Advertisement

- France

- /

- Gas Utilities

- /

- ENXTPA:RUI

Does Rubis (EPA:RUI) Have A Healthy Balance Sheet?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Rubis (EPA:RUI) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Rubis

What Is Rubis's Debt?

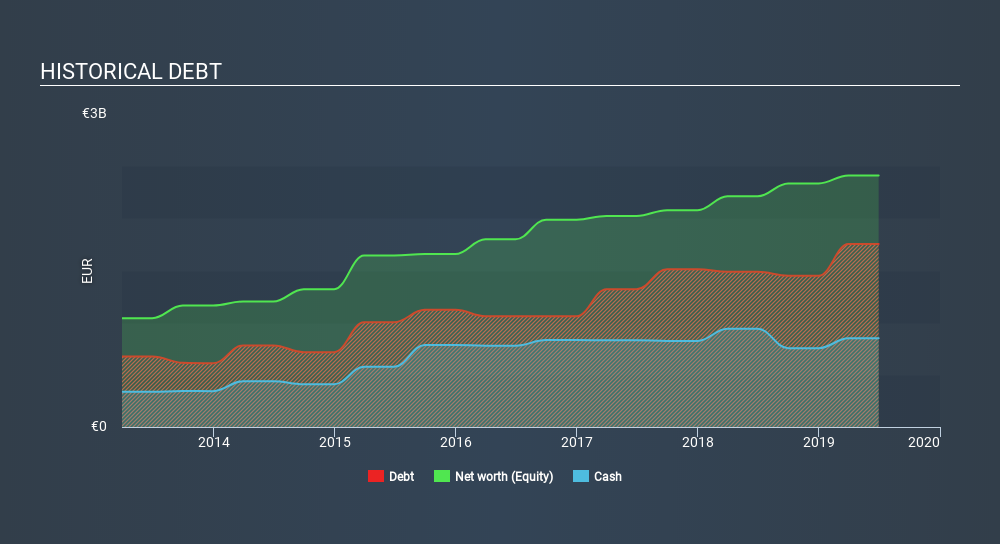

You can click the graphic below for the historical numbers, but it shows that as of June 2019 Rubis had €1.75b of debt, an increase on €1.5k, over one year. However, it does have €849.5m in cash offsetting this, leading to net debt of about €904.3m.

How Strong Is Rubis's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Rubis had liabilities of €1.24b due within 12 months and liabilities of €1.73b due beyond that. On the other hand, it had cash of €849.5m and €752.2m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by €1.38b.

While this might seem like a lot, it is not so bad since Rubis has a market capitalization of €5.65b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Rubis's net debt to EBITDA ratio of about 1.7 suggests only moderate use of debt. And its commanding EBIT of 17.9 times its interest expense, implies the debt load is as light as a peacock feather. Fortunately, Rubis grew its EBIT by 8.3% in the last year, making that debt load look even more manageable. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Rubis's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. In the last three years, Rubis's free cash flow amounted to 23% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

On our analysis Rubis's interest cover should signal that it won't have too much trouble with its debt. However, our other observations weren't so heartening. For instance it seems like it has to struggle a bit to convert EBIT to free cash flow. We would also note that Gas Utilities industry companies like Rubis commonly do use debt without problems. Considering this range of data points, we think Rubis is in a good position to manage its debt levels. Having said that, the load is sufficiently heavy that we would recommend any shareholders keep a close eye on it. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Like risks, for instance. Every company has them, and we've spotted 2 warning signs for Rubis (of which 1 is significant!) you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About ENXTPA:RUI

Rubis

Engages in the energy distribution business in Europe, Africa, and the Caribbean.

6 star dividend payer and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

DA

davidlsander on Nevgold ·

The U.S. Government Is Desperate for This Metal. This Tiny Miner Has It -- Its Closest Peer Is Already Worth Double.

Fair Value:US$2.1943.7% undervalued

49 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7720.5% undervalued

26 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9218.9% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$1909.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

OO

OOO97 on QXO ·

QXO aims for $24B revenue by 2031 with AI-driven margin expansion (Priced for good execution)

Fair Value:US$32.5357.1% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

danmad on Sonic Healthcare ·

Sonic Healthcare is poised for large upside as margins recover

Fair Value:AU$2721.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CE

CentryResearch on DraftKings ·

DraftKings: Priced for Pessimism, But Are the Risks Fully Priced In?

Fair Value:US$20.9713.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75028.2% undervalued

98 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.1% undervalued

67 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5449.8% undervalued

64 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

BE

benjamin_lvieq on PayPal Holdings ·

An investment case is not about loving the product. Its about price vs reality.

2

|0

ST

StoxEurope on Koninklijke Ahold Delhaize ·

I ran Ahold Delhaize through a three-model triangulation — DCF, dividend discount, and residual inco...

1

|0