Advertisement

Here’s why USU Software AG’s (ETR:OSP2) Returns On Capital Matters So Much

Today we are going to look at USU Software AG (ETR:OSP2) to see whether it might be an attractive investment prospect. Specifically, we'll consider its Return On Capital Employed (ROCE), since that will give us an insight into how efficiently the business can generate profits from the capital it requires.

First up, we'll look at what ROCE is and how we calculate it. Second, we'll look at its ROCE compared to similar companies. And finally, we'll look at how its current liabilities are impacting its ROCE.

Return On Capital Employed (ROCE): What is it?

ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. In general, businesses with a higher ROCE are usually better quality. Overall, it is a valuable metric that has its flaws. Author Edwin Whiting says to be careful when comparing the ROCE of different businesses, since 'No two businesses are exactly alike.

How Do You Calculate Return On Capital Employed?

The formula for calculating the return on capital employed is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

Or for USU Software:

0.08 = €5.8m ÷ (€109m - €36m) (Based on the trailing twelve months to March 2020.)

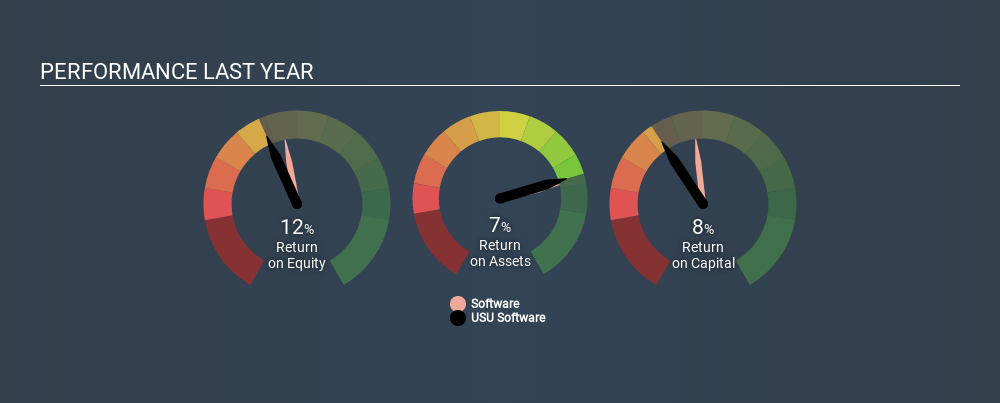

Therefore, USU Software has an ROCE of 8.0%.

Check out our latest analysis for USU Software

Is USU Software's ROCE Good?

One way to assess ROCE is to compare similar companies. In this analysis, USU Software's ROCE appears meaningfully below the 12% average reported by the Software industry. This performance is not ideal, as it suggests the company may not be deploying its capital as effectively as some competitors. Aside from the industry comparison, USU Software's ROCE is mediocre in absolute terms, considering the risk of investing in stocks versus the safety of a bank account. Investors may wish to consider higher-performing investments.

We can see that, USU Software currently has an ROCE of 8.0%, less than the 11% it reported 3 years ago. Therefore we wonder if the company is facing new headwinds. The image below shows how USU Software's ROCE compares to its industry, and you can click it to see more detail on its past growth.

When considering ROCE, bear in mind that it reflects the past and does not necessarily predict the future. ROCE can be deceptive for cyclical businesses, as returns can look incredible in boom times, and terribly low in downturns. ROCE is only a point-in-time measure. Since the future is so important for investors, you should check out our free report on analyst forecasts for USU Software.

USU Software's Current Liabilities And Their Impact On Its ROCE

Short term (or current) liabilities, are things like supplier invoices, overdrafts, or tax bills that need to be paid within 12 months. The ROCE equation subtracts current liabilities from capital employed, so a company with a lot of current liabilities appears to have less capital employed, and a higher ROCE than otherwise. To counteract this, we check if a company has high current liabilities, relative to its total assets.

USU Software has total assets of €109m and current liabilities of €36m. As a result, its current liabilities are equal to approximately 33% of its total assets. USU Software's middling level of current liabilities have the effect of boosting its ROCE a bit.

The Bottom Line On USU Software's ROCE

Despite this, its ROCE is still mediocre, and you may find more appealing investments elsewhere. But note: make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a P/E ratio below 20).

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About XTRA:OSP2

USU Software

Provides software and service solutions for information technology (IT) and customer service management in Germany and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1939.7% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6527.1% undervalued

28 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

JD

JD009 on Celsius Holdings ·

From $5M to $2B: Why the 2024 Crash Was the Best Buying Opportunity in Consumer Stocks

Fair Value:US$55.4345.6% undervalued

10 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

WA

Wavefarer on Accenture ·

High-quality global services company facing an AI-driven valuation reset.

Fair Value:US$30155.3% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

HE

HedgeY on Arm Holdings ·

The Architecture Layer of AI Computing - But Priced Like the Future Already Arrived?

Fair Value:US$43034.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CC

cchan3330 on Pacific Basin Shipping ·

Pacific Basin Betting on Green Methanol for Future Growth

Fair Value:HK$3.065.2% overvalued

6 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

ES

Ester on A1 A.K. Koh Group Berhad ·

A1 A.K. Koh Group Berhad Expands Footprint via Strategic Land Acquisition in Puchong Jaya

Fair Value:RM 0.3655.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.3% undervalued

90 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5451.0% undervalued

62 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3462.5% undervalued

60 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative