Last Update15 Oct 25Fair value Increased 1.51%

Analysts have slightly raised their fair value estimate for Gap, increasing the price target from $24.38 to $24.74. This change is due to incremental improvements in profitability and margin potential following positive updates from recent research coverage.

Analyst Commentary

Recent analyst coverage of Gap has highlighted both encouraging momentum and lingering challenges for the company. Valuation updates and rating changes reflect shifting views on Gap's growth prospects, profitability, and sensitivity to broader economic variables.

Bullish Takeaways- Bullish analysts believe Gap’s brands are regaining relevance. This supports opportunities to expand operating margins over the long term, potentially into double digits from current levels.

- Positive comparable sales trends across major banners such as Gap and Old Navy have been cited as evidence of the company’s successful repositioning and improving consumer appeal.

- Some have highlighted recent expansions, particularly into beauty and accessories, as strategic moves that could unlock new growth drivers and diversify revenues. The impact may take time to materialize.

- Upward revisions to price targets and earnings estimates by some bullish analysts reflect incremental improvements in profitability and execution. Recent earnings beats have reinforced this view.

- Bearish analysts remain concerned about tariff-related margin pressures. Gap’s ability to offset increased costs through pricing actions appears limited, particularly in a higher tariff environment.

- Concerns about macroeconomic uncertainty have led to downgrades and reduced price targets. Valuation adjustments reflect lower expectations for operating margin expansion.

- While some acknowledge short-term progress, doubts persist regarding long-term profitability and sustained execution amid ongoing market volatility.

- Recent coverage also highlights the risk that certain growth initiatives, such as category expansions, may take significant time to impact the bottom line and could delay meaningful margin improvement.

What's in the News

- The company completed a share repurchase of 3,434,491 shares between May 4 and August 2, 2025, totaling $81.29 million. Since February 2019, Gap has repurchased 39,828,667 shares for $750.56 million under its ongoing buyback program (Key Developments).

- Gap provided updated earnings guidance for the third quarter and full fiscal year 2025, expecting net sales growth of 1.5% to 2.5% for Q3 and 1% to 2% for the full year compared to the prior year (Key Developments).

- The company announced plans to close approximately 35 net stores during fiscal year 2025 (Key Developments).

Valuation Changes

- The Fair Value Estimate has risen slightly to $24.74 from $24.38 per share, reflecting a modest increase.

- The Discount Rate has increased to 10.07 percent from 9.81 percent, indicating slightly higher perceived risk in the valuation model.

- The Revenue Growth Projection has edged down marginally to 1.75 percent from 1.76 percent.

- The Net Profit Margin Estimate has improved slightly to 5.99 percent from 5.98 percent.

- The future P/E (Price-to-Earnings) Ratio has risen to 12.17x from 11.98x, suggesting higher expectations for future earnings multiples.

Key Takeaways

- Strong value positioning, digital investments, and brand reinvigoration are driving customer engagement, stable demand, and long-term margin expansion.

- Operational discipline, portfolio optimization, and sustainable sourcing initiatives position Gap for future growth and enhanced competitive advantage.

- Persistent operational and strategic challenges-including trade risks, brand underperformance, inventory missteps, and rising competition-threaten profitability, revenue growth, and market positioning.

Catalysts

About Gap- Operates as an apparel retail company.

- Gap's accessible price positioning and demonstrated value focus-seen in Old Navy's consistent category leadership and strong execution in core categories like denim and active-positions the company to benefit from the ongoing shift toward value-conscious consumer behavior, supporting stable demand and revenue growth.

- Ongoing investments in digital technology, supply chain optimization, and omni-channel retail (e.g., tech-driven inventory management, AI in demand planning, modernized media mix) enable Gap to better serve consumers' expectation for seamless integration across digital and physical, driving efficiency gains and supporting margin expansion over the long term.

- Brand reinvigoration strategies (especially at Old Navy, Gap, and Banana Republic), including product innovation, viral marketing campaigns, and strategic collaborations, are producing stronger customer engagement, increased traffic, higher average unit retails (AUR), and improved brand equity-laying a foundation for sustained revenue and earnings growth.

- Continued improvement in cost structure (portfolio rationalization, store optimization, SG&A leverage, disciplined inventory management) and rigorous operational discipline are freeing up capital for growth investments and have supported expanded operating margins despite external pressures like tariffs, with further margin improvement expected as tariff impact is mitigated.

- Gap's leadership in sustainable sourcing, increasing circular initiatives (like resale/collaborative platforms), and supply chain agility align with rising consumer preference for sustainable and ethically-produced apparel as well as industry moves toward integrated, responsive inventory models-providing a strategic differentiator that can enhance long-term competitive positioning and support both top-line growth and gross margin resilience.

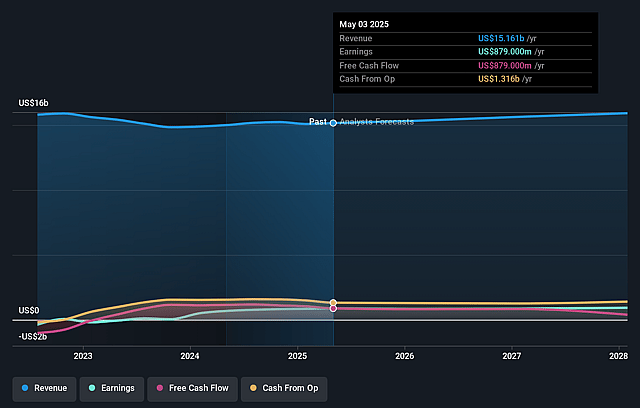

Gap Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Gap's revenue will grow by 1.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.9% today to 6.0% in 3 years time.

- Analysts expect earnings to reach $956.2 million (and earnings per share of $2.69) by about September 2028, up from $889.0 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $808 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 12.0x on those 2028 earnings, up from 10.1x today. This future PE is lower than the current PE for the US Specialty Retail industry at 18.7x.

- Analysts expect the number of shares outstanding to decline by 1.4% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.81%, as per the Simply Wall St company report.

Gap Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Ongoing exposure to tariff headwinds and evolving trade policy poses a structural risk-while mitigation is underway, tariffs have already caused a 100–110 basis point hit to operating margin and $150–175M in lost earnings power, with future trade disputes or escalation potentially creating recurring cost pressure and volatility, impacting net margins and earnings.

- Chronic underperformance and brand execution issues at Athleta, now in a "reset" year with -11% net sales and -9% comps, show continued vulnerability to category misalignment and poor product/marketing fit, risking further revenue stagnation and dragging on consolidated earnings until a turnaround is proven.

- Flat net sales performance company-wide, with only 1% comparable sales growth and a reliance on a few high-performing brands (Gap, Old Navy, Banana Republic), signals limited underlying revenue momentum; this exposes the company to greater risk if demand trends soften, key categories falter, or promotional activity increases.

- Elevated inventory levels (+9% YoY) due to accelerated receipts and higher input costs/tariffs highlight structural inventory management challenges; such issues could force markdowns and aggressive discounting (as seen at Athleta), compressing gross margins and undermining earnings consistency.

- Heightened competitive pressures from fast-fashion and digital-native brands, ongoing shifts toward e-commerce, and changing consumer preferences (including sustainability and experience over goods) continue to threaten Gap's market share, limit international expansion prospects, and increase the need for costly adaptation, posing risk to long-term revenue growth and net margin resilience.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $24.376 for Gap based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $32.0, and the most bearish reporting a price target of just $19.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $16.0 billion, earnings will come to $956.2 million, and it would be trading on a PE ratio of 12.0x, assuming you use a discount rate of 9.8%.

- Given the current share price of $24.1, the analyst price target of $24.38 is 1.1% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.