Advertisement

- Sweden

- /

- Trade Distributors

- /

- OM:BERG B

A Sliding Share Price Has Us Looking At Bergman & Beving AB (publ)'s (STO:BERG B) P/E Ratio

To the annoyance of some shareholders, Bergman & Beving (STO:BERG B) shares are down a considerable 34% in the last month. Indeed the recent decline has arguably caused some bitterness for shareholders who have held through the 51% drop over twelve months.

Assuming nothing else has changed, a lower share price makes a stock more attractive to potential buyers. While the market sentiment towards a stock is very changeable, in the long run, the share price will tend to move in the same direction as earnings per share. The implication here is that long term investors have an opportunity when expectations of a company are too low. Perhaps the simplest way to get a read on investors' expectations of a business is to look at its Price to Earnings Ratio (PE Ratio). A high P/E implies that investors have high expectations of what a company can achieve compared to a company with a low P/E ratio.

View our latest analysis for Bergman & Beving

Does Bergman & Beving Have A Relatively High Or Low P/E For Its Industry?

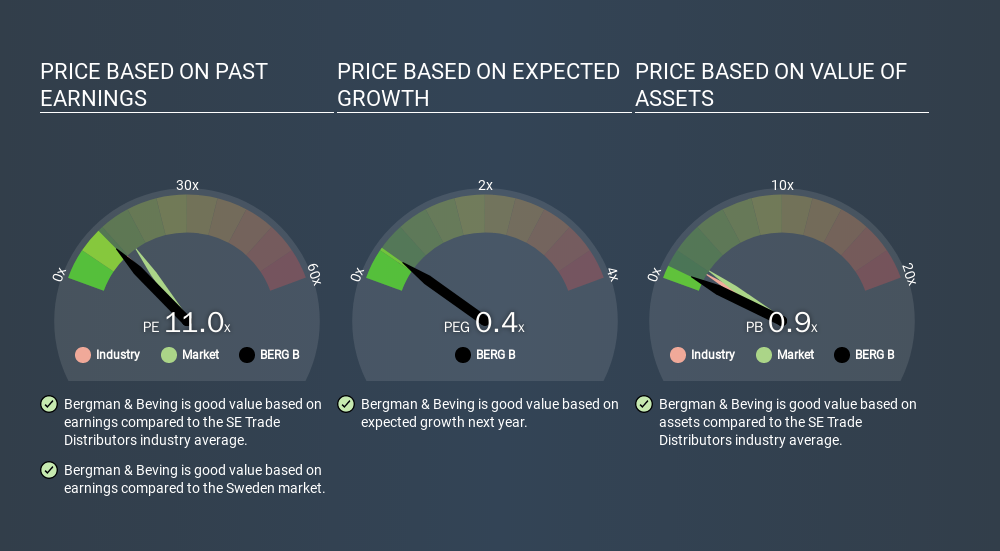

Bergman & Beving's P/E is 10.98. You can see in the image below that the average P/E (10.6) for companies in the trade distributors industry is roughly the same as Bergman & Beving's P/E.

Bergman & Beving's P/E tells us that market participants think its prospects are roughly in line with its industry. So if Bergman & Beving actually outperforms its peers going forward, that should be a positive for the share price. I would further inform my view by checking insider buying and selling., among other things.

How Growth Rates Impact P/E Ratios

When earnings fall, the 'E' decreases, over time. That means unless the share price falls, the P/E will increase in a few years. Then, a higher P/E might scare off shareholders, pushing the share price down.

Bergman & Beving saw earnings per share decrease by 27% last year. And EPS is down 16% a year, over the last 5 years. This could justify a pessimistic P/E.

Remember: P/E Ratios Don't Consider The Balance Sheet

One drawback of using a P/E ratio is that it considers market capitalization, but not the balance sheet. That means it doesn't take debt or cash into account. Theoretically, a business can improve its earnings (and produce a lower P/E in the future) by investing in growth. That means taking on debt (or spending its cash).

Such spending might be good or bad, overall, but the key point here is that you need to look at debt to understand the P/E ratio in context.

Bergman & Beving's Balance Sheet

Net debt is 43% of Bergman & Beving's market cap. While it's worth keeping this in mind, it isn't a worry.

The Bottom Line On Bergman & Beving's P/E Ratio

Bergman & Beving's P/E is 11.0 which is below average (13.8) in the SE market. With only modest debt, it's likely the lack of EPS growth at least partially explains the pessimism implied by the P/E ratio. What can be absolutely certain is that the market has become significantly less optimistic about Bergman & Beving over the last month, with the P/E ratio falling from 16.7 back then to 11.0 today. For those who prefer to invest with the flow of momentum, that might be a bad sign, but for a contrarian, it may signal opportunity.

When the market is wrong about a stock, it gives savvy investors an opportunity. If the reality for a company is not as bad as the P/E ratio indicates, then the share price should increase as the market realizes this. So this free report on the analyst consensus forecasts could help you make a master move on this stock.

Of course you might be able to find a better stock than Bergman & Beving. So you may wish to see this free collection of other companies that have grown earnings strongly.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About OM:BERG B

Bergman & Beving

Provides solutions for the manufacturing and construction sectors in Sweden, Norway, Finland, and internationally.

Reasonable growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|29.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.8% undervalued

AG

Community Contributor