- United States

- /

- Professional Services

- /

- NYSE:RHI

Be Sure To Check Out Robert Half International Inc. (NYSE:RHI) Before It Goes Ex-Dividend

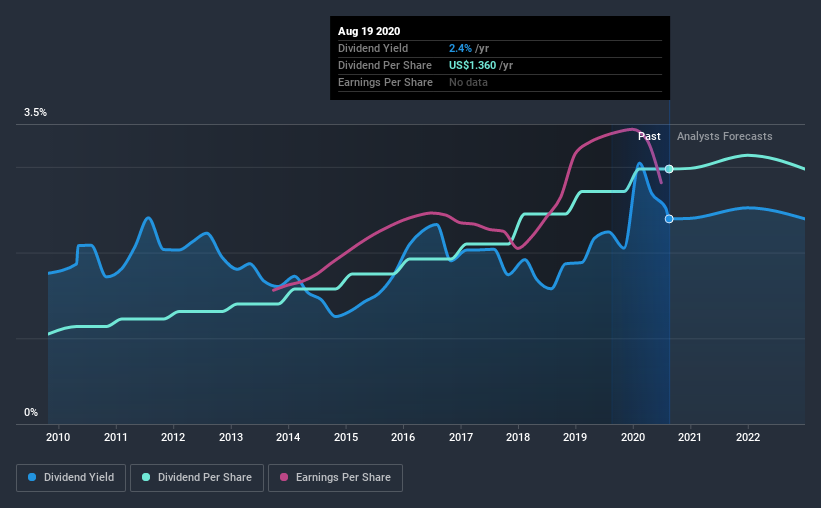

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Robert Half International Inc. (NYSE:RHI) is about to go ex-dividend in just 4 days. If you purchase the stock on or after the 24th of August, you won't be eligible to receive this dividend, when it is paid on the 15th of September.

Robert Half International's upcoming dividend is US$0.34 a share, following on from the last 12 months, when the company distributed a total of US$1.36 per share to shareholders. Based on the last year's worth of payments, Robert Half International has a trailing yield of 2.4% on the current stock price of $56.83. If you buy this business for its dividend, you should have an idea of whether Robert Half International's dividend is reliable and sustainable. So we need to investigate whether Robert Half International can afford its dividend, and if the dividend could grow.

See our latest analysis for Robert Half International

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. That's why it's good to see Robert Half International paying out a modest 40% of its earnings. A useful secondary check can be to evaluate whether Robert Half International generated enough free cash flow to afford its dividend. Luckily it paid out just 23% of its free cash flow last year.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. This is why it's a relief to see Robert Half International earnings per share are up 7.2% per annum over the last five years. The company is retaining more than half of its earnings within the business, and it has been growing earnings at a decent rate. Organisations that reinvest heavily in themselves typically get stronger over time, which can bring attractive benefits such as stronger earnings and dividends.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Robert Half International has delivered an average of 11% per year annual increase in its dividend, based on the past 10 years of dividend payments. It's encouraging to see the company lifting dividends while earnings are growing, suggesting at least some corporate interest in rewarding shareholders.

The Bottom Line

From a dividend perspective, should investors buy or avoid Robert Half International? Earnings per share have been growing moderately, and Robert Half International is paying out less than half its earnings and cash flow as dividends, which is an attractive combination as it suggests the company is investing in growth. It might be nice to see earnings growing faster, but Robert Half International is being conservative with its dividend payouts and could still perform reasonably over the long run. There's a lot to like about Robert Half International, and we would prioritise taking a closer look at it.

So while Robert Half International looks good from a dividend perspective, it's always worthwhile being up to date with the risks involved in this stock. For example - Robert Half International has 1 warning sign we think you should be aware of.

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

If you’re looking to trade Robert Half International, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NYSE:RHI

Robert Half

Provides talent solutions and business consulting services in the United States and internationally.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion