Advertisement

- United Kingdom

- /

- Specialty Stores

- /

- LSE:DNLM

A Look At Dunelm Group plc's (LON:DNLM) Exceptional Fundamentals

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Building up an investment case requires looking at a stock holistically. Today I've chosen to put the spotlight on Dunelm Group plc (LON:DNLM) due to its excellent fundamentals in more than one area. DNLM is a financially-healthy , dividend-paying company with an impressive history of performance. In the following section, I expand a bit more on these key aspects. For those interested in understanding where the figures come from and want to see the analysis, read the full report on Dunelm Group here.

Established dividend payer with adequate balance sheet

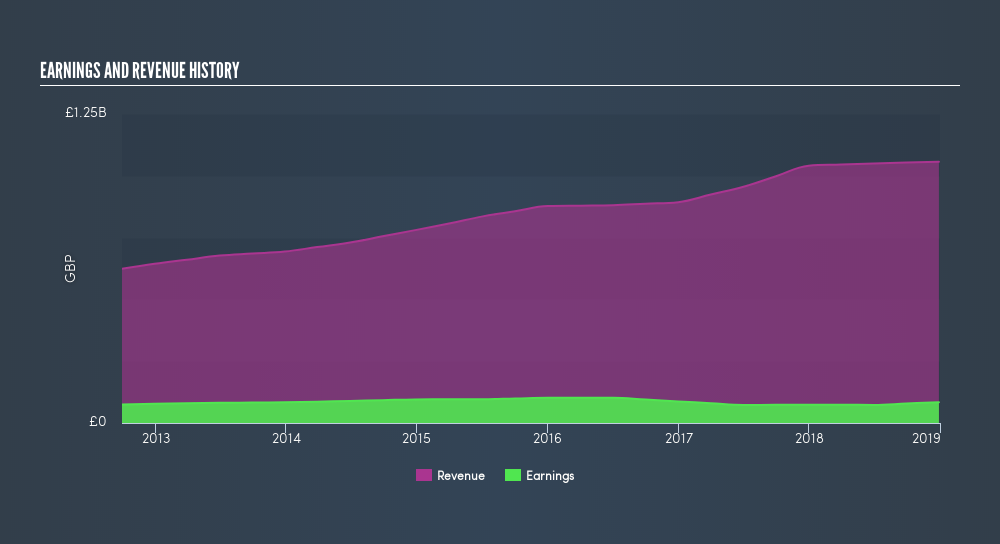

In the previous year, DNLM has ramped up its bottom line by 14%, with its latest earnings level surpassing its average level over the last five years. This strong performance generated a robust double-digit return on equity of 54%, which is an optimistic signal for the future. DNLM is financially robust, with ample cash on hand and short-term investments to meet upcoming liabilities. This implies that DNLM manages its cash and cost levels well, which is a key determinant of the company’s health. DNLM appears to have made good use of debt, producing operating cash levels of 1.55x total debt in the prior year. This is a strong indication that debt is reasonably met with cash generated.

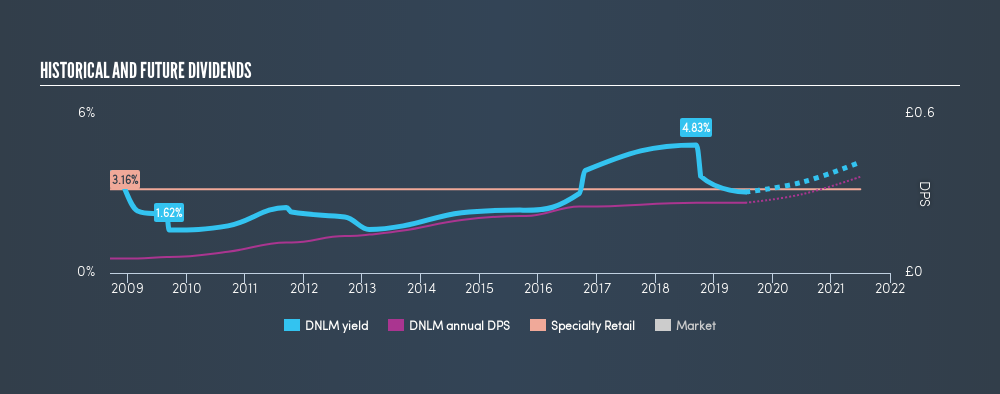

Income investors would also be happy to know that DNLM is a great dividend company, with a current yield standing at 3.1%. DNLM has also been regularly increasing its dividend payments to shareholders over the past decade.

Next Steps:

For Dunelm Group, I've put together three important aspects you should further examine:

- Future Outlook: What are well-informed industry analysts predicting for DNLM’s future growth? Take a look at our free research report of analyst consensus for DNLM’s outlook.

- Valuation: What is DNLM worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether DNLM is currently mispriced by the market.

- Other Attractive Alternatives : Are there other well-rounded stocks you could be holding instead of DNLM? Explore our interactive list of stocks with large potential to get an idea of what else is out there you may be missing!

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About LSE:DNLM

Dunelm Group

Engages in the retail of homewares in the United Kingdom.

Very undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.551.6% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$58016.4% overvalued

27 followersusers have followed this narrative

3 commentsusers have commented on this narrative

28 likesusers have liked this narrative

TH

TheBestInvestor on Lockheed Martin ·

Orbit + Aero + Defense

Fair Value:US$673.8823.8% undervalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on Steppe Gold ·

A case for Steppe Gold, bear case CAD $4, base case CAD $15, bull case CAD $25

Fair Value:CA$2594.4% undervalued

21 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

LE

lexdrew1 on GE Vernova ·

GE Vernova revenue will grow by 13% with a future PE of 64.7x

Fair Value:US$1.17k2.2% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Ubisoft Entertainment ·

Is Ubisoft the Market’s Biggest Pricing Error? Why Forensic Value Points to €33 Per Share

Fair Value:€33.886.0% undervalued

78 followersusers have followed this narrative

7 commentsusers have commented on this narrative

1 likeusers have liked this narrative

RO

RockeTeller on Thor Explorations ·

West Africa's 20 Baggers Gold Play (Nigeria/Senegal)

Fair Value:CA$3295.7% undervalued

11 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3957.5% overvalued

52 followersusers have followed this narrative

3 commentsusers have commented on this narrative

43 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.231.8% undervalued

65 followersusers have followed this narrative

2 commentsusers have commented on this narrative

23 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$579.5726.7% undervalued

1387 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

TA

Taurustunez88 on Dangote Sugar Refinery ·

With the N500b rights issue, I believe Dangote sugar refinery’s loss due to FX pressures will be dra...

1

|0

CL

Claysikes on Taiwan Semiconductor Manufacturing ·

Geopolitical risks balance a monopoly with current and future demand - Pricing in that risk is the c...

0

|0