Advertisement

- United States

- /

- Insurance

- /

- NasdaqCM:OXBR

Does Oxbridge Re Holdings Limited's (NASDAQ:OXBR) CEO Salary Reflect Performance?

In 2013 Jay Madhu was appointed CEO of Oxbridge Re Holdings Limited (NASDAQ:OXBR). This analysis aims first to contrast CEO compensation with other companies that have similar market capitalization. After that, we will consider the growth in the business. And finally - as a second measure of performance - we will look at the returns shareholders have received over the last few years. This method should give us information to assess how appropriately the company pays the CEO.

See our latest analysis for Oxbridge Re Holdings

How Does Jay Madhu's Compensation Compare With Similar Sized Companies?

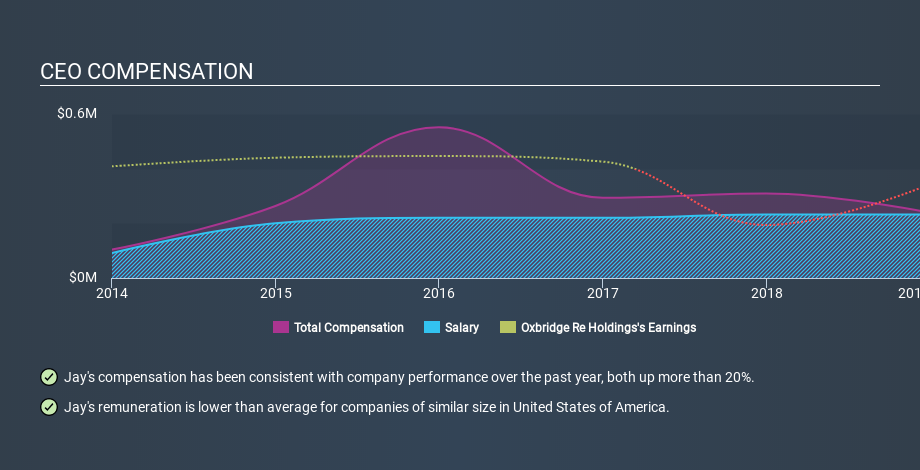

Our data indicates that Oxbridge Re Holdings Limited is worth US$5.1m, and total annual CEO compensation was reported as US$239k for the year to December 2018. Notably, the salary of US$232k is the vast majority of the CEO compensation. We looked at a group of companies with market capitalizations under US$200m, and the median CEO total compensation was US$502k.

This would give shareholders a good impression of the company, since most similar size companies have to pay more, leaving less for shareholders. However, before we heap on the praise, we should delve deeper to understand business performance.

The graphic below shows how CEO compensation at Oxbridge Re Holdings has changed from year to year.

Is Oxbridge Re Holdings Limited Growing?

On average over the last three years, Oxbridge Re Holdings Limited has shrunk earnings per share by 30% each year (measured with a line of best fit). The trailing twelve months of revenue was pretty much the same as the prior period.

Unfortunately, earnings per share have trended lower over the last three years. And the flat revenue hardly impresses. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Although we don't have analyst forecasts you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Oxbridge Re Holdings Limited Been A Good Investment?

Since shareholders would have lost about 82% over three years, some Oxbridge Re Holdings Limited shareholders would surely be feeling negative emotions. So shareholders would probably think the company shouldn't be too generous with CEO compensation.

In Summary...

Oxbridge Re Holdings Limited is currently paying its CEO below what is normal for companies of its size.

Shareholders should note that compensation for Jay Madhu is under the median of a group of similar sized companies. But then, EPS growth is lacking and so are the returns to shareholders. We would not call the pay too generous, but nor would we claim the CEO is underpaid, given lacklustre business performance. So you may want to check if insiders are buying Oxbridge Re Holdings shares with their own money (free access).

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies, that have HIGH return on equity and low debt.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqCM:OXBR

Oxbridge Re Holdings

Through its subsidiaries, provides specialty property and casualty reinsurance solutions.

Excellent balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.562.2% undervalued

35 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.828.9% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23059.6% overvalued

39 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32039.9% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

GE

Germaine on Kucingko Berhad ·

Kucingko Berhad: Fundamentals Show Early Recovery as Creative Content Expansion Gains Traction

Fair Value:RM 0.012691.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

Blagget on BP Silver ·

“valer un Potosí” GOOGLE IT. Now you’re should be kinda locked in. Educate yourself, Read the rest.

Fair Value:CA$685.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TimLee on Master Tec Group Berhad ·

Master Tec’s TNB Extension Reinforces Its Utility-Scale Growth Story

Fair Value:RM 1.6841.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.1% undervalued

84 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9630.8% undervalued

64 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5457.5% undervalued

59 followersusers have followed this narrative

3 commentsusers have commented on this narrative

10 likesusers have liked this narrative