Last Update 03 Jun 26

Fair value Decreased 0.89%WTS: Record Q1 Results And Higher Payouts Will Shape Forward Risk Balance

Narrative Update: Watts Water Technologies Price Target Shift

The updated analyst price target for Watts Water Technologies edges down by about $3 to $333, as analysts balance slightly softer growth assumptions and a higher discount rate against a modestly higher profit margin outlook and a lower future P/E, in line with recent mixed target revisions from Barclays, RBC Capital, Deutsche Bank, and Stifel.

Analyst Commentary

Recent Street research on Watts Water Technologies shows a mix of raised and lowered price targets, with adjustments moving in both directions over the past several reports. This split view gives you a useful snapshot of how analysts are weighing execution, growth prospects, and valuation risk at current levels.

Bullish Takeaways

- Bullish analysts raising price targets highlight confidence in Watts Water Technologies' ability to execute on its current business plan, which they see as supportive of a higher long term valuation than previously assumed.

- The series of upward target revisions, including moves of $5, $12, and $22, point to a view that the stock's earnings power and cash generation potential may justify a richer P/E than earlier models suggested.

- Supportive research notes signal that bullish analysts see the company as relatively well positioned within its sector, which they link to resilience in revenue and margin assumptions in their models.

- Some bullish updates imply that prior targets may have been too conservative, with revised estimates reflecting a stronger fundamental profile than what had been priced into earlier forecasts.

Bearish Takeaways

- Bearish analysts lowering price targets, including cuts of $6 and $22, are signaling more caution on how much investors should be willing to pay for the stock given current information.

- These target reductions suggest concerns that prior expectations embedded in valuation models, such as growth or margin assumptions, may have been too optimistic relative to recent data.

- The downward revisions also point to increased focus on risk, with bearish analysts building in more conservative scenarios around execution and earnings visibility.

- Overall, the target cuts indicate that some on the Street see a less favorable risk and reward balance at recent prices, prompting tighter valuation multiples in their frameworks.

What's in the News

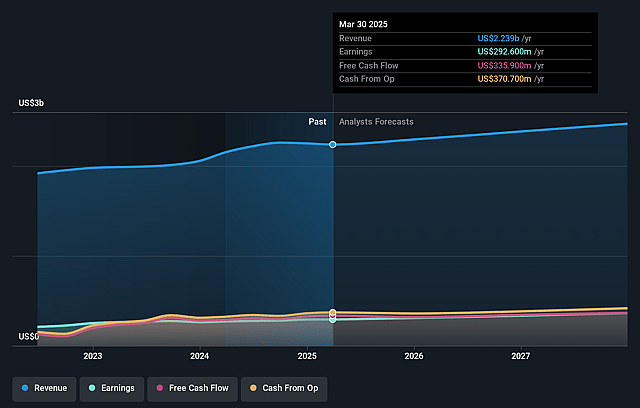

- Q1 2026 results: Watts Water Technologies reported record Q1 2026 revenue of $677.3 million, up 21.4% year over year, with organic sales up 12% and adjusted EPS of $3.04, both ahead of analyst estimates, and an operating margin of 19.6% versus 15.7% a year earlier. Source: Q1 2026 earnings reports.

- Dividend move: The company announced a 21% increase in its quarterly dividend to $0.63 per share, payable June 15, 2026, to holders of record on June 1, 2026. Source: dividend declaration and Q1 2026 earnings release.

- Guidance and capital allocation: Management reaffirmed full-year 2026 guidance for reported sales growth of 8% to 12% and operating margin of 18.8% to 19.4%, and highlighted continued investment in product development, digital solutions, and targeted acquisitions, supported by a balance sheet described as strong. Source: Q1 2026 earnings call and guidance update.

- Share repurchases: Between January 1 and March 29, 2026, Watts repurchased 12,652 shares for US$3.85 million, completing buybacks of 103,975 shares for US$24.93 million under the existing program announced August 2, 2023. Source: buyback tranche update.

- Governance and shareholder support: At the 2026 Annual Meeting, shareholders re-elected nine directors, approved executive compensation with 98.2% support on an advisory basis, and ratified KPMG LLP as auditor with 97.0% support, alongside Q1 results that exceeded analyst expectations. Source: 2026 Annual Meeting summary and Q1 2026 earnings reports.

Valuation Changes

- Fair Value: The updated fair value estimate edges down slightly from $336.11 to $333.11 per share, a reduction of about 0.9%.

- Discount Rate: The discount rate in the valuation model rises modestly from 8.34% to 8.51%.

- Revenue Growth: The revenue growth assumption is trimmed from 6.84% to 6.13%.

- Net Profit Margin: The net profit margin assumption ticks up from 16.10% to 16.25%.

- Future P/E: The future P/E multiple assumption moves down from 29.45x to 28.26x.

Key Takeaways

- Accelerating growth in intelligent water management and regulatory-driven demand is boosting recurring revenue, margins, and Watts' pricing power across key sectors and acquisitions.

- Strategic investments in automation, supply chain, and integration of acquisitions are increasing operational efficiency, supporting profitability and resilience against global cost pressures.

- European weakness, tariff risks, fading pricing benefits, slow digital growth, and declining segment volumes threaten revenue stability, margin expansion, and long-term growth expectations.

Catalysts

About Watts Water Technologies- Supplies systems, products and solutions that manage and conserve the flow of fluids and energy into, though, and out of buildings in the commercial, industrial, and residential markets in the Americas, Europe, the Asia-Pacific, the Middle East, and Africa.

- The accelerating rollout and success of Nexa, Watts' intelligent water management platform, positions the company to capture the growing demand for advanced, data-driven water conservation, efficiency, and regulatory compliance solutions-expected to drive higher-margin, recurring revenue and support long-term earnings and margin expansion.

- Ongoing global urbanization and the need for water infrastructure upgrades-especially in fast-growing segments like data centers and across verticals such as hospitality and multifamily-are expected to sustain revenue growth by increasing the addressable market and demand for Watts' portfolio, including through new acquisitions.

- Growing sustainability and regulatory requirements around water quality, conservation, and carbon reduction are increasing demand for Watts' differentiated solutions (e.g., energy-efficient, compliant, and safe products), likely supporting resilient end-market demand and enabling continued pricing power, supporting topline growth and profitability.

- Strategic investments in automation, supply chain resilience, and proactive tariff management have improved operational flexibility and cost efficiency, positioning Watts to defend and potentially expand net margins even in the face of ongoing global trade and input cost volatility.

- Integration of recent acquisitions (I-CON, EasyWater, Bradley, Josam) is delivering faster-than-expected revenue and cost synergies, providing a catalyst for further operating leverage and supporting both revenue and earnings per share growth in future periods.

Watts Water Technologies Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Watts Water Technologies's revenue will grow by 6.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 14.3% today to 16.3% in 3 years time.

- Analysts expect earnings to reach $496.9 million (and earnings per share of $14.83) by about June 2029, up from $366.4 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 28.7x on those 2029 earnings, up from 28.3x today. This future PE is greater than the current PE for the US Machinery industry at 27.5x.

- Analysts expect the number of shares outstanding to grow by 0.09% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.51%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Persistent weakness and uncertainty in the European market, with continued volume declines and soft construction activity, poses a risk to international revenue diversification and could result in longer-term revenue stagnation or even contraction.

- Significant exposure to tariff fluctuations, including unpredictable new tariffs on copper and products sourced globally, increases input cost volatility and could compress net margins if further price increases become unsustainable in the face of customer resistance or competitive pricing pressures.

- The positive impact of recent price/cost dynamics is largely nonrecurring (e.g., pull-forward demand and low-cost inventory), so gross and operating margins may decline toward historical levels, limiting sustained earnings growth and potentially disappointing future expectations.

- Growth in digital and smart water offerings (such as Nexa) is slow, with long sales cycles (1–2 years), small current revenue contribution, and uncertainty about the pace of adoption; this could result in underwhelming revenue and margin expansion from digital initiatives relative to long-term projections.

- Volumes in certain segments (notably residential and, at times, APMEA) are declining, and much of the recent outperformance in Americas was partly driven by pull-forward demand, which will reverse in subsequent quarters, risking future revenue and profit volatility if organic demand does not rebound.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $333.11 for Watts Water Technologies based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $379.0, and the most bearish reporting a price target of just $275.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $3.1 billion, earnings will come to $496.9 million, and it would be trading on a PE ratio of 28.7x, assuming you use a discount rate of 8.5%.

- Given the current share price of $310.27, the analyst price target of $333.11 is 6.9% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Watts Water Technologies?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.