Advertisement

Emirates Integrated Telecommunications Company PJSC Recorded A 9.8% Miss On Revenue: Analysts Are Revisiting Their Models

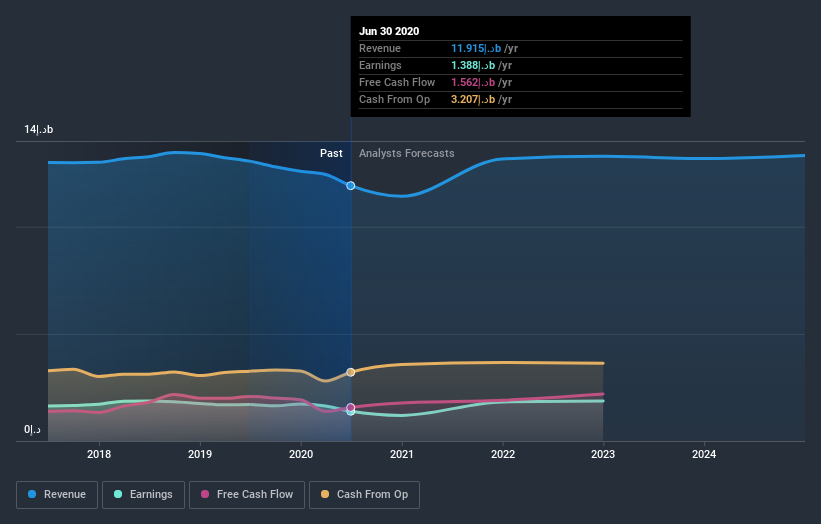

The quarterly results for Emirates Integrated Telecommunications Company PJSC (DFM:DU) were released last week, making it a good time to revisit its performance. Revenues came in 9.8% below expectations, at د.إ2.7b. Statutory earnings per share were relatively better off, with a per-share profit of د.إ0.38 being roughly in line with analyst estimates. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

Check out our latest analysis for Emirates Integrated Telecommunications Company PJSC

Taking into account the latest results, the current consensus, from the twin analysts covering Emirates Integrated Telecommunications Company PJSC, is for revenues of د.إ11.4b in 2020, which would reflect a noticeable 4.2% reduction in Emirates Integrated Telecommunications Company PJSC's sales over the past 12 months. Statutory earnings per share are predicted to bounce 29% to د.إ0.40. In the lead-up to this report, the analysts had been modelling revenues of د.إ13.3b and earnings per share (EPS) of د.إ0.39 in 2020. It looks like there's been a meaningful change to the consensus view following the recent earnings report, with the analysts making a real cut to to revenue forecasts and a slight bump in to next year's earnings estimates.

There's been no real change to the average price target of د.إ6.83, with the lower revenue and higher earnings forecasts not expected to meaningfully impact the company's valuation over a longer timeframe.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We would highlight that sales are expected to reverse, with the forecast 4.2% revenue decline a notable change from historical growth of 0.6% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 2.9% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Emirates Integrated Telecommunications Company PJSC is expected to lag the wider industry.

The Bottom Line

The most important thing here is that the analysts upgraded their earnings per share estimates, suggesting that there has been a clear increase in optimism towards Emirates Integrated Telecommunications Company PJSC following these results. On the negative side, they also downgraded their revenue estimates, and forecasts imply revenues will perform worse than the wider industry. Even so, earnings are more important to the intrinsic value of the business. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have analyst estimates for Emirates Integrated Telecommunications Company PJSC going out as far as 2024, and you can see them free on our platform here.

And what about risks? Every company has them, and we've spotted 1 warning sign for Emirates Integrated Telecommunications Company PJSC you should know about.

When trading Emirates Integrated Telecommunications Company PJSC or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Emirates Integrated Telecommunications Company PJSC might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About DFM:DU

Emirates Integrated Telecommunications Company PJSC

Provides mobile, fixed services, broadband connectivity, and IPTV solutions to homes and businesses in the United Arab Emirates.

Outstanding track record with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor