Advertisement

- United States

- /

- Banks

- /

- NasdaqGS:CBSH

Commerce Bancshares, Inc. Just Missed EPS By 37%: Here's What Analysts Think Will Happen Next

Investors in Commerce Bancshares, Inc. (NASDAQ:CBSH) had a good week, as its shares rose 5.4% to close at US$58.22 following the release of its quarterly results. It looks like a pretty bad result, all things considered. Although revenues of US$328m were in line with analyst predictions, statutory earnings fell badly short, missing estimates by 37% to hit US$0.44 per share. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

See our latest analysis for Commerce Bancshares

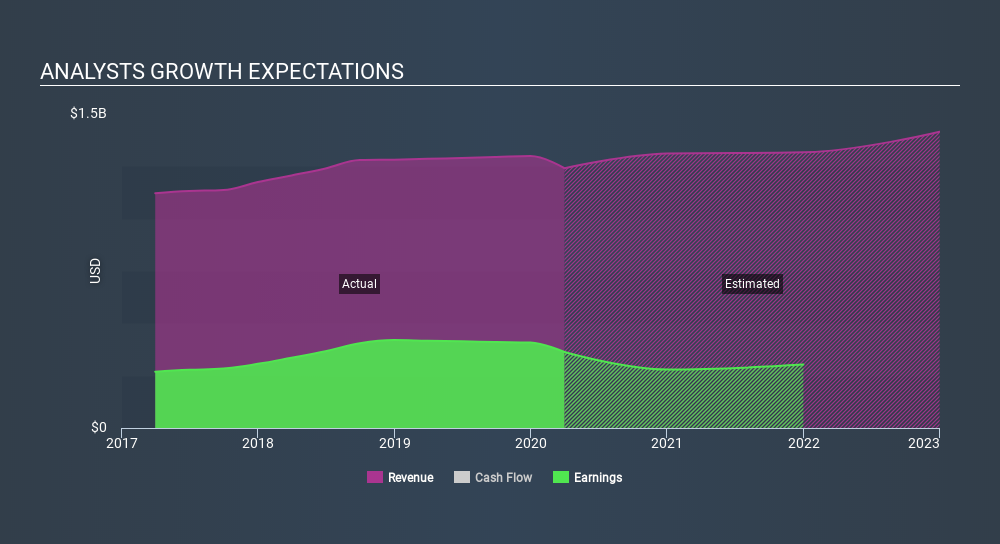

Taking into account the latest results, the consensus forecast from Commerce Bancshares' eight analysts is for revenues of US$1.31b in 2020, which would reflect a modest 5.6% improvement in sales compared to the last 12 months. Statutory earnings per share are expected to dive 20% to US$2.56 in the same period. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$1.31b and earnings per share (EPS) of US$2.82 in 2020. The analysts seem to have become a little more negative on the business after the latest results, given the minor downgrade to their earnings per share numbers for next year.

It might be a surprise to learn that the consensus price target was broadly unchanged at US$54.80, with the analysts clearly implying that the forecast decline in earnings is not expected to have much of an impact on valuation. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. The most optimistic Commerce Bancshares analyst has a price target of US$64.00 per share, while the most pessimistic values it at US$35.00. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We can infer from the latest estimates that forecasts expect a continuation of Commerce Bancshares'historical trends, as next year's 5.6% revenue growth is roughly in line with 5.1% annual revenue growth over the past five years. Compare this with the wider industry, which analyst estimates (in aggregate) suggest will see revenues grow 2.8% next year. So although Commerce Bancshares is expected to maintain its revenue growth rate, it's definitely expected to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Fortunately, they also reconfirmed their revenue numbers, suggesting sales are tracking in line with expectations - and our data suggests that revenues are expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple Commerce Bancshares analysts - going out to 2022, and you can see them free on our platform here.

Plus, you should also learn about the 1 warning sign we've spotted with Commerce Bancshares .

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NasdaqGS:CBSH

Commerce Bancshares

Operates as the bank holding company for Commerce Bank that provides retail, mortgage banking, corporate, investment, trust, and asset management products and services to individuals and businesses in the United States.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor