Advertisement

- United States

- /

- Personal Products

- /

- OTCPK:REVR.Q

Earnings Update: Here's Why Analysts Just Lifted Their Revlon, Inc. (NYSE:REV) Price Target To US$12.00

As you might know, Revlon, Inc. (NYSE:REV) last week released its latest quarterly, and things did not turn out so great for shareholders. Revenues missed expectations somewhat, coming in at US$453m, but statutory earnings fell catastrophically short, with a loss of US$4.02 some 272% larger than what the analyst had predicted. This is an important time for investors, as they can track a company's performance in its report, look at what expert is forecasting for next year, and see if there has been any change to expectations for the business. We've gathered the most recent statutory forecasts to see whether the analyst has changed their earnings models, following these results.

See our latest analysis for Revlon

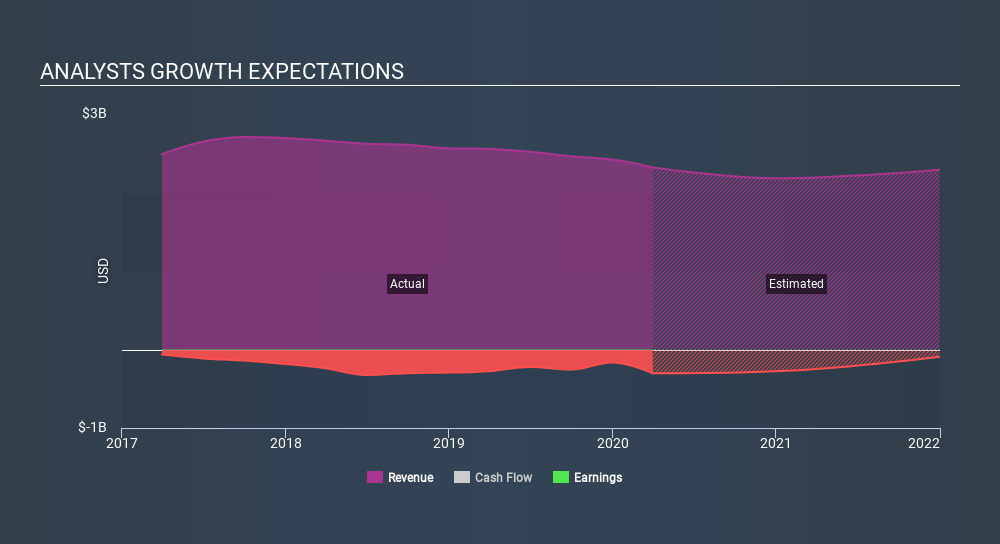

After the latest results, the consensus from Revlon's lone analyst is for revenues of US$2.18b in 2020, which would reflect a discernible 5.9% decline in sales compared to the last year of performance. Losses are forecast to narrow 8.9% to US$5.20 per share. Before this earnings announcement, the analyst had been modelling revenues of US$2.25b and losses of US$2.26 per share in 2020. So it's pretty clear the analyst has mixed opinions on Revlon after this update; revenues were downgraded and per-share losses expected to increase.

The average price target lifted 20% to US$12.00, clearly signalling that the weaker revenue and EPS outlook are not expected to weigh on the stock over the longer term.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We would highlight that sales are expected to reverse, with the forecast 5.9% revenue decline a notable change from historical growth of 6.3% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 6.5% next year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Revlon is expected to lag the wider industry.

The Bottom Line

The most important thing to note is the forecast of increased losses next year, suggesting all may not be well at Revlon. On the negative side, they also downgraded their revenue estimates, and forecasts imply revenues will perform worse than the wider industry. There was also a nice increase in the price target, with the analyst clearly feeling that the intrinsic value of the business is improving.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have analyst estimates for Revlon going out as far as 2021, and you can see them free on our platform here.

You still need to take note of risks, for example - Revlon has 3 warning signs (and 1 which can't be ignored) we think you should know about.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About OTCPK:REVR.Q

Revlon

Revlon, Inc. develops, manufactures, markets, distributes, and sells beauty and personal care products worldwide.

Slightly overvalued with weak fundamentals.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor