Last Update 30 Dec 25

Fair value Increased 0.011%PayPal Stock: The Shift From Growth at Any Cost to Payments With Discipline

PayPal (NASDAQ: PYPL) has spent the past two years doing something the market often demands but rarely rewards in real time: resetting expectations. After a long stretch defined by rapid user expansion and sprawling product initiatives, the company is refocusing on fundamentals—transaction margins, operating leverage, and capital returns.

The core question for investors is no longer whether PayPal can process payments at scale. It clearly can. The question is whether PayPal can convert that scale into durable profitability in a payments landscape that is more competitive and fragmented than ever.

Payments Are Ubiquitous—Margins Are Not

Digital payments have become table stakes. Consumers expect seamless checkout, instant transfers, and wallet integrations across devices and platforms. That ubiquity has lowered switching friction and intensified competition from card networks, banks, tech platforms, and embedded finance providers.

PayPal’s advantage is not exclusivity—it is breadth. The company operates across branded checkout, unbranded processing, Venmo, Braintree, and merchant services. Each serves a different use case, and together they create a diversified revenue mix. However, not all volume is created equal. Some transactions carry thin margins, while others generate meaningful contribution profit.

PayPal’s recent strategic emphasis reflects this reality: fewer distractions, more focus on profitable flows.

Expert Insight: The Turnaround Is About Quality, Not Speed

According to Andrew Gosselin, Senior Contributor at Save My Cent, PayPal’s turnaround should be evaluated less on headline growth and more on earnings quality. He notes that for years, the company optimized for volume and engagement, often at the expense of margin clarity.

Gosselin emphasizes that PayPal’s renewed focus on transaction margin dollars, cost discipline, and shareholder returns signals a maturing business rather than a declining one. In his view, payments platforms that survive long term are those that balance scale with unit economics—especially as competition compresses pricing. The market’s patience, he argues, will ultimately hinge on consistency, not acceleration.

This perspective reframes PayPal’s recent strategy as consolidation rather than retreat.

Branded vs. Unbranded: A Strategic Tradeoff

One of PayPal’s most important internal debates centers on branded checkout versus unbranded processing. Branded PayPal buttons command higher margins and stronger consumer recognition, but growth has slowed. Unbranded services like Braintree grow faster, particularly with large merchants, but at lower margins.

Rather than choosing one over the other, PayPal is leaning into optimization—improving take rates, reducing fraud, and upselling value-added services. Over time, even small improvements in margin efficiency across massive transaction volumes can materially impact earnings.

This is a scale game, not a feature race.

Venmo and the Long Tail of Monetization

Venmo remains one of PayPal’s most valuable assets, yet also one of its most debated. User engagement is high, but monetization lags more mature payment products. Management has taken a measured approach, gradually layering in checkout, card usage, and merchant acceptance.

The opportunity is significant, but so is the risk of over-monetizing too quickly. Venmo’s strength lies in cultural relevance and daily usage. Preserving that trust while increasing revenue requires restraint—a theme that increasingly defines PayPal’s strategy across the board.

Capital Returns Signal Confidence

PayPal’s decision to emphasize share repurchases and disciplined capital allocation reflects confidence in its cash-generation ability. Rather than chasing acquisitions or speculative expansion, the company is prioritizing returns on invested capital.

For investors, this marks a shift in narrative. PayPal is no longer asking the market to underwrite a vision of endless growth. It is offering a case for steady cash flow, improving margins, and rational execution.

Valuation and Expectations

PYPL’s valuation reflects skepticism born from past overreach. Expectations are lower, which raises the bar for disappointment but lowers the bar for upside. The stock no longer requires flawless execution—just credible progress.

If PayPal continues to expand transaction margins, manage costs, and return capital consistently, sentiment can improve even without explosive top-line growth.

Conclusion

For investors, PYPL represents a recalibration story. The platform still sits at the center of global digital commerce, but its next chapter will be written in basis points, operating leverage, and discipline. If PayPal executes patiently, the market may eventually reward what it once overlooked: a payments giant learning how to grow up.

As PayPal (PYPL) solidifies its position in the digital payments landscape, it presents a promising opportunity driven by transaction growth, profitability, and an attractive valuation. This analysis delves into how each of these areas contributes to PayPal’s robust potential as an investment.

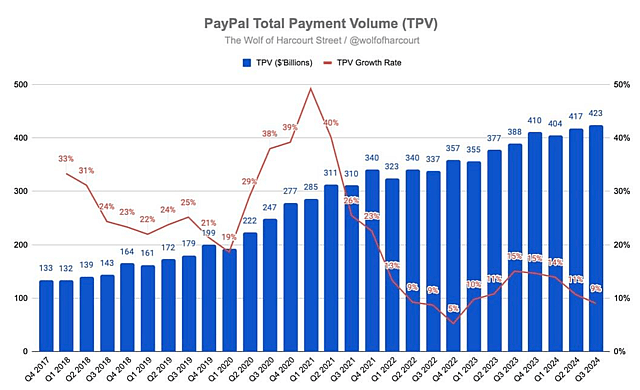

Transaction growth is a cornerstone of PayPal’s continued strength, underpinned by the company’s broad array of services and expanding user base. Since Q1 2022, PayPal’s transaction volume has grown from 5,161 million to 6,631 million by Q3 2024. This increase, amounting to an additional 1,470 million transactions, reflects PayPal’s ability to attract and retain a dedicated customer base across its ecosystem. Stability in transaction frequency is bolstered by brand loyalty, as seen in minor fluctuations in the year-over-year (YoY) transaction growth rate, which has largely remained stable at around 10% after some initial variability.

Much of PayPal’s growth has been driven by the performance of its core products. PayPal’s branded checkout continues to perform strongly, with a YoY growth rate of 6%, supported by large enterprises, marketplaces, and international markets. Venmo, a key driver in the peer-to-peer payments space, has contributed an 8% increase in Total Payment Volume (TPV), further strengthening PayPal’s transaction base. Cross-border transactions have also grown by 7%, fueled by continued demand within Europe, where digital payment adoption is high.

Source: Threads

To further enhance its checkout process, PayPal has recently launched an improved mobile interface that streamlines the checkout experience for consumers, whether using one-time checkouts, recurring payments, or vaulted options. This update has already shown positive results, with a 20% transaction rate increase for one-time purchases through the new interface.

Increasingly, Venmo is expanding beyond peer-to-peer transactions- a further indication that PayPal is working to ensure more touchpoints and greater user engagement by adding more features such as merchant rewards, debit card cashback, and refreshed app experiences. Indeed, the portfolio of services that the PayPal ecosystem represents has become a diverse, rich platform for user engagement, lending to the long-term path to revenue stability.

This is also reflected in PayPal's resiliency in another area: profitability. Although margins have compressed somewhat over the last few quarters, the company has maintained healthy profit margins through cost rationalization. PayPal's transaction margin has averaged around 45-46% for the last two quarters, therefore, after an initial decline from 50.9% in Q1 '22 to 46.6% in Q3 '24. Though the road was somewhat rocky due to strategic cost control, PayPal's profitability was maintained, allowing its non-GAAP EPS in Q3 '24 to rise 22% YoY—a strong 146% improvement from Q1 '22.

PayPal’s strong profitability derives from effective cost control in sales and marketing. PayPal has strategically managed its marketing and sales expenses, with sales and marketing costs dropping by 22% YoY in Q2 2023 and 18% in Q3 2023. However, this expense rose by 17% in Q3 2024, indicating a targeted approach to reinvestment in high-impact areas while maintaining overall efficiency in cost management.

PayPal’s Profitability Push: Tech-Driven Margins Amid Fierce Fintech Competition

Enhanced technology has contributed to PayPal’s profitability by reducing transaction losses and boosting the transaction margin by 115 basis points in Q3 2024. This improvement underscores PayPal’s commitment to minimizing credit risks and fraud-related losses and maintaining its profit margins. Although YoY revenue growth has slowed somewhat, PayPal’s ability to balance operational expenses has enabled it to maintain stable margins. In Q3 2024, revenue grew by 6% YoY, while non-GAAP operating income rose by 18%, demonstrating that PayPal can still deliver profitability even with slower payment volume growth.

Lastly, PayPal faces fierce competition due to the entry of tech giants like Apple, Google, and emerging fintechs offering integrated payment ecosystems, advanced financial products, and seamless user experiences that challenge PayPal’s market share in digital payments. According to the CPA, David Kindness, to remain competitive in the market, PayPal should leverage its vast merchant network, enhance personalization, and develop omnichannel solutions to strengthen its core. By pursuing strategic partnerships, investing in technologies like blockchain and AI, and improving user experience, PayPal can boost its competitive edge. Expanding ‘buy now, pay later’ and entering emerging markets would fuel growth while focusing on security and simplicity, building trust and reinforcing its position as a digital payments leader.

PayPal’s Valuation Discount: A Strategic Buy Opportunity?

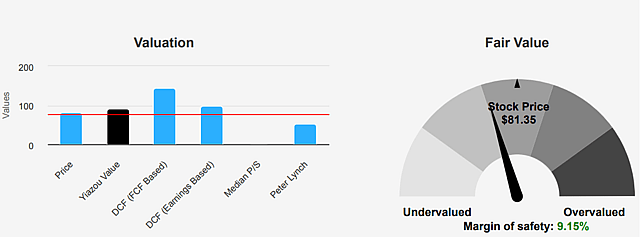

The concept of margin of safety refers to the difference between a stock’s market price and its intrinsic value, offering a cushion for investors against potential downside risks. In PayPal’s case, the intrinsic value is around $90, while the current market price is $81.35. This difference suggests a margin of safety of 9%, meaning investors are potentially paying less than the stock’s estimated worth, which reduces the risk if the company’s growth expectations are not fully met.

Source: yiazou.com

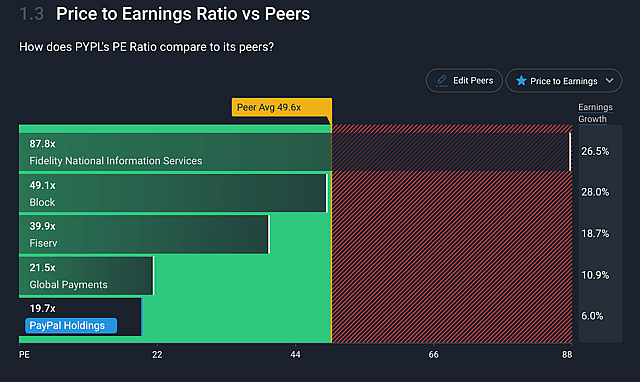

One key reason investors may want to consider an investment in the stock is for valuation purposes. Currently, PayPal trades at a forward price to sales of 2.5 and at a substantial 58.52% discount to its five-year average P/S of 6.03, which could suggest that PayPal is undervalued in the market. In addition, the forward P/E ratio of 17.32, while up 41.73% from the sector median, has yet to reach a commonly accepted discount relative to PayPal's five-year average P/E, which presently trades 43.97% cheaper than its historical average, considering recent pressures on growth.

Source: Simply Wall Street.

In addition to attractive valuation metrics, there is a commitment to creating long-term value from PayPal in its free cash flow and shareholder returns. For Q3 2024, the free cash flow generation by PayPal stood at $1.4 billion, up 31% YoY, underlining strong cash generation capability. During Q3 2024, PayPal returned $1.8 billion to its shareholders through share repurchases, a total of $5.4 billion over twelve months, and decreased outstanding shares by 7%. This capital allocation strategy underpins PayPal's share price and speaks volumes of management's confidence in the company's intrinsic value.

Takeaway

In summary, PayPal's transaction growth, strategic cost control, and generally attractive valuation make it a very attractive investment. The company's ecosystem continues to develop and benefits greatly from user loyalty and significant service diversification. Meanwhile, PayPal can maintain a stable profit margin due to operational efficiency and cost management even if revenue growth slows down.

On a valuation basis, PayPal's metrics reflect an attractive entry point for investors steeped in upside potential against historical and sector benchmarks. Therefore, PayPal combines resilience with upside for investors in the digital payments area, maintaining a balanced risk-reward profile with significant growth possibilities over the coming years.

Have other thoughts on PayPal Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

The user yiannisz holds no position in NasdaqGS:PYPL. Simply Wall St has no position in any of the companies mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The author of this narrative is not affiliated with, nor authorised by Simply Wall St as a sub-authorised representative. This narrative is general in nature and explores scenarios and estimates created by the author. The narrative does not reflect the opinions of Simply Wall St, and the views expressed are the opinion of the author alone, acting on their own behalf. These scenarios are not indicative of the company's future performance and are exploratory in the ideas they cover. The fair value estimates are estimations only, and does not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that the author's analysis may not factor in the latest price-sensitive company announcements or qualitative material.