Catalysts

About Charles Schwab

Charles Schwab is a diversified financial services firm providing brokerage, wealth management, banking and advisory solutions to individual investors and independent advisers.

What are the underlying business or industry changes driving this perspective?

- Heavy investment in AI, technology and new platforms such as spot crypto could overshoot sustainable demand. This may lead to structurally higher run-rate technology and personnel spending that compresses operating leverage and erodes pretax margins, even if revenues keep growing.

- Record equity markets, elevated trading volumes and peak margin balances risk reversing as rates fall and volatility normalizes. This could simultaneously reduce net interest revenue, trading revenue and securities lending income, putting pressure on top line growth and earnings.

- Greater reliance on pledged asset lines, margin lending and bank lending to drive growth increases credit and interest rate risk. A downturn or policy shift could slow loan demand, raise loss provisions and materially weaken net interest margin and net income.

- Rapid growth among younger, more digitally native and trading-oriented clients may skew revenue toward cyclical trading and lower-yield cash balances, while requiring sustained content and service investment. This may create a mix shift that limits fee growth and dampens long-term net margins.

- Strategic balance sheet repositioning from high-cost wholesale funding toward new securities and flexible BDA usage may lock in lower yields if the rate-cut path accelerates. This could cap future net interest income growth and constrain earnings expansion despite robust client asset growth.

Assumptions

This narrative explores a more pessimistic perspective on Charles Schwab compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts. How have these above catalysts been quantified?

- The bearish analysts are assuming Charles Schwab's revenue will grow by 9.2% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 33.9% today to 36.5% in 3 years time.

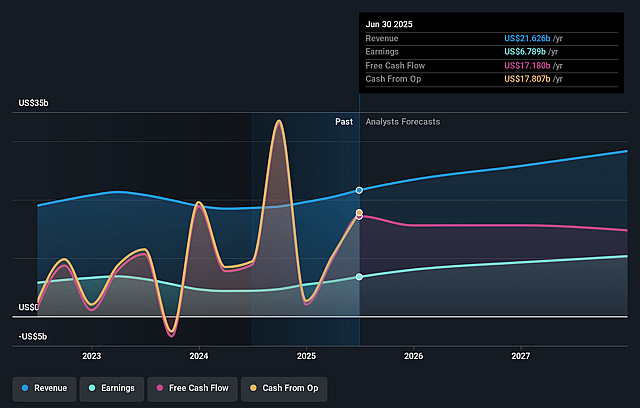

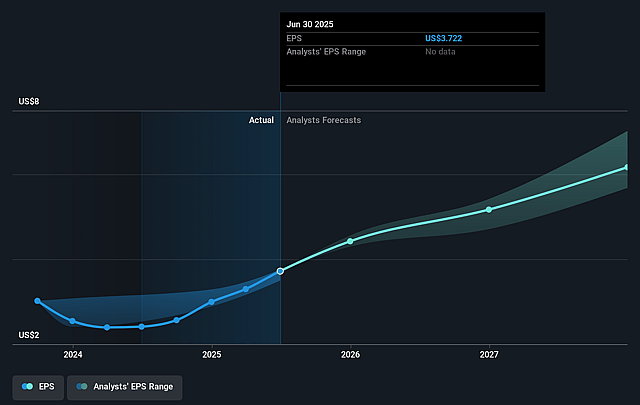

- The bearish analysts expect earnings to reach $10.9 billion (and earnings per share of $6.62) by about December 2028, up from $7.8 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $12.3 billion.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 17.4x on those 2028 earnings, down from 23.2x today. This future PE is lower than the current PE for the US Capital Markets industry at 25.1x.

- The bearish analysts expect the number of shares outstanding to decline by 2.02% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.79%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Sustained client asset growth, including $11.59 trillion of client assets and nearly $356 billion of core net new assets year to date, suggests Schwab may continue to compound its asset base through cycles. This could support long term revenue and earnings growth rather than a structural decline in the share price.

- Secular tailwinds from younger, highly engaged investors, with roughly one third of new to firm retail households coming from Gen Z and a growing share of under 40s using Schwab for financial planning, could underpin durable volume, fee and lending growth that bolsters long term revenue and net margins.

- Ongoing mix shift into higher value wealth, lending and advisory solutions, including record Schwab Wealth Advisory flows, 24% growth in bank lending and 37% growth in pledged asset line balances, may structurally enhance profitability and capital efficiency. This may support resilient net interest income and pretax margins.

- Strategic investments in scale and efficiency, such as AI enabled service tools, expanded digital capabilities and balance sheet optimization, are designed to keep cost to serve low and operating leverage high. This could sustain strong pretax margins and earnings growth even if market conditions soften.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for Charles Schwab is $88.0, which represents up to two standard deviations below the consensus price target of $112.79. This valuation is based on what can be assumed as the expectations of Charles Schwab's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $148.0, and the most bearish reporting a price target of just $88.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2028, revenues will be $29.9 billion, earnings will come to $10.9 billion, and it would be trading on a PE ratio of 17.4x, assuming you use a discount rate of 8.8%.

- Given the current share price of $101.41, the analyst price target of $88.0 is 15.2% lower. Despite analysts expecting the underlying business to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Charles Schwab?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.