- United States

- /

- Pharma

- /

- OTCPK:CYTO.F

Here's Why Auris Medical Holding (NASDAQ:EARS) Must Use Its Cash Wisely

Even when a business is losing money, it's possible for shareholders to make money if they buy a good business at the right price. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. Having said that, unprofitable companies are risky because they could potentially burn through all their cash and become distressed.

So, the natural question for Auris Medical Holding (NASDAQ:EARS) shareholders is whether they should be concerned by its rate of cash burn. In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. Let's start with an examination of the business's cash, relative to its cash burn.

View our latest analysis for Auris Medical Holding

Does Auris Medical Holding Have A Long Cash Runway?

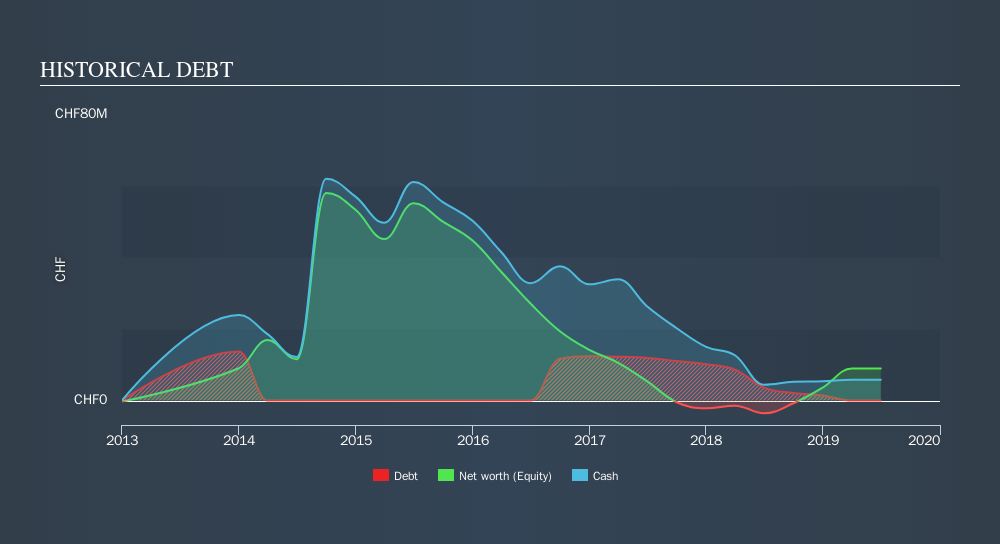

A company's cash runway is calculated by dividing its cash hoard by its cash burn. In June 2019, Auris Medical Holding had CHF5.8m in cash, and was debt-free. In the last year, its cash burn was CHF15m. Therefore, from June 2019 it had roughly 5 months of cash runway. With a cash runway that short, we strongly believe that the company must raise cash or else douse its cash burn promptly. The image below shows how its cash balance has been changing over the last few years.

How Is Auris Medical Holding's Cash Burn Changing Over Time?

Because Auris Medical Holding isn't currently generating revenue, we consider it an early-stage business. Nonetheless, we can still examine its cash burn trajectory as part of our assessment of its cash burn situation. As it happens, the company's cash burn reduced by 21% over the last year, which suggests that management are mindful of the possibility of running out of cash. Clearly, however, the crucial factor is whether the company will grow its business going forward. So you might want to take a peek at how much the company is expected to grow in the next few years.

Can Auris Medical Holding Raise More Cash Easily?

While Auris Medical Holding is showing a solid reduction in its cash burn, it's still worth considering how easily it could raise more cash, even just to fuel faster growth. Companies can raise capital through either debt or equity. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash to fund growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Since it has a market capitalisation of US$5.4m, Auris Medical Holding's CHF15m in cash burn equates to about 276% of its market value. That suggests the company may have some funding difficulties, and we'd be very wary of the stock.

How Risky Is Auris Medical Holding's Cash Burn Situation?

There are no prizes for guessing that we think Auris Medical Holding's cash burn is a bit of a worry. In particular, we think its cash burn relative to its market cap suggests it isn't in a good position to keep funding growth. And although we accept its cash burn reduction wasn't as worrying as its cash burn relative to its market cap, it was still a real negative; as indeed were all the factors we considered in this article. Looking at the metrics in this article all together, we consider its cash burn situation to be rather dangerous, and likely to cost shareholders one way or the other. While it's important to consider hard data like the metrics discussed above, many investors would also be interested to note that Auris Medical Holding insiders have been trading shares in the company. Click here to find out if they have been buying or selling.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About OTCPK:CYTO.F

Altamira Therapeutics

Operates as a preclinical-stage biopharmaceutical company in Switzerland, Australia, the United States, and Europe.

Moderate risk and slightly overvalued.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion