Advertisement

- United States

- /

- Chemicals

- /

- NYSE:CF

CF Industries Holdings (NYSE:CF) Has A Pretty Healthy Balance Sheet

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk'. So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, CF Industries Holdings, Inc. (NYSE:CF) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for CF Industries Holdings

What Is CF Industries Holdings's Net Debt?

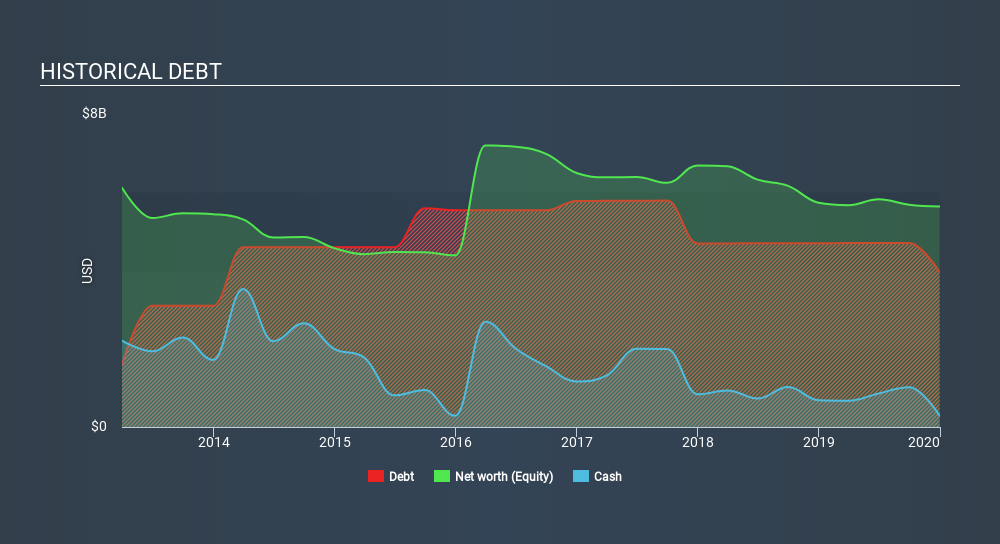

You can click the graphic below for the historical numbers, but it shows that CF Industries Holdings had US$3.96b of debt in December 2019, down from US$4.70b, one year before. However, it does have US$287.0m in cash offsetting this, leading to net debt of about US$3.67b.

A Look At CF Industries Holdings's Liabilities

Zooming in on the latest balance sheet data, we can see that CF Industries Holdings had liabilities of US$665.0m due within 12 months and liabilities of US$5.87b due beyond that. On the other hand, it had cash of US$287.0m and US$242.0m worth of receivables due within a year. So it has liabilities totalling US$6.01b more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company's market capitalization of US$4.60b, we think shareholders really should watch CF Industries Holdings's debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

CF Industries Holdings's net debt is sitting at a very reasonable 2.0 times its EBITDA, while its EBIT covered its interest expense just 4.3 times last year. While these numbers do not alarm us, it's worth noting that the cost of the company's debt is having a real impact. We note that CF Industries Holdings grew its EBIT by 29% in the last year, and that should make it easier to pay down debt, going forward. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine CF Industries Holdings's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Happily for any shareholders, CF Industries Holdings actually produced more free cash flow than EBIT over the last three years. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

Both CF Industries Holdings's ability to to convert EBIT to free cash flow and its EBIT growth rate gave us comfort that it can handle its debt. In contrast, our confidence was undermined by its apparent struggle to handle its total liabilities. When we consider all the factors mentioned above, we do feel a bit cautious about CF Industries Holdings's use of debt. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 3 warning signs for CF Industries Holdings you should be aware of, and 1 of them can't be ignored.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:CF

CF Industries Holdings

Engages in the production of ammonia in North America, Europe, and internationally.

Outstanding track record, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1158.7% undervalued

32 followersusers have followed this narrative

2 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7721.6% undervalued

49 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9220.2% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$1908.3% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

Recently Updated Narratives

RE

Reex on Unibap Space Solutions ·

Long-term bet on Europe's strategic space autonomy (2030–2055)

Fair Value:SEK 36.0176.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AV

Averagemike on Samsara ·

Samsara's Future PE Will Soar to 337.7x and the Future is Bright

Fair Value:US$57.34k99.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

John_Eric on ServiceNow ·

The Company Nobody Brags About

Fair Value:US$266.0164.1% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75029.1% undervalued

103 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6514.6% undervalued

69 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5449.5% undervalued

64 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

PI

PittTheYounger on International Consolidated Airlines Group ·

IAG is a surefire investment in the airline space, once and if the Iran War is finally over in the sense of a lasting peace agreement or at least a reliable ceasefire. Before that, however and by the same token, IAG ranks among the most vulnerable if spring's kerosene fears return to the fore, as is very likely right now.

0

|0

ST

stephen_iwu3c on CK Hutchison Holdings ·

Hutchsion 3 UK has been sold to vodafone, why is there an integration costs, is the analysis outdated?

0

|0