Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:SASR

Do You Like Sandy Spring Bancorp, Inc. (NASDAQ:SASR) At This P/E Ratio?

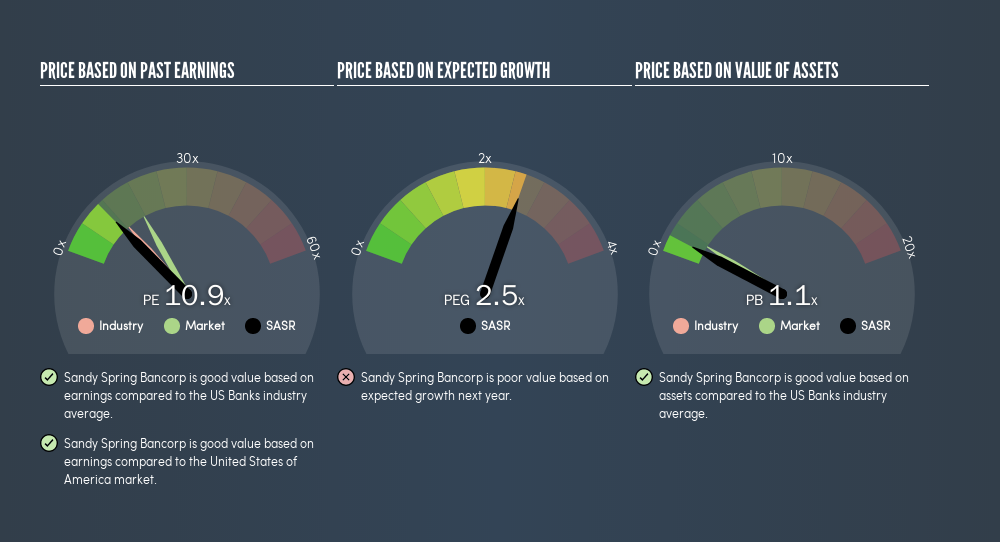

This article is for investors who would like to improve their understanding of price to earnings ratios (P/E ratios). We'll show how you can use Sandy Spring Bancorp, Inc.'s (NASDAQ:SASR) P/E ratio to inform your assessment of the investment opportunity. Sandy Spring Bancorp has a price to earnings ratio of 10.89, based on the last twelve months. That means that at current prices, buyers pay $10.89 for every $1 in trailing yearly profits.

View our latest analysis for Sandy Spring Bancorp

How Do You Calculate A P/E Ratio?

The formula for price to earnings is:

Price to Earnings Ratio = Share Price ÷ Earnings per Share (EPS)

Or for Sandy Spring Bancorp:

P/E of 10.89 = $34.56 ÷ $3.17 (Based on the year to June 2019.)

Is A High P/E Ratio Good?

A higher P/E ratio means that investors are paying a higher price for each $1 of company earnings. That is not a good or a bad thing per se, but a high P/E does imply buyers are optimistic about the future.

How Does Sandy Spring Bancorp's P/E Ratio Compare To Its Peers?

One good way to get a quick read on what market participants expect of a company is to look at its P/E ratio. The image below shows that Sandy Spring Bancorp has a lower P/E than the average (12.3) P/E for companies in the banks industry.

This suggests that market participants think Sandy Spring Bancorp will underperform other companies in its industry.

How Growth Rates Impact P/E Ratios

Generally speaking the rate of earnings growth has a profound impact on a company's P/E multiple. That's because companies that grow earnings per share quickly will rapidly increase the 'E' in the equation. That means unless the share price increases, the P/E will reduce in a few years. Then, a lower P/E should attract more buyers, pushing the share price up.

Sandy Spring Bancorp increased earnings per share by a whopping 37% last year. And earnings per share have improved by 15% annually, over the last five years. With that performance, I would expect it to have an above average P/E ratio.

Remember: P/E Ratios Don't Consider The Balance Sheet

One drawback of using a P/E ratio is that it considers market capitalization, but not the balance sheet. That means it doesn't take debt or cash into account. Theoretically, a business can improve its earnings (and produce a lower P/E in the future) by investing in growth. That means taking on debt (or spending its cash).

While growth expenditure doesn't always pay off, the point is that it is a good option to have; but one that the P/E ratio ignores.

Sandy Spring Bancorp's Balance Sheet

Net debt is 44% of Sandy Spring Bancorp's market cap. While that's enough to warrant consideration, it doesn't really concern us.

The Verdict On Sandy Spring Bancorp's P/E Ratio

Sandy Spring Bancorp's P/E is 10.9 which is below average (17.2) in the US market. The company hasn't stretched its balance sheet, and earnings growth was good last year. If it continues to grow, then the current low P/E may prove to be unjustified.

When the market is wrong about a stock, it gives savvy investors an opportunity. As value investor Benjamin Graham famously said, 'In the short run, the market is a voting machine but in the long run, it is a weighing machine.' So this free report on the analyst consensus forecasts could help you make a master move on this stock.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with modest (or no) debt, trading on a P/E below 20.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NasdaqGS:SASR

Sandy Spring Bancorp

Operates as the bank holding company for Sandy Spring Bank that provides commercial and retail banking, mortgage, private banking, and trust services in the United States.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Eva Live ·

This small cap is building the AI workforce of the future

Fair Value:US$7.4351.3% undervalued

76 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

26 followersusers have followed this narrative

6 commentsusers have commented on this narrative

27 likesusers have liked this narrative

WO

woodworthfund on Kraft Heinz ·

Kraft Heinz (KHC): Less Drama, More Ketchup

Fair Value:US$3532.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

CA

Canderous on PetroTal ·

Beyond 2026, Beyond a Double

Fair Value:CA$1.8166.9% undervalued

28 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

WA

wahyud on Perusahaan Perkebunan London Sumatra Indonesia ·

LSIP Revenue to Rise a Whopping 43.92% Amid Market Dynamics

Fair Value:Rp3.6k63.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WA

wahyud on Charoen Pokphand Indonesia ·

Charoen Pokphand Indonesia will soar with a 12.94% growth and a 10.67x future P/E

Fair Value:Rp4.53k4.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WA

wahyud on Medco Energi Internasional ·

Medco Energi's Revenue Will Increase by 2.45% Doors Opening

Fair Value:Rp1.75k23.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8590.4% undervalued

113 followersusers have followed this narrative

2 commentsusers have commented on this narrative

31 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6119.8% undervalued

1194 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.2% undervalued

26 followersusers have followed this narrative

6 commentsusers have commented on this narrative

27 likesusers have liked this narrative