Last Update 15 Apr 26

AVAV: SCAR Recompetition Will Shape Future Space And Defense Demand

Analysts have collectively trimmed AeroVironment price targets by tens of dollars to a range of roughly $235 to $350, reflecting contract uncertainty around the SCAR program and questions about BlueHalo integration. They still highlight long term demand for unmanned systems, space and defense programs in their updated models.

Analyst Commentary

Recent research updates on AeroVironment show a mix of optimism about long term growth drivers and caution around execution risks tied to specific contracts and acquisitions.

Bullish Takeaways

- Bullish analysts point to AeroVironment's exposure to drones, counter-drone systems and space as key growth areas within defense, with JPMorgan highlighting these segments as drivers in its initiation work.

- Several research notes emphasize that even after SCAR related changes, the company still carries a sizeable unfunded backlog of about US$3b, which includes roughly US$1.5b linked to SCAR, supporting multi year revenue visibility if contracts convert as planned.

- Some bullish analysts describe underlying demand trends as favorable, citing long term opportunities in U.S. and global defense priorities and the potential for BlueHalo to open additional markets despite near term integration questions.

- Where models have been revised, bullish analysts often maintain positive views on long term capital appreciation potential, arguing that recent volatility and contract resets are already reflected in lowered price targets and valuations.

Bearish Takeaways

- Bearish analysts flag the termination and recompete of the SCAR program as a key overhang, with concerns that this may remove US$1b to US$1.4b from reported backlog and reduce visibility on revenue and margins over the next few years.

- Several reports describe Q3 results as disappointing or messy, pointing to weaker performance in the services heavy Cyber & Mission Systems business and to timing issues in the space segment that weighed on execution against prior expectations.

- Some cautious analysts question the fit of lower growth, margin dilutive BlueHalo legacy assets within a historically product led company, raising the risk that integration could pressure profitability compared with previous assumptions.

- There is added concern that contract changes and guidance cuts have increased uncertainty around outer year estimates, with at least one bearish group highlighting that core backlog may not grow in the near term and that investors face higher execution risk while waiting for contract resolutions.

What's in the News

- The U.S. Space Force is reopening the US$1.4b Satellite Communications Augmentation Resource (SCAR) program for mobile ground stations as it shifts away from cost-plus contracts and looks to diversify suppliers, affecting AeroVironment's largest program of record (Space News via The Fly).

- The U.S. Army deployed AeroVironment's LOCUST laser counter-drone weapon system near El Paso International Airport, prompting the FAA to halt air traffic for more than seven hours because of safety concerns for commercial flights (Reuters).

- AeroVironment reported goodwill impairment of about US$151m for the third quarter ended January 31, 2026. The company also expects goodwill impairment of US$151m for the fiscal year ending April 30, 2026, alongside earnings guidance that points to revenue between US$1.85b and US$1.95b and a projected net loss of US$218m to US$201m for the same period.

- The company announced the LOCUST X3 high-energy laser system, a third generation counter drone platform with a scalable 20 to 35+ kilowatt laser, AI-enabled targeting software and design features intended to support deployment across ground and maritime platforms.

- AeroVironment and the U.S. government remain in active negotiations on a revised SCAR ground station contract after a stop work order in January 2026. The parties are working toward a firm fixed price agreement while AeroVironment invests in expanded manufacturing capacity in Albuquerque, New Mexico, to support space and directed energy programs.

Valuation Changes

- Fair Value: Unchanged at $311.47 per share, indicating no adjustment to the base valuation level used in the model.

- Discount Rate: Reduced slightly from 7.74% to 7.66%, a modest shift that marginally lowers the hurdle rate applied to future cash flows.

- Revenue Growth: Kept effectively flat at about 20.52%, suggesting no material change in the long run top line growth assumption.

- Net Profit Margin: Held steady at about 7.30%, indicating stable expectations for underlying profitability.

- Future P/E: Trimmed slightly from 113.54x to 113.27x, reflecting a small adjustment in the multiple applied to projected earnings.

Key Takeaways

- Expansion into advanced defense technologies and international markets is driving sustained revenue growth, backlog visibility, and long-term earnings stability.

- Modular, AI-powered platforms and recent acquisitions enable margin expansion, diversification, and operational leverage as defense demands accelerate.

- Heavy reliance on U.S. defense contracts, intensifying competition, margin pressures from acquisitions, underdeveloped international markets, and rapid tech shifts threaten future growth and profitability.

Catalysts

About AeroVironment- Designs, develops, produces, delivers, and supports a portfolio of robotic systems and related services for government agencies and businesses in the United States and internationally.

- AeroVironment's recent contract wins and rapid expansion into advanced areas like space-based laser communications and directed energy weapons position the company to capitalize on the persistent global shift toward defense modernization, addressing urgent demands among the U.S. and allied militaries-likely supporting sustained top-line revenue growth and backlog visibility over multiple years.

- The company's strategic focus on developing modular, interoperable, and software-defined platforms-including the newly launched AV Halo open software ecosystem-directly aligns with the accelerating adoption of AI-powered autonomy and network-centric warfare, enabling future premium pricing, increased service revenues, and gross margin expansion as these high-value platforms are deployed at scale.

- Successful integration of the BlueHalo acquisition materially expands AeroVironment's addressable markets, diversifies its competitive portfolio, and enables operational leverage as the company increases manufacturing capacity, which should support bottom-line EBITDA and net margin improvement as production volumes ramp.

- AeroVironment's growing list of large, multi-year government contracts (funded and unfunded backlog), as well as its positioning as a sole-source or leading provider in next-generation missile defense, Counter-UAS, and space comms, offers long-term revenue visibility and reduces downside risk associated with individual program delays-further enhancing future earnings stability.

- Driven by rising geopolitical tensions, cross-border threats, and persistent ISR needs, AeroVironment is successfully expanding internationally through key partnerships and certifications, which should drive both revenue growth and higher-margin international sales beyond its historical domestic concentration, positively impacting both top-line and profit growth trajectories.

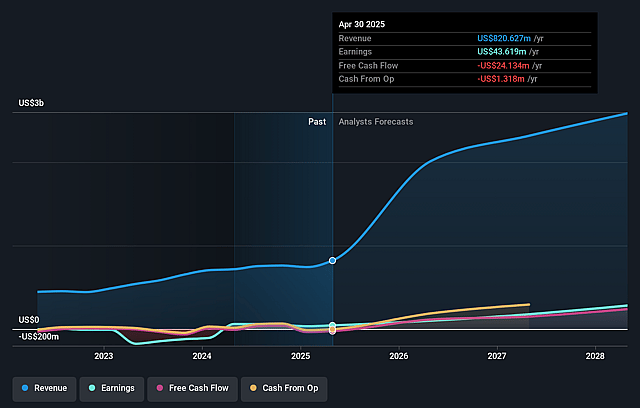

AeroVironment Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming AeroVironment's revenue will grow by 20.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from -13.9% today to 7.3% in 3 years time.

- Analysts expect earnings to reach $205.9 million (and earnings per share of $3.94) by about April 2029, up from -$224.4 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $479.8 million in earnings, and the most bearish expecting $119.7 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 115.0x on those 2029 earnings, up from -43.7x today. This future PE is greater than the current PE for the US Aerospace & Defense industry at 38.9x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.66%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- AeroVironment's substantial dependence on U.S. government and DoD contracts (with 78% of revenue domestic and only 22% international) makes it highly vulnerable to U.S. budget cycles, congressional delays, or shifting defense priorities, increasing the risk of revenue volatility if funding or priorities change.

- Long-term competitive risks are amplified by the increasing number of entrants and established players in the UAS and Counter-UAS markets, raising the likelihood of price competition, margin compression, and potentially lower long-term net earnings on flagship products like Switchblade.

- The company's gross margin profile has seen a significant decline post-BlueHalo acquisition (from 43% GAAP/45% adjusted to 21% GAAP/29% adjusted), driven by a higher services mix and costs associated with integration, which may persist or worsen, pressuring long-term net margins and profitability.

- While AeroVironment highlights international opportunities, underinvestment or limited traction in expanding international sales and after-sales support could restrain revenue diversification and long-term growth, leaving the business exposed to regional policy changes or geopolitical headwinds.

- Accelerating technological advances in AI, large-scale drone autonomy, and counter-UAS solutions pose a risk that AeroVironment's current platforms could be leapfrogged if R&D investment or innovation pace lags behind larger or more nimble competitors, threatening future contract wins and eroding revenue and margins over time.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $311.47 for AeroVironment based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $450.0, and the most bearish reporting a price target of just $235.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $2.8 billion, earnings will come to $205.9 million, and it would be trading on a PE ratio of 115.0x, assuming you use a discount rate of 7.7%.

- Given the current share price of $194.52, the analyst price target of $311.47 is 37.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on AeroVironment?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.