Advertisement

Does Dollarama Inc.'s (TSE:DOL) CEO Pay Matter?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Neil Rossy became the CEO of Dollarama Inc. (TSE:DOL) in 2016. This analysis aims first to contrast CEO compensation with other large companies. Then we'll look at a snap shot of the business growth. And finally we will reflect on how common stockholders have fared in the last few years, as a secondary measure of performance. This process should give us an idea about how appropriately the CEO is paid.

Check out our latest analysis for Dollarama

How Does Neil Rossy's Compensation Compare With Similar Sized Companies?

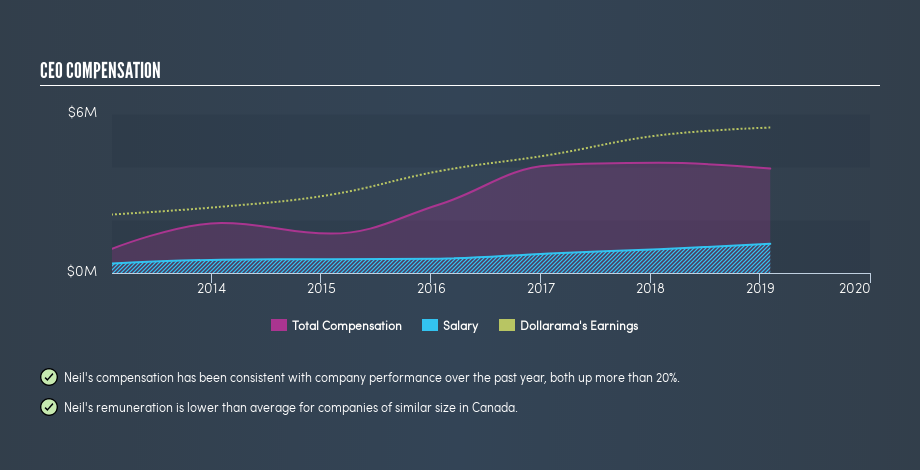

Our data indicates that Dollarama Inc. is worth CA$15b, and total annual CEO compensation is CA$3.9m. (This figure is for the year to February 2019). That's actually a decrease on the year before. While we always look at total compensation first, we note that the salary component is less, at CA$1.1m. We looked at a group of companies with market capitalizations over CA$10b and the median CEO total compensation was CA$9.1m. (We took a wide range because the CEOs of massive companies tend to be paid similar amounts - even though some are quite a bit bigger than others).

Most shareholders would consider it a positive that Neil Rossy takes less in total compensation than the CEOs of most other large companies, leaving more for shareholders. While this is a good thing, you'll need to understand the business better before you can form an opinion.

You can see a visual representation of the CEO compensation at Dollarama, below.

Is Dollarama Inc. Growing?

Dollarama Inc. has increased its earnings per share (EPS) by an average of 16% a year, over the last three years (using a line of best fit). Its revenue is up 9.0% over last year.

This demonstrates that the company has been improving recently. A good result. It's nice to see a little revenue growth, as this is consistent with healthy business conditions.

Has Dollarama Inc. Been A Good Investment?

I think that the total shareholder return of 52%, over three years, would leave most Dollarama Inc. shareholders smiling. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

In Summary...

Dollarama Inc. is currently paying its CEO below what is normal for large companies. Many would consider this to indicate that the pay is modest since the business is growing. The strong history of shareholder returns might even have some thinking that Neil Rossy deserves a raise!

It's not often we see shareholders do so well, and yet the CEO is paid modestly. It would be even more positive if company insiders are buying shares. Shareholders may want to check for free if Dollarama insiders are buying or selling shares.

Important note: Dollarama may not be the best stock to buy. You might find something better in this list of interesting companies with high ROE and low debt.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About TSX:DOL

Dollarama

Operates a chain of stores and provides related logistical and administrative support activities.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Unicycive Therapeutics ·

Looking to be second time lucky with a game-changing new product

Fair Value:US$21.5361.6% undervalued

139 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

DE

Degen_GCR on Everpure ·

Second order memory play likely to double in a year

Fair Value:US$18054.9% undervalued

23 followersusers have followed this narrative

1 commentusers have commented on this narrative

15 likesusers have liked this narrative

DO

Double_Bubbler on Intuitive Machines ·

Intuitive Machines: To The Moon and Beyond!

Fair Value:US$42.319.9% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

YI

yiannisz on AppLovin ·

AppLovin’s AI Engine Is Printing Profit

Fair Value:US$989.2449.4% undervalued

33 followersusers have followed this narrative

2 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

KA

kapirey on STIF Société anonyme ·

STIF Société anonyme will achieve 14% revenue growth with a focus on future gains

Fair Value:€43.6317.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Palantir Technologies ·

Palantir is strategic geopolitical asset at the intersection of AI, defense, and Western alliances.

Fair Value:US$120.1411.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Village Farms International ·

VFF is a vertically integrated, low-cost cannabis producer

Fair Value:US$4.7244.7% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.6% undervalued

111 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74017.0% undervalued

38 followersusers have followed this narrative

3 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6116.1% undervalued

1182 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative