Advertisement

- India

- /

- Hospitality

- /

- NSEI:TAJGVK

Does TAJGVK Hotels & Resorts (NSE:TAJGVK) Have A Healthy Balance Sheet?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that TAJGVK Hotels & Resorts Limited (NSE:TAJGVK) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for TAJGVK Hotels & Resorts

What Is TAJGVK Hotels & Resorts's Net Debt?

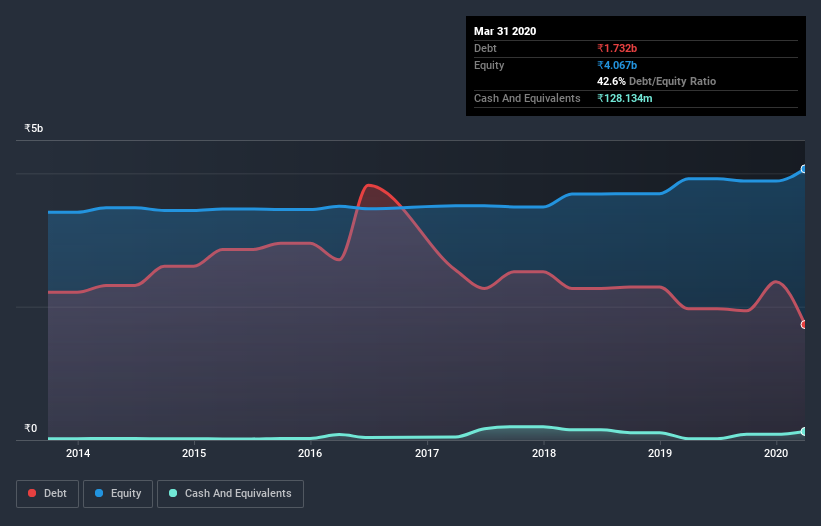

The image below, which you can click on for greater detail, shows that TAJGVK Hotels & Resorts had debt of ₹1.73b at the end of March 2020, a reduction from ₹1.97b over a year. However, it does have ₹128.1m in cash offsetting this, leading to net debt of about ₹1.60b.

How Strong Is TAJGVK Hotels & Resorts's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that TAJGVK Hotels & Resorts had liabilities of ₹831.6m due within 12 months and liabilities of ₹2.48b due beyond that. On the other hand, it had cash of ₹128.1m and ₹156.5m worth of receivables due within a year. So its liabilities total ₹3.0b more than the combination of its cash and short-term receivables.

While this might seem like a lot, it is not so bad since TAJGVK Hotels & Resorts has a market capitalization of ₹9.23b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

TAJGVK Hotels & Resorts's net debt is sitting at a very reasonable 2.2 times its EBITDA, while its EBIT covered its interest expense just 2.6 times last year. While these numbers do not alarm us, it's worth noting that the cost of the company's debt is having a real impact. Importantly TAJGVK Hotels & Resorts's EBIT was essentially flat over the last twelve months. Ideally it can diminish its debt load by kick-starting earnings growth. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine TAJGVK Hotels & Resorts's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we always check how much of that EBIT is translated into free cash flow. Happily for any shareholders, TAJGVK Hotels & Resorts actually produced more free cash flow than EBIT over the last three years. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

On our analysis TAJGVK Hotels & Resorts's conversion of EBIT to free cash flow should signal that it won't have too much trouble with its debt. However, our other observations weren't so heartening. In particular, interest cover gives us cold feet. Considering this range of data points, we think TAJGVK Hotels & Resorts is in a good position to manage its debt levels. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Consider for instance, the ever-present spectre of investment risk. We've identified 2 warning signs with TAJGVK Hotels & Resorts (at least 1 which is concerning) , and understanding them should be part of your investment process.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you’re looking to trade TAJGVK Hotels & Resorts, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if TAJGVK Hotels & Resorts might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:TAJGVK

TAJGVK Hotels & Resorts

Engages in the business of owning, operating, and managing hotels, palaces, and resorts under the TAJ brand in India.

Flawless balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|40.2% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|62.7% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.1% undervalued

UN

Community Contributor