Advertisement

Here's What To Make Of K.M. Sugar Mills' (NSE:KMSUGAR) Returns On Capital

If you're looking for a multi-bagger, there's a few things to keep an eye out for. One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. With that in mind, the ROCE of K.M. Sugar Mills (NSE:KMSUGAR) looks decent, right now, so lets see what the trend of returns can tell us.

Return On Capital Employed (ROCE): What is it?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on K.M. Sugar Mills is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

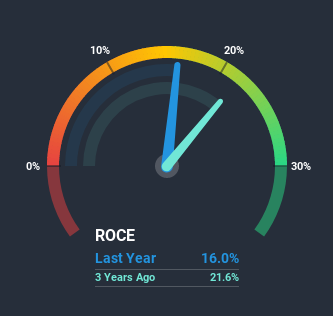

0.16 = ₹436m ÷ (₹5.5b - ₹2.8b) (Based on the trailing twelve months to June 2020).

Therefore, K.M. Sugar Mills has an ROCE of 16%. In absolute terms, that's a satisfactory return, but compared to the Food industry average of 13% it's much better.

View our latest analysis for K.M. Sugar Mills

Historical performance is a great place to start when researching a stock so above you can see the gauge for K.M. Sugar Mills' ROCE against it's prior returns. If you're interested in investigating K.M. Sugar Mills' past further, check out this free graph of past earnings, revenue and cash flow.

What Can We Tell From K.M. Sugar Mills' ROCE Trend?

While the returns on capital are good, they haven't moved much. Over the past five years, ROCE has remained relatively flat at around 16% and the business has deployed 290% more capital into its operations. 16% is a pretty standard return, and it provides some comfort knowing that K.M. Sugar Mills has consistently earned this amount. Stable returns in this ballpark can be unexciting, but if they can be maintained over the long run, they often provide nice rewards to shareholders.

One more thing to note, even though ROCE has remained relatively flat over the last five years, the reduction in current liabilities to 51% of total assets, is good to see from a business owner's perspective. Effectively suppliers now fund less of the business, which can lower some elements of risk. We'd like to see this trend continue though because as it stands today, thats still a pretty high level.What We Can Learn From K.M. Sugar Mills' ROCE

In the end, K.M. Sugar Mills has proven its ability to adequately reinvest capital at good rates of return. And the stock has done incredibly well with a 142% return over the last five years, so long term investors are no doubt ecstatic with that result. So while the positive underlying trends may be accounted for by investors, we still think this stock is worth looking into further.

K.M. Sugar Mills does have some risks, we noticed 5 warning signs (and 1 which is significant) we think you should know about.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

If you’re looking to trade K.M. Sugar Mills, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if K.M. Sugar Mills might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:KMSUGAR

K.M. Sugar Mills

Engages in manufacturing and sells sugar and industrial alcohol in India.

Solid track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|58.8% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|17.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|2.4% undervalued

RO

Community Contributor