followersusers have followed this narrative

4 commentsusers have commented on this narrative

1 likeusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8210.0% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on NeXGold Mining ·

NexGold Mining: 4.7Moz M&I Resources, $100M Cash + Debt-Free, Construction Decision 2026 Undervalued Canadian Gold Developer

Fair Value:CA$39.5296.9% undervalued

5 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75033.5% undervalued

73 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9636.6% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.1% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative