Advertisement

- United Kingdom

- /

- Office REITs

- /

- LSE:DLN

Derwent London Plc (LON:DLN): Set To Experience A Decrease In Earnings?

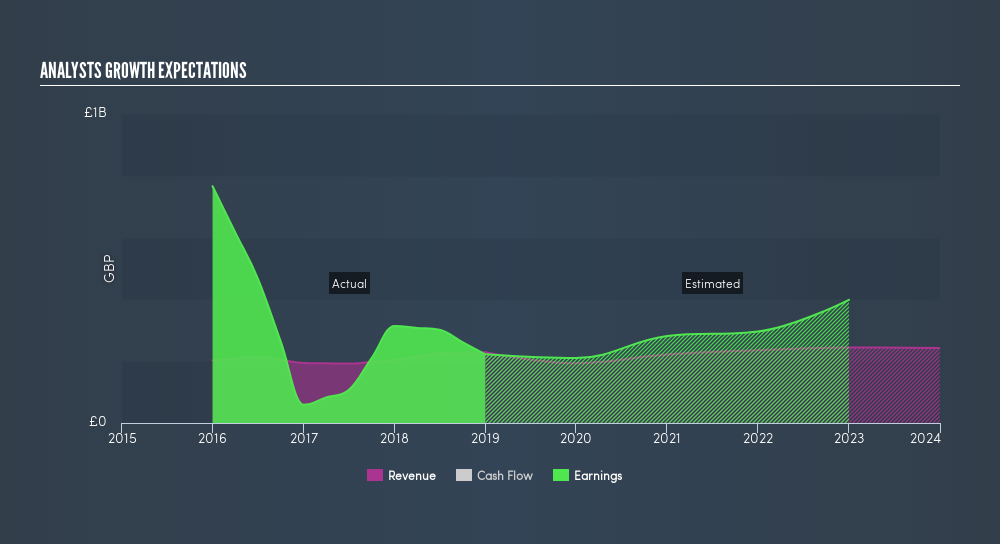

In December 2018, Derwent London Plc (LON:DLN) released its earnings update. Generally, the consensus outlook from analysts appear pessimistic, with earnings expected to decline by 5.4% in the upcoming year. However, compared to its 5-year track record of the average earnings growth rate of -25%, this is still an improvement. With trailing-twelve-month net income at current levels of UK£222m, the consensus growth rate suggests that earnings will decline to UK£210m by 2020. In this article, I've outline a few earnings growth rates to give you a sense of the market sentiment for Derwent London in the longer term. Investors wanting to learn more about other aspects of the company should research its fundamentals here.

View our latest analysis for Derwent London

Can we expect Derwent London to keep growing?

The longer term view from the 9 analysts covering DLN is one of positive sentiment. Broker analysts tend to forecast up to three years ahead due to a lack of clarity around the business trajectory beyond this. I've plotted out each year's earnings expectations and inserted a line of best fit to calculate an annual growth rate from the slope in order to understand the overall trajectory of DLN's earnings growth over these next few years.

By 2022, DLN's earnings should reach UK£296m, from current levels of UK£222m, resulting in an annual growth rate of 13%. This leads to an EPS of £2.66 in the final year of projections relative to the current EPS of £1.99. Margins are currently sitting at 97%, which is expected to expand to 126% by 2022.

Next Steps:

Future outlook is only one aspect when you're building an investment case for a stock. For Derwent London, I've compiled three essential factors you should look at:

- Financial Health: Does it have a healthy balance sheet? Take a look at our free balance sheet analysis with six simple checks on key factors like leverage and risk.

- Valuation: What is Derwent London worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether Derwent London is currently mispriced by the market.

- Other High-Growth Alternatives : Are there other high-growth stocks you could be holding instead of Derwent London? Explore our interactive list of stocks with large growth potential to get an idea of what else is out there you may be missing!

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About LSE:DLN

Derwent London

Derwent London plc owns a commercial real estate portfolio predominantly in central London valued at 5.2 billion euros as at 30 June 2025, making it the largest London office-focused real estate investment trust (REIT).

Average dividend payer and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

112 followersusers have followed this narrative

1 commentusers have commented on this narrative

20 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9819.4% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

29 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1559.0% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3650.4% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

CR

CrayonDave on New Found Gold ·

The Birth of a High-Grade Canadian Gold Powerhouse

Fair Value:US$5.0850.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

Kallan on Zip Co ·

Fundamental Analysis on BNPL companies should be viewed differently for Valuation Metrics.

Fair Value:AU$2.5537.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HE

Henrynuke03 on Nigerian Exchange Group ·

Future Growth Awaits NGXGROUP with New High-Profile Listings

Fair Value:₦105.2977.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.5% undervalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59632.1% undervalued

1305 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0226.5% undervalued

1102 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative

Trending Discussion

DA

daqui_luis on Corticeira Amorim S.G.P.S ·

Great analysis on a great and solid company with a dominant position in the Cork Market.

0

|0