Advertisement

- United Kingdom

- /

- Commercial Services

- /

- LSE:BIFF

Biffa (LON:BIFF) Shareholders Have Enjoyed A 62% Share Price Gain

By buying an index fund, investors can approximate the average market return. But if you pick the right individual stocks, you could make more than that. For example, Biffa plc (LON:BIFF) shareholders have seen the share price rise 62% over three years, well in excess of the market return (3.8%, not including dividends).

View our latest analysis for Biffa

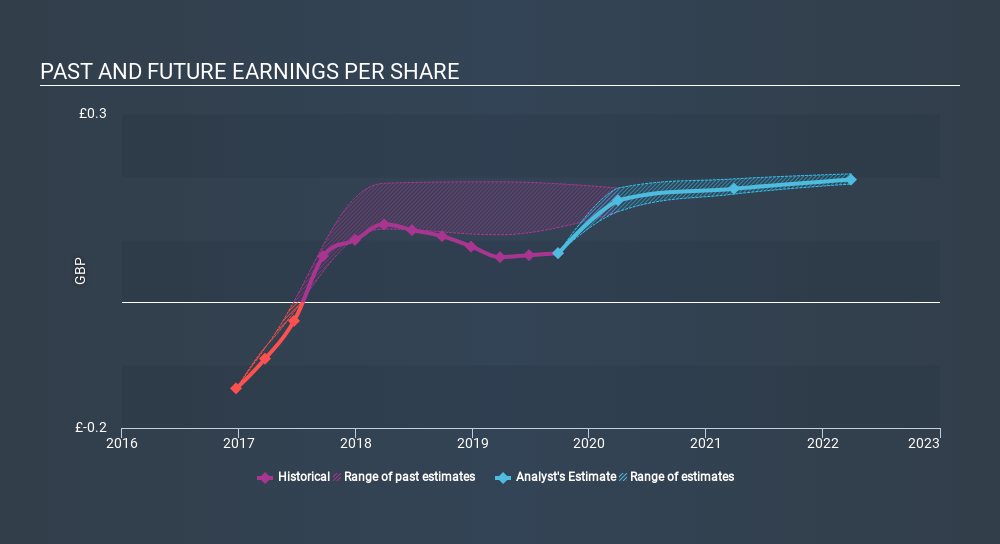

While markets are a powerful pricing mechanism, share prices reflect investor sentiment, not just underlying business performance. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

During three years of share price growth, Biffa moved from a loss to profitability. So we would expect a higher share price over the period.

The image below shows how EPS has tracked over time (if you click on the image you can see greater detail).

We consider it positive that insiders have made significant purchases in the last year. Even so, future earnings will be far more important to whether current shareholders make money. Before buying or selling a stock, we always recommend a close examination of historic growth trends, available here..

What About Dividends?

When looking at investment returns, it is important to consider the difference between total shareholder return (TSR) and share price return. The TSR incorporates the value of any spin-offs or discounted capital raisings, along with any dividends, based on the assumption that the dividends are reinvested. So for companies that pay a generous dividend, the TSR is often a lot higher than the share price return. We note that for Biffa the TSR over the last 3 years was 76%, which is better than the share price return mentioned above. The dividends paid by the company have thusly boosted the total shareholder return.

A Different Perspective

We're pleased to report that Biffa rewarded shareholders with a total shareholder return of 66% over the last year. That includes the value of the dividend. So this year's TSR was actually better than the three-year TSR (annualized) of 21%. Given the track record of solid returns over varying time frames, it might be worth putting Biffa on your watchlist. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. To that end, you should learn about the 2 warning signs we've spotted with Biffa (including 1 which is shouldn't be ignored) .

There are plenty of other companies that have insiders buying up shares. You probably do not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on GB exchanges.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About LSE:BIFF

Biffa

Biffa plc provides waste management services in the United Kingdom.

Reasonable growth potential with questionable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56054.5% undervalued

61 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.6% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

AN

AntonioS on CAR Group ·

CAR Group. A wonderful compounding franchise at a fair-not-cheap price.

Fair Value:AU$3219.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GA

GaryB on Palantir Technologies ·

Palantir hits 52 week low.

Fair Value:US$274.861.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NO

North49_ on iShares - iShares MSCI South Korea ETF ·

EWY:US NYSE Arca iShares Msci South Korea ETF, an opportunity to diversify your tech investments.

Fair Value:US$273.4525.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative