Last Update 17 Mar 26

Fair value Increased 2.89%COST: Membership Headwinds And Rich P E Will Shape Cautious Outlook

Costco Wholesale's intrinsic value estimate has been lifted by about $23 to $822.59 per share as analysts factor in higher long term price targets, supported by consistent same store sales execution, resilient traffic and ticket trends, recurring membership income growth, and views that the warehouse model remains a core holding for many portfolios despite a premium P/E multiple and membership growth headwinds flagged in some recent research.

Analyst Commentary

Recent research on Costco Wholesale centers on strong operational execution and consistent earnings beats, alongside ongoing debate about how much of that quality is already reflected in the share price. Several firms have raised price targets following Q2 and Q4 results, citing solid comparable sales, healthy traffic trends, and robust membership income.

Some large institutions, such as JPMorgan, emphasize that Costco's core story remains intact, with the underlying business described as strong and supported by unit growth opportunities. Other research points to Q2 earnings that were characterized as robust, with gross margin expansion, 14% membership income growth, and comp traffic up 3.1% worldwide. These views generally see Costco as a core holding within the retail sector.

Other analysts highlight specific operating metrics, such as 7.4% Q2 comparable sales growth, driven by 3.1% traffic growth and 4.2% ticket growth. These data points are often cited as support for higher price targets and continued confidence in Costco's ability to maintain its warehouse club model and membership economics.

At the same time, not all research is uniformly positive. Some firms maintain more neutral or cautious ratings even while lifting price targets, pointing to membership growth as a headwind and limited room for execution missteps at current valuation levels. There are also bearish views that question the durability of certain sales benefits and express concern about future quarters if current supports fade.

For investors, the key takeaway from this mixed commentary is that Costco's execution and membership model receive broad recognition, but there is less agreement on how much to pay for that quality and how much growth remains embedded in current expectations.

Bearish Takeaways

- Bearish analysts point to membership growth as a headwind and argue that for Costco's P/E multiple to expand further, investors may want to see a clear inflection in member additions rather than relying on pricing or ticket growth alone.

- Some bearish views highlight that the current valuation leaves limited room for execution errors, meaning any slowdown in same store sales, traffic, or membership income could lead to a sharper reaction if expectations are not met.

- Cautious research flags the risk that recent strong quarters, including Q2 beats, set a high bar for future performance, which could pressure the stock if comparable sales growth, ticket growth, or margin trends soften.

- Where bearish analysts see temporary factors supporting recent sales, such as timing related benefits, there is concern that these could reverse in later months, creating a more challenging backdrop for sustaining current growth and margins.

What's in the News

- Costco is named among more than 1,400 importers that have sued for refunds of tariffs paid under former U.S. President Donald Trump's emergency trade measures, following a U.S. Supreme Court ruling that the duties were unlawful (Reuters).

- Walmart owned Sam's Club is reported to have a larger warehouse club footprint than Costco in China, with 60 stores compared with Costco's seven. This highlights different international growth paths in that market (Wall Street Journal).

- Costco, Sesame, and IVI RMA North America launched a partnership that gives Costco members access to fertility care coordination, diagnostic workups, referrals to specialty clinics, and member pricing on fertility medications filled by Costco pharmacies.

- Instacart expanded its partnership with Costco into Europe, powering new same day delivery websites for Costco members in France and Spain that offer delivery from all warehouses in those countries.

- Costco is the subject of a nationwide class action lawsuit in the U.S. alleging that its Kirkland Signature Seasoned Rotisserie Chicken is falsely advertised as containing no preservatives, with claims brought under consumer protection laws in Washington and California.

Valuation Changes

- Fair Value: The updated intrinsic value estimate has moved from $799.51 to $822.59 per share, a change of about $23.

- Discount Rate: The discount rate has edged up slightly from 6.96% to 6.98%.

- Revenue Growth: The assumed long term annual revenue growth rate has shifted from 6.75% to 6.37%.

- Net Profit Margin: The assumed net profit margin has adjusted from 3.10% to 3.18%.

- Future P/E: The future P/E multiple used in the model has moved modestly from 40.96x to 40.74x.

Key Takeaways

- Evolving consumer behavior and urban demographics threaten Costco's bulk-sales model, risking slower same-store growth and long-term margin pressure.

- Rising costs and global expansion challenges could compress margins, while membership growth stagnates in mature markets, limiting future earnings potential.

- Expanding global presence, strong membership growth, private label innovation, e-commerce investments, and operational efficiency initiatives are driving stable revenue streams and sustainable margin improvement.

Catalysts

About Costco Wholesale- Engages in the operation of membership warehouses in the United States, Puerto Rico, Canada, Mexico, Japan, the United Kingdom, Korea, Australia, Taiwan, China, Spain, France, Iceland, New Zealand, and Sweden.

- Ongoing shifts toward e-commerce and alternative payment/loyalty platforms threaten Costco's traditional membership-based warehouse model, potentially capping future same-store sales growth and leading to lower renewal rates, which would directly impact both top-line revenue expansion and the stability of membership income.

- The increasing urbanization and reduction in average household size across developed markets is eroding demand for bulk purchasing, weakening one of Costco's core revenue drivers and making its value proposition less compelling to a growing portion of consumers, thereby risking slower comparable sales growth and pressure on long-term margins.

- Membership growth in mature markets is beginning to plateau, as acknowledged by the company's focus on strategic cannibalization and infill to relieve high-volume locations, indicating a saturation point that will constrain revenue expansion and could lead to lower overall earnings growth as opportunities for meaningful U.S. membership gains dwindle.

- Persistently rising labor costs, supply chain complexities, and heightened compliance costs-in an environment where price markups are already limited-will increasingly compress net margins, especially as global regulation and labor practices come under closer scrutiny, threatening Costco's historical margin stability.

- International expansion carries mounting risks, including cultural barriers, regulatory hurdles, and variable renewal rates in foreign markets that typically trail the U.S. These factors could dilute profitability, reduce returns on invested capital, and create volatility in future earnings growth, undermining the company's ability to sustain historic levels of financial performance.

Costco Wholesale Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Costco Wholesale compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Costco Wholesale's revenue will grow by 3.9% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 2.9% today to 3.2% in 3 years time.

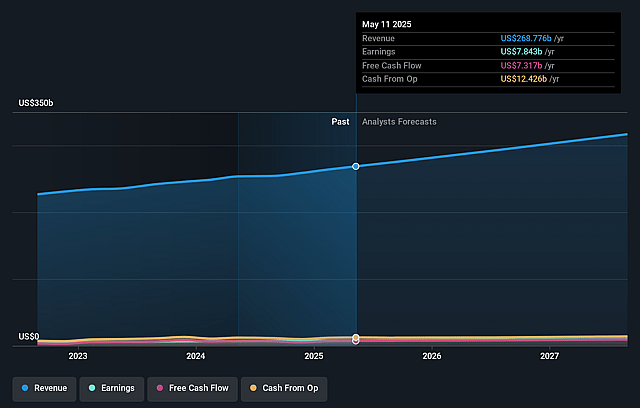

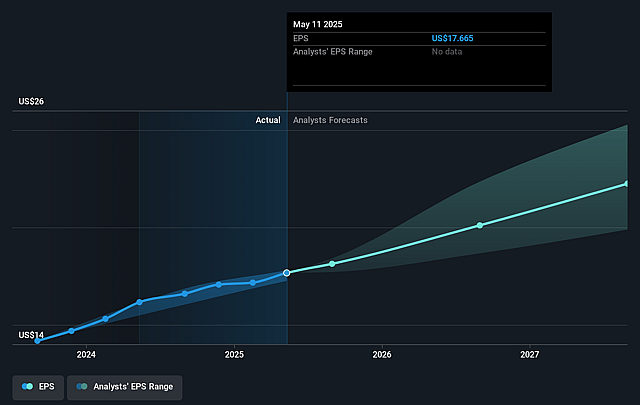

- The bearish analysts expect earnings to reach $9.5 billion (and earnings per share of $21.6) by about September 2028, up from $7.8 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 47.3x on those 2028 earnings, down from 54.1x today. This future PE is greater than the current PE for the US Consumer Retailing industry at 21.7x.

- Analysts expect the number of shares outstanding to grow by 0.09% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.78%, as per the Simply Wall St company report.

Costco Wholesale Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Strong and consistent membership growth, with paid household members and executive memberships both rising at robust rates, points toward stable and expanding high-margin recurring revenue, positively impacting overall earnings and net margins.

- Continued international expansion, particularly with new warehouses in markets like Japan, Korea, Sweden, and Canada, is broadening Costco's global footprint and diversifying revenue streams, reducing reliance on the U.S. for revenue and supporting long-term top-line growth.

- Sustained strength and innovation within the Kirkland Signature private label, including margin improvements and successful local sourcing strategies, both lower costs and enhance differentiation, supporting gross margin expansion and strengthening pricing power over time.

- Accelerating digital and e-commerce capabilities-demonstrated by double-digit e-commerce growth, investment in Costco Logistics, new personalized digital features, and partnerships enabling Buy Now, Pay Later-are increasing member engagement and driving omnichannel sales, which can lead to higher revenue and customer retention.

- Ongoing investments in operational efficiency, technology improvements (such as digital checkout and inventory planning), and supply chain optimization are likely to mitigate cost pressures and support continuous improvement in net margins and operating income.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Costco Wholesale is $834.56, which represents two standard deviations below the consensus price target of $1072.67. This valuation is based on what can be assumed as the expectations of Costco Wholesale's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $1225.0, and the most bearish reporting a price target of just $620.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $301.3 billion, earnings will come to $9.5 billion, and it would be trading on a PE ratio of 47.3x, assuming you use a discount rate of 6.8%.

- Given the current share price of $956.29, the bearish analyst price target of $834.56 is 14.6% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Costco Wholesale?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.