Last Update 08 Jul 26

Fair value Increased 6.40%SCHW: Record Asset Gathering And AI Tools Will Shape Balanced Outlook

The updated analyst price target for Charles Schwab increases from about $88 to roughly $94, with analysts pointing to clearer revenue and margin guidance, refreshed models following investor day, and greater confidence in client engagement and key growth initiatives.

Analyst Commentary

Recent research on Charles Schwab highlights a mix of optimism around the updated financial outlook and ongoing debate about risk, particularly around valuation, client behavior, and execution on new initiatives. While several firms have adjusted their price targets upward following investor day, there is also a pocket of more cautious commentary that readers should weigh alongside the bullish views.

On the constructive side, several analysts reference clearer guidance on revenue and expenses, refreshed models, and what they see as solid client engagement. Some research notes point to Schwab's fiscal 2026 revenue and expense guidance as an important input for their updated targets, and others emphasize momentum in advisor services, workplace services, and self-directed trading and wealth businesses. Management's framing of AI as a constructive tool for the business, and as a counterpoint to the AI driven "cash optimization" concern, is another area that has drawn attention in analyst reports.

There is also focus on how the Charles Schwab stock traded on the investor day, including a roughly 2% decline on the day in one report despite commentary around revenue guidance and net interest margin. That kind of market reaction is being interpreted by some as a reminder that expectations and positioning matter, even when the company provides more clarity around its outlook.

JPMorgan is cited among the firms adjusting price targets, while other global banks have also made smaller revisions as they incorporate the latest guidance and investor day messaging into their models. Across the board, the core debate centers on how much of Schwab's planned initiatives and updated financial framework are already reflected in the stock price and what that implies for forward returns.

Bearish Takeaways

- Bearish analysts who trimmed price targets in recent months signal concern that Charles Schwab's valuation already embeds a lot of execution success, leaving less room for error if revenue or expense trends differ from the current framework.

- Some of the cautious research flags execution risk around key growth initiatives, such as advisor and workplace services, where slower than expected client adoption or engagement could weigh on long term growth assumptions.

- Reports that mention AI related "cash optimization" pressures indicate a view that client behavior or product mix shifts linked to AI tools could be a drag on balance sheet growth, which bears see as a risk to earnings power.

- The mix of both raised and lowered targets over the period reflects ongoing debate about whether Schwab's updated guidance justifies current multiples, with bearish analysts stressing that any disappointment on revenue, margins, or cost control could lead to further downside risk for the stock.

What’s in the News for Charles Schwab

- Charles Schwab reported record core net new assets of US$49.9b for May 2026, 43% above May 2025, with total client assets at US$13.14b and 461,000 new brokerage accounts opened for the month, according to company data.

- The company passed the Federal Reserve’s 2026 CCAR stress test with a Common Equity Tier 1 ratio of 26.3% as of March 31, 2026. The Federal Reserve kept this ratio above required minimums through an unchanged stress capital buffer, which the company highlighted as supporting a strong capital and regulatory position.

- Schwab outlined a mixed 2026 Mid-Year Market Outlook that points to support for U.S. stocks from business investment. The outlook also flags risks tied to inflation, geopolitics, and potential Federal Reserve rate hikes. Its stock fell over 3% after a hawkish Fed signal and sector-wide selling, according to recent reports.

- Trading platform updates include nearly 24/7 cryptocurrency futures on thinkorswim, broader fractional trading across most U.S. stocks and ETFs with a US$1 minimum, and new research and risk tools on Schwab.com and Schwab Mobile, as disclosed in company product announcements.

- Schwab introduced its first generative AI portfolio insights tool for retail clients, providing day change summaries, holding-level drivers, and curated Schwab research and news in one view. The company frames the tool as a source of information rather than investment advice.

Valuation Changes for Charles Schwab

- Fair Value: The updated fair value estimate for Charles Schwab has risen slightly from $88.00 to about $93.63 per share.

- Discount Rate: The applied discount rate has edged lower from 8.79% to about 8.51%, indicating a modestly different risk or return assumption in the model.

- Revenue Growth: The modeled long term revenue growth rate has fallen significantly from about 9.23% to roughly 5.70%.

- Net Profit Margin: The assumed net profit margin has increased from roughly 36.47% to about 43.38%, implying a higher expected earnings share of each $1 of revenue for Charles Schwab in the model.

- Future P/E: The future P/E assumption has declined from about 17.39x to roughly 14.39x, reflecting a lower valuation multiple applied to projected earnings.

Catalysts

About Charles Schwab

Charles Schwab is a diversified financial services firm providing brokerage, wealth management, banking and advisory solutions to individual investors and independent advisers.

What are the underlying business or industry changes driving this perspective?

- Heavy investment in AI, technology and new platforms such as spot crypto could overshoot sustainable demand. This may lead to structurally higher run-rate technology and personnel spending that compresses operating leverage and erodes pretax margins, even if revenues keep growing.

- Record equity markets, elevated trading volumes and peak margin balances risk reversing as rates fall and volatility normalizes. This could simultaneously reduce net interest revenue, trading revenue and securities lending income, putting pressure on top line growth and earnings.

- Greater reliance on pledged asset lines, margin lending and bank lending to drive growth increases credit and interest rate risk. A downturn or policy shift could slow loan demand, raise loss provisions and materially weaken net interest margin and net income.

- Rapid growth among younger, more digitally native and trading-oriented clients may skew revenue toward cyclical trading and lower-yield cash balances, while requiring sustained content and service investment. This may create a mix shift that limits fee growth and dampens long-term net margins.

- Strategic balance sheet repositioning from high-cost wholesale funding toward new securities and flexible BDA usage may lock in lower yields if the rate-cut path accelerates. This could cap future net interest income growth and constrain earnings expansion despite robust client asset growth.

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on Charles Schwab compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Charles Schwab's revenue will grow by 5.7% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 36.4% today to 43.4% in 3 years time.

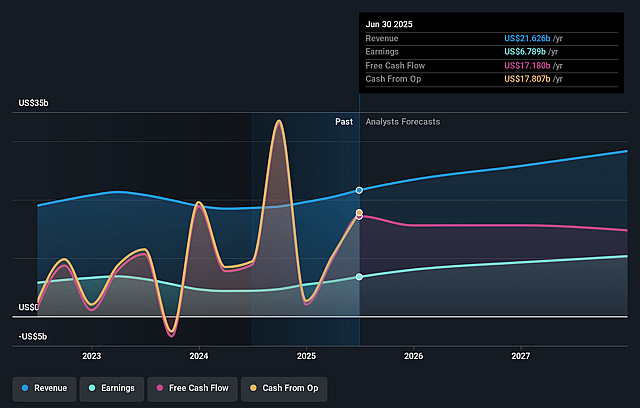

- The bearish analysts expect earnings to reach $12.7 billion (and earnings per share of $6.6) by about July 2029, up from $9.0 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 14.4x on those 2029 earnings, down from 19.7x today. This future PE is lower than the current PE for the US Capital Markets industry at 40.8x.

- The bearish analysts expect the number of shares outstanding to decline by 4.19% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.51%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Sustained client asset growth, including $11.59 trillion of client assets and nearly $356 billion of core net new assets year to date, suggests Schwab may continue to compound its asset base through cycles. This could support long term revenue and earnings growth rather than a structural decline in the share price.

- Secular tailwinds from younger, highly engaged investors, with roughly one third of new to firm retail households coming from Gen Z and a growing share of under 40s using Schwab for financial planning, could underpin durable volume, fee and lending growth that bolsters long term revenue and net margins.

- Ongoing mix shift into higher value wealth, lending and advisory solutions, including record Schwab Wealth Advisory flows, 24% growth in bank lending and 37% growth in pledged asset line balances, may structurally enhance profitability and capital efficiency. This may support resilient net interest income and pretax margins.

- Strategic investments in scale and efficiency, such as AI enabled service tools, expanded digital capabilities and balance sheet optimization, are designed to keep cost to serve low and operating leverage high. This could sustain strong pretax margins and earnings growth even if market conditions soften.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Charles Schwab is $93.63, which represents up to two standard deviations below the consensus price target of $116.68. This valuation is based on what can be assumed as the expectations of Charles Schwab's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $137.0, and the most bearish reporting a price target of just $84.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $29.3 billion, earnings will come to $12.7 billion, and it would be trading on a PE ratio of 14.4x, assuming you use a discount rate of 8.5%.

- Given the current share price of $101.93, the analyst price target of $93.63 is 8.9% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Charles Schwab?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.