Advertisement

- United States

- /

- Energy Services

- /

- NasdaqGS:KLXE

Does KLX Energy Services Holdings (NASDAQ:KLXE) Have A Healthy Balance Sheet?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that KLX Energy Services Holdings, Inc. (NASDAQ:KLXE) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for KLX Energy Services Holdings

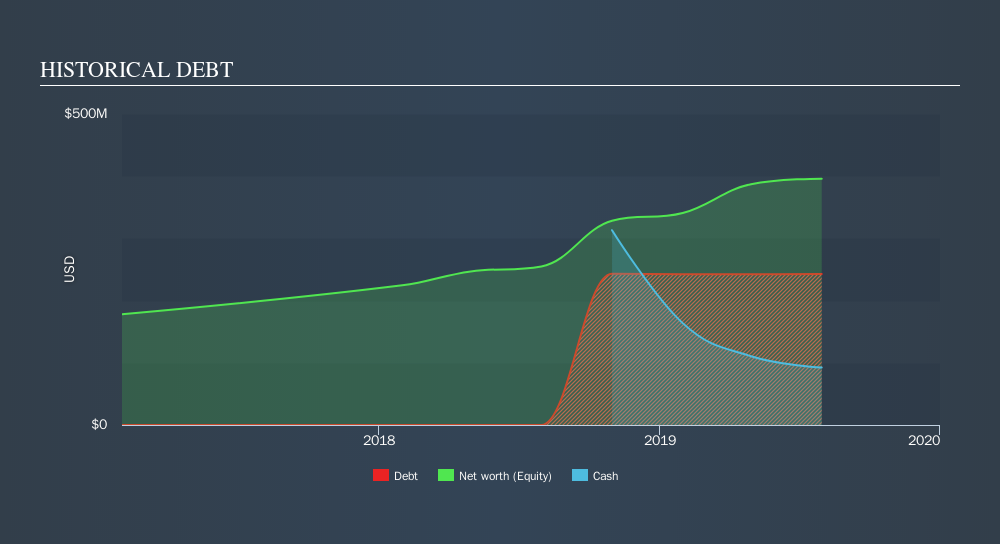

What Is KLX Energy Services Holdings's Net Debt?

The image below, which you can click on for greater detail, shows that at July 2019 KLX Energy Services Holdings had debt of US$242.6m, up from none in one year. However, because it has a cash reserve of US$92.4m, its net debt is less, at about US$150.2m.

How Healthy Is KLX Energy Services Holdings's Balance Sheet?

According to the last reported balance sheet, KLX Energy Services Holdings had liabilities of US$82.3m due within 12 months, and liabilities of US$254.9m due beyond 12 months. Offsetting these obligations, it had cash of US$92.4m as well as receivables valued at US$153.4m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$91.4m.

This deficit isn't so bad because KLX Energy Services Holdings is worth US$187.4m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

KLX Energy Services Holdings has a very low debt to EBITDA ratio of 1.5 so it is strange to see weak interest coverage, with last year's EBIT being only 2.2 times the interest expense. So one way or the other, it's clear the debt levels are not trivial. Pleasingly, KLX Energy Services Holdings is growing its EBIT faster than former Australian PM Bob Hawke downs a yard glass, boasting a 169% gain in the last twelve months. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if KLX Energy Services Holdings can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last two years, KLX Energy Services Holdings saw substantial negative free cash flow, in total. While that may be a result of expenditure for growth, it does make the debt far more risky.

Our View

KLX Energy Services Holdings's conversion of EBIT to free cash flow and interest cover definitely weigh on it, in our esteem. But its EBIT growth rate tells a very different story, and suggests some resilience. Taking the abovementioned factors together we do think KLX Energy Services Holdings's debt poses some risks to the business. So while that leverage does boost returns on equity, we wouldn't really want to see it increase from here. Given our hesitation about the stock, it would be good to know if KLX Energy Services Holdings insiders have sold any shares recently. You click here to find out if insiders have sold recently.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NasdaqGS:KLXE

KLX Energy Services Holdings

Provides drilling, completions, production, and well intervention services and products to the onshore oil and gas producing regions of the United States.

Medium-low and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|38.6% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|8.8% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.0% undervalued

BL

Community Contributor