Advertisement

- Belgium

- /

- Consumer Durables

- /

- ENXTBR:BELYS

Has Balta Group (EBR:BALTA) Got What It Takes To Become A Multi-Bagger?

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. Although, when we looked at Balta Group (EBR:BALTA), it didn't seem to tick all of these boxes.

What is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for Balta Group, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

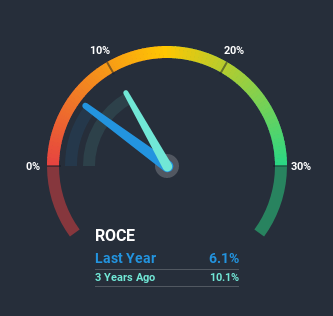

0.061 = €36m ÷ (€788m - €199m) (Based on the trailing twelve months to December 2019).

Thus, Balta Group has an ROCE of 6.1%. Ultimately, that's a low return and it under-performs the Consumer Durables industry average of 8.5%.

See our latest analysis for Balta Group

In the above chart we have a measured Balta Group's prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Balta Group here for free.

So How Is Balta Group's ROCE Trending?

On the surface, the trend of ROCE at Balta Group doesn't inspire confidence. Around five years ago the returns on capital were 13%, but since then they've fallen to 6.1%. Meanwhile, the business is utilizing more capital but this hasn't moved the needle much in terms of sales in the past 12 months, so this could reflect longer term investments. It may take some time before the company starts to see any change in earnings from these investments.

On a related note, Balta Group has decreased its current liabilities to 25% of total assets. So we could link some of this to the decrease in ROCE. Effectively this means their suppliers or short-term creditors are funding less of the business, which reduces some elements of risk. Since the business is basically funding more of its operations with it's own money, you could argue this has made the business less efficient at generating ROCE.Our Take On Balta Group's ROCE

Bringing it all together, while we're somewhat encouraged by Balta Group's reinvestment in its own business, we're aware that returns are shrinking. And investors may be expecting the fundamentals to get a lot worse because the stock has crashed 91% over the last three years. In any case, the stock doesn't have these traits of a multi-bagger discussed above, so if that's what you're looking for, we think you'd have more luck elsewhere.

On a final note, we found 3 warning signs for Balta Group (1 is a bit concerning) you should be aware of.

While Balta Group isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

If you decide to trade Balta Group, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Belysse Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About ENXTBR:BELYS

Belysse Group

Manufactures and sells textile floor coverings for commercial and residential applications in Europe, North America, and internationally.

Undervalued with moderate growth potential.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.562.2% undervalued

33 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.828.9% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23059.6% overvalued

39 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32039.9% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

BL

Blagget on BP Silver ·

“valer un Potosí” GOOGLE IT. Now you’re should be kinda locked in. Educate yourself, Read the rest.

Fair Value:CA$685.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TimLee on Master Tec Group Berhad ·

Master Tec’s TNB Extension Reinforces Its Utility-Scale Growth Story

Fair Value:RM 1.6841.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

danmad on Judo Capital Holdings ·

A Fast-Growing SME Lender Trading Like a Problem Bank

Fair Value:AU$0.954.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.1% undervalued

84 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9630.8% undervalued

64 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5457.5% undervalued

59 followersusers have followed this narrative

3 commentsusers have commented on this narrative

10 likesusers have liked this narrative