Advertisement

- United Kingdom

- /

- Electrical

- /

- LSE:DSCV

Here’s What discoverIE Group plc’s (LON:DSCV) Return On Capital Can Tell Us

Today we'll look at discoverIE Group plc (LON:DSCV) and reflect on its potential as an investment. To be precise, we'll consider its Return On Capital Employed (ROCE), as that will inform our view of the quality of the business.

First of all, we'll work out how to calculate ROCE. Next, we'll compare it to others in its industry. And finally, we'll look at how its current liabilities are impacting its ROCE.

What is Return On Capital Employed (ROCE)?

ROCE measures the 'return' (pre-tax profit) a company generates from capital employed in its business. All else being equal, a better business will have a higher ROCE. Ultimately, it is a useful but imperfect metric. Author Edwin Whiting says to be careful when comparing the ROCE of different businesses, since 'No two businesses are exactly alike.

So, How Do We Calculate ROCE?

Analysts use this formula to calculate return on capital employed:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

Or for discoverIE Group:

0.098 = UK£27m ÷ (UK£373m - UK£101m) (Based on the trailing twelve months to September 2019.)

Therefore, discoverIE Group has an ROCE of 9.8%.

Check out our latest analysis for discoverIE Group

Is discoverIE Group's ROCE Good?

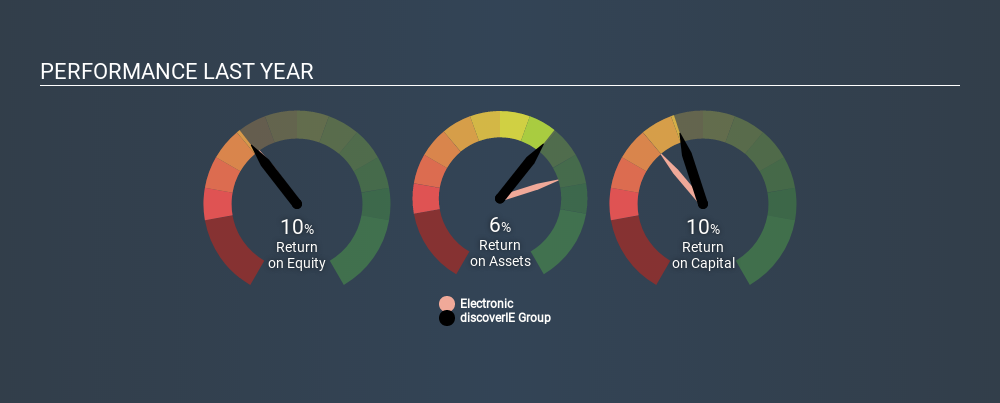

ROCE is commonly used for comparing the performance of similar businesses. Using our data, discoverIE Group's ROCE appears to be around the 9.5% average of the Electronic industry. Independently of how discoverIE Group compares to its industry, its ROCE in absolute terms appears decent, and the company may be worthy of closer investigation.

We can see that, discoverIE Group currently has an ROCE of 9.8% compared to its ROCE 3 years ago, which was 7.2%. This makes us wonder if the company is improving. You can see in the image below how discoverIE Group's ROCE compares to its industry. Click to see more on past growth.

Remember that this metric is backwards looking - it shows what has happened in the past, and does not accurately predict the future. ROCE can be deceptive for cyclical businesses, as returns can look incredible in boom times, and terribly low in downturns. ROCE is only a point-in-time measure. What happens in the future is pretty important for investors, so we have prepared a free report on analyst forecasts for discoverIE Group.

How discoverIE Group's Current Liabilities Impact Its ROCE

Current liabilities include invoices, such as supplier payments, short-term debt, or a tax bill, that need to be paid within 12 months. The ROCE equation subtracts current liabilities from capital employed, so a company with a lot of current liabilities appears to have less capital employed, and a higher ROCE than otherwise. To check the impact of this, we calculate if a company has high current liabilities relative to its total assets.

discoverIE Group has total assets of UK£373m and current liabilities of UK£101m. Therefore its current liabilities are equivalent to approximately 27% of its total assets. Low current liabilities are not boosting the ROCE too much.

The Bottom Line On discoverIE Group's ROCE

With that in mind, discoverIE Group's ROCE appears pretty good. There might be better investments than discoverIE Group out there, but you will have to work hard to find them . These promising businesses with rapidly growing earnings might be right up your alley.

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About LSE:DSCV

discoverIE Group

Designs, manufactures, and supplies specialist electronic components for industrial applications in the United Kingdom, Europe, North America, Asia, and internationally.

Excellent balance sheet with acceptable track record.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.558.3% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.1% undervalued

58 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56053.2% undervalued

60 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.3% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

NO

North49_ on iShares - iShares MSCI South Korea ETF ·

EWY:US NYSE Arca iShares Msci South Korea ETF, an opportunity to diversify your tech investments.

Fair Value:US$273.4527.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.885.3% undervalued

89 followersusers have followed this narrative

7 commentsusers have commented on this narrative

1 likeusers have liked this narrative

RO

RockeTeller on Montage Gold ·

Montage Gold, Building West Africa’s Next 300Koz Producer, First Pour Late 2026, 5.88Moz Resource

Fair Value:CA$23.538.3% undervalued

18 followersusers have followed this narrative

4 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9638.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17060.0% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative