Advertisement

- United States

- /

- REITS

- /

- NYSE:APTS

Analysts Have Been Trimming Their Preferred Apartment Communities, Inc. Price Target After Its Latest Report

There's been a major selloff in Preferred Apartment Communities, Inc. (NYSE:APTS) shares in the week since it released its full-year report, with the stock down 20% to US$10.00. Revenues came in at US$470m, in line with forecasts and the company reported a statutory loss of US$2.73 per share, roughly in line with expectations. Earnings are an important time for investors, as they can track a company's performance, look at what top analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. We thought readers would find it interesting to see analysts' latest (statutory) post-earnings forecasts for next year.

See our latest analysis for Preferred Apartment Communities

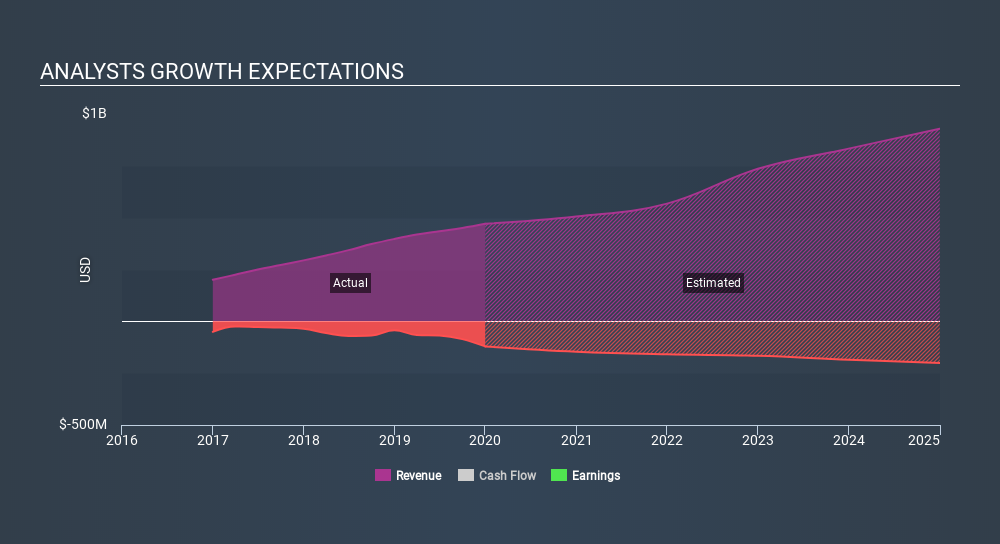

Taking into account the latest results, the current consensus from Preferred Apartment Communities's three analysts is for revenues of US$505.6m in 2020, which would reflect a satisfactory 7.5% increase on its sales over the past 12 months. Statutory losses are expected to reduce, shrinking 13% from last year to US$3.08. Before this earnings announcement, analysts had been forecasting revenues of US$525.6m and losses of US$2.83 per share in 2020. Although analysts have lowered their sales forecasts, they've also made a their earnings per share estimates, which implies there's been something of an uptick in sentiment following the latest results.

The consensus price target fell 20% to US$11.90, with analysts clearly concerned about the company following the weaker revenue and earnings outlook. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on Preferred Apartment Communities, with the most bullish analyst valuing it at US$14.00 and the most bearish at US$10.00 per share. This shows there is still quite a bit of diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

Zooming out to look at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up both against past performance, and against industry growth estimates. It's pretty clear that analysts expect Preferred Apartment Communities's revenue growth will slow down substantially, with revenues next year expected to grow 7.5%, compared to a historical growth rate of 35% over the past five years. By way of comparison, other companies in this market with analyst coverage, are forecast to grow their revenue at 4.9% next year. So it's pretty clear that, while Preferred Apartment Communities's revenue growth is expected to slow, it's still expected to grow faster than the market itself.

The Bottom Line

The most important thing to take away is that analysts reduced their loss per share estimates for next year, perhaps highlighting increased optimism around Preferred Apartment Communities's prospects. Unfortunately analysts also downgraded their revenue estimates, although industry data suggests that Preferred Apartment Communities's revenues are expected to grow faster than the wider market. The consensus price target fell measurably, with analysts seemingly not reassured by the latest results, leading to a lower estimate of Preferred Apartment Communities's future valuation.

Still, the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple Preferred Apartment Communities analysts - going out to 2024, and you can see them free on our platform here.

It might also be worth considering whether Preferred Apartment Communities's debt load is appropriate, using our debt analysis tools on the Simply Wall St platform, here.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:APTS

Preferred Apartment Communities

Preferred Apartment Communities, Inc. (NYSE: APTS) is a real estate investment trust engaged primarily in the ownership and operation of Class A multifamily properties, with select investments in grocery anchored shopping centers, Class A office buildings, and student housing properties.

Fair value with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% undervalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|45.0% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.4% undervalued

TI

Community Contributor