Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:STBA

Here's Why We Think S&T Bancorp (NASDAQ:STBA) Is Well Worth Watching

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it completely lacks a track record of revenue and profit. But as Warren Buffett has mused, 'If you've been playing poker for half an hour and you still don't know who the patsy is, you're the patsy.' When they buy such story stocks, investors are all too often the patsy.

In contrast to all that, I prefer to spend time on companies like S&T Bancorp (NASDAQ:STBA), which has not only revenues, but also profits. While that doesn't make the shares worth buying at any price, you can't deny that successful capitalism requires profit, eventually. Conversely, a loss-making company is yet to prove itself with profit, and eventually the sweet milk of external capital may run sour.

Check out our latest analysis for S&T Bancorp

How Quickly Is S&T Bancorp Increasing Earnings Per Share?

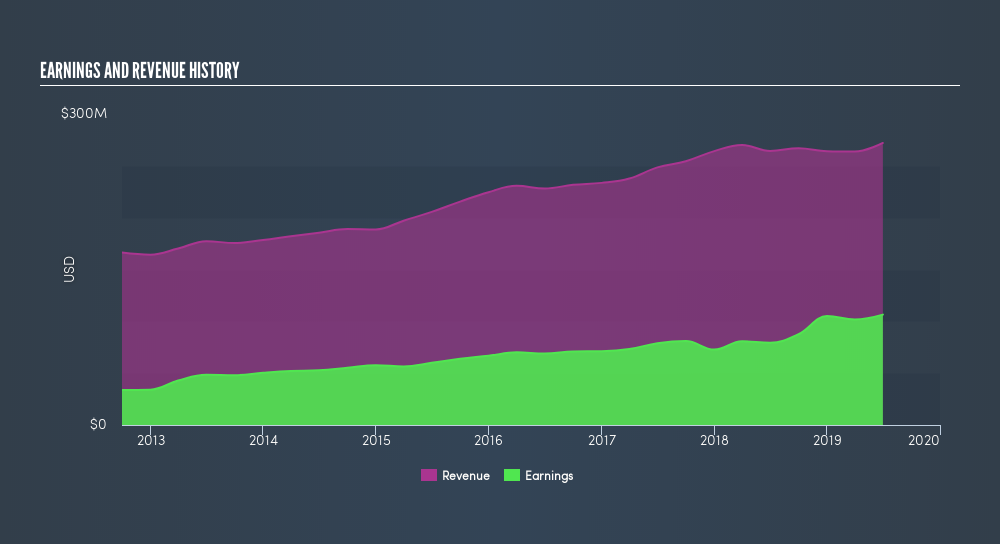

If a company can keep growing earnings per share (EPS) long enough, its share price will eventually follow. That makes EPS growth an attractive quality for any company. Over the last three years, S&T Bancorp has grown EPS by 16% per year. That's a good rate of growth, if it can be sustained.

I like to take a look at earnings before interest and (EBIT) tax margins, as well as revenue growth, to get another take on the quality of the company's growth. Not all of S&T Bancorp's revenue this year is revenue from operations, so keep in mind the revenue and margin numbers I've used might not be the best representation of the underlying business. While we note S&T Bancorp's EBIT margins were flat over the last year, revenue grew by a solid 2.9% to US$272m. That's a real positive.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of S&T Bancorp's forecast profits?

Are S&T Bancorp Insiders Aligned With All Shareholders?

Like the kids in the streets standing up for their beliefs, insider share purchases give me reason to believe in a brighter future. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

Despite -US$325.4k worth of sales, S&T Bancorp insiders have overwhelmingly been buying the stock, spending US$839k on purchases in the last twelve months. On balance, to me, this signals their optimism. It is also worth noting that it was Director James Gibson who made the biggest single purchase, worth US$467k, paying US$38.92 per share.

Along with the insider buying, another encouraging sign for S&T Bancorp is that insiders, as a group, have a considerable shareholding. To be specific, they have US$32m worth of shares. That's a lot of money, and no small incentive to work hard. Despite being just 2.7% of the company, the value of that investment is enough to show insiders have plenty riding on the venture.

While insiders are apparently happy to hold and accumulate shares, that is just part of the pretty picture. That's because on our analysis the CEO, Todd Brice, is paid less than the median for similar sized companies. For companies with market capitalizations between US$1.0b and US$3.2b, like S&T Bancorp, the median CEO pay is around US$4.1m.

The CEO of S&T Bancorp only received US$1.3m in total compensation for the year ending December 2018. That's clearly well below average, so at a glance, that arrangement seems generous to shareholders, and points to a modest remuneration culture. While the level of CEO compensation isn't a huge factor in my view of the company, modest remuneration is a positive, because it suggests that the board keeps shareholder interests in mind. It can also be a sign of good governance, more generally.

Should You Add S&T Bancorp To Your Watchlist?

As I already mentioned, S&T Bancorp is a growing business, which is what I like to see. Better yet, insiders are significant shareholders, and have been buying more shares. That makes the company a prime candidate for my watchlist - and arguably a research priority. Once you've identified a business you like, the next step is to consider what you think it's worth. And right now is your chance to view our exclusive discounted cashflow valuation of S&T Bancorp. You might benefit from giving it a glance today.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of S&T Bancorp, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NasdaqGS:STBA

S&T Bancorp

Operates as the bank holding company for S&T Bank that provides retail and commercial banking products and services to consumer, commercial, and small business in Pennsylvania and Ohio.

Flawless balance sheet, good value and pays a dividend.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% undervalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|45.0% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.4% undervalued

TI

Community Contributor