Advertisement

- United States

- /

- Trade Distributors

- /

- NasdaqGM:WLFC

Does Willis Lease Finance Corporation's (NASDAQ:WLFC) CEO Salary Reflect Performance?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Charlie Willis has been the CEO of Willis Lease Finance Corporation (NASDAQ:WLFC) since 1985. First, this article will compare CEO compensation with compensation at similar sized companies. Then we'll look at a snap shot of the business growth. And finally we will reflect on how common stockholders have fared in the last few years, as a secondary measure of performance. This method should give us information to assess how appropriately the company pays the CEO.

View our latest analysis for Willis Lease Finance

How Does Charlie Willis's Compensation Compare With Similar Sized Companies?

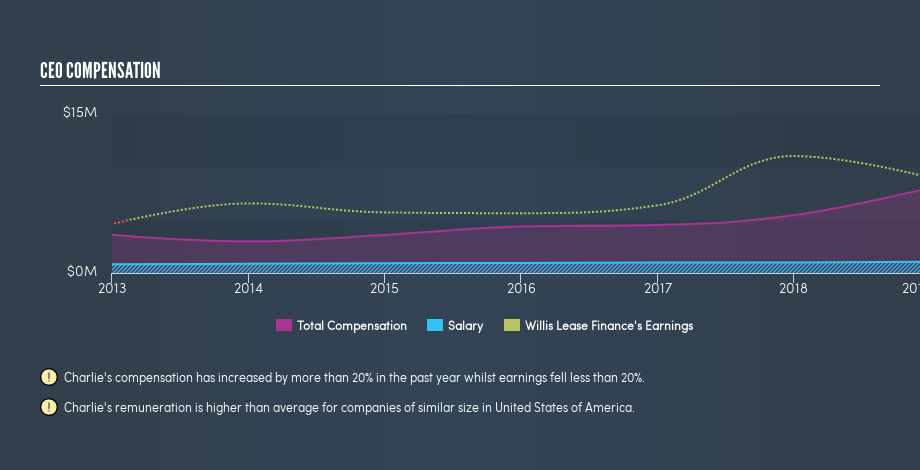

According to our data, Willis Lease Finance Corporation has a market capitalization of US$316m, and pays its CEO total annual compensation worth US$8.0m. (This is based on the year to December 2018). Notably, that's an increase of 48% over the year before. We think total compensation is more important but we note that the CEO salary is lower, at US$1.1m. When we examined a selection of companies with market caps ranging from US$200m to US$800m, we found the median CEO total compensation was US$1.8m.

Thus we can conclude that Charlie Willis receives more in total compensation than the median of a group of companies in the same market, and of similar size to Willis Lease Finance Corporation. However, this doesn't necessarily mean the pay is too high. A closer look at the performance of the underlying business will give us a better idea about whether the pay is particularly generous.

You can see, below, how CEO compensation at Willis Lease Finance has changed over time.

Is Willis Lease Finance Corporation Growing?

Over the last three years Willis Lease Finance Corporation has grown its earnings per share (EPS) by an average of 60% per year (using a line of best fit). In the last year, its revenue is up 43%.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's great to see that revenue growth is strong, too. These metrics suggest the business is growing strongly. We don't have analyst forecasts, but you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Willis Lease Finance Corporation Been A Good Investment?

Most shareholders would probably be pleased with Willis Lease Finance Corporation for providing a total return of 121% over three years. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

We compared total CEO remuneration at Willis Lease Finance Corporation with the amount paid at companies with a similar market capitalization. As discussed above, we discovered that the company pays more than the median of that group.

Importantly, though, the company has impressed with its earnings per share growth, over three years. In addition, shareholders have done well over the same time period. So, considering this good performance, the CEO compensation may be quite appropriate. Whatever your view on compensation, you might want to check if insiders are buying or selling Willis Lease Finance shares (free trial).

If you want to buy a stock that is better than Willis Lease Finance, this free list of high return, low debt companies is a great place to look.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NasdaqGM:WLFC

Willis Lease Finance

Operates as a lessor and servicer of commercial aircraft and aircraft engines worldwide.

Acceptable track record and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3447.6% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7101.1% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.652.3% undervalued

31 followersusers have followed this narrative

2 commentsusers have commented on this narrative

15 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£162.2% undervalued

40 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

IV

Ivoed on Adyen ·

Adyen’s next debate is not about payments growth, but whether its new layers actually become cash flow

Fair Value:€974.8110.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AL

ALL_in on Shenzhen Kaifa Technology ·

$深科技 / 000021.SZ — the chokepoint nobody is pricing in.

Fair Value:CN¥88.9547.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IV

Ivoed on D'Ieteren Group ·

D’Ieteren Group: The Market Still Prices the Belgian Car Cycle, But the Value Sits Elsewhere

Fair Value:€229.9829.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7444.1% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.0% undervalued

60 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1928.5% undervalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative