Last Update 01 Apr 26

Fair value Decreased 3.99%IREN: Microsoft AI Contract Will Drive Transformative Data Center Expansion

The Street's blended 12 month price target for IREN has shifted modestly lower to about $76 from roughly $79, as analysts balance Macquarie's $25 cut with fresh Buy upgrades and a higher $80 target tied to IREN's large AI contract with Microsoft and a sizeable data center growth pipeline.

Analyst Commentary

Recent Street research on IREN shows a mix of optimism around growth optionality and caution around execution and valuation, which is feeding into the wide range of price targets and rating changes.

Bullish Takeaways

- Bullish analysts point to the large AI infrastructure contract with Microsoft as a key support for their higher price targets around $80, seeing it as an anchor customer that can help underpin long term revenue visibility.

- The expectation of over 2 GW of incremental capacity targeted to be fully energized by 2027 is viewed as a major growth lever, with bulls arguing that IREN offers some of the highest exposure to the AI infrastructure theme within their coverage.

- Double upgrades from Sell to Buy, along with price targets raised from $56 to $80, signal a reassessment of IREN's execution potential as the company scales its data center footprint tied to AI workloads.

- Supportive commentary around a "transformative year" reflects confidence that IREN's development pipeline and AI focus can justify premium growth expectations relative to more traditional Bitcoin mining peers.

Bearish Takeaways

- Bearish analysts cutting price targets by $25 highlight that, despite the AI narrative, there are still concerns around how quickly IREN can execute on its large build out and convert pipeline into cash flow.

- The shift in the blended 12 month target from roughly $79 to about $76 suggests that some on the Street are reassessing risk around timing, costs, and potential delays tied to the 2 GW expansion plan.

- Cautious views also reflect questions about concentration risk around a single large AI customer relationship, with bears watching how dependency on Microsoft evolves over time.

- The wide spread between the more conservative and the high end $80 targets underlines uncertainty around IREN's ability to deliver on both its AI ambitions and traditional mining operations without execution slip ups.

What's in the News

- IREN entered purchase agreements for over 50,000 NVIDIA B300 GPUs, with plans to expand its total fleet to 150,000 GPUs deployed in phases through the second half of 2026 across existing air cooled data centers in Mackenzie, British Columbia and Childress, Texas (Key Developments).

- The planned 150,000 GPU fleet is expected to support AI Cloud annualized run rate revenue of over US$3.7b by the end of 2026, tied to deployments across the company’s existing sites including Canal Flats and Childress, which provide capacity for more GPUs over time (Key Developments).

- IREN has secured US$9.3b of funding in the past eight months across customer prepayments, convertible notes, GPU leasing and GPU financing, and plans to use these and other capital sources to finance roughly US$3.5b of additional capex for the GPU and data center build out expected in the second half of 2026 (Key Developments).

- Payment terms on the GPU orders are structured on a post shipment basis, which the company indicates is intended to support working capital efficiency as hardware procurement is sequenced with commercial milestones and capital availability (Key Developments).

- IREN established an at the market equity program as part of its broader capital management framework, with the program intended to sit alongside existing and new funding sources as the company scales (Key Developments).

Valuation Changes

- Fair Value: The blended Fair Value estimate has eased from about $79.31 to roughly $76.14, representing a modest step down in the modeled upside for IREN.

- Discount Rate: The Discount Rate has risen slightly from 8.88% to about 8.99%, reflecting a marginally higher required return in the updated assumptions.

- Revenue Growth: Revenue Growth expectations have shifted from roughly 58.78% to about 85.70%, indicating a much higher modeled growth rate in the latest update.

- Net Profit Margin: Net Profit Margin assumptions have moved from about 0.04% to around 1.62%, pointing to a higher projected level of profitability on future dollar revenue.

- Future P/E: The Future P/E multiple has moved from a very large level, above 30,000x, to about 512x, which is still very elevated but far lower than in the prior model run.

Key Takeaways

- Vertical integration and strategic partnerships strengthen IREN's growth in AI cloud and data center markets, supporting higher margins and future competitiveness.

- Flexible business model and efficient financing provide resilience, enabling shifts to higher-margin sectors and sustaining earnings amid industry changes.

- Heavy reliance on debt-funded expansion, volatile revenues, rising energy costs, competitive pressures, and regulatory risks threaten profitability, cash flow stability, and long-term growth.

Catalysts

About IREN- Operates in the integrated data center business.

- Rapid expansion into AI cloud services, fueled by IREN's vertical integration and direct-to-chip liquid cooling data centers, positions the company to capitalize on accelerating demand for AI infrastructure; this is expected to significantly boost long-term revenue growth and improve EBITDA margins due to recurring, high-margin AI cloud contracts.

- Secured expansion of grid-connected power and proprietary data centers (now at nearly 3GW and 810MW of operational capacity), enables IREN to serve both the digital currencies mining and AI compute sectors, offering flexibility to pivot toward higher-margin segments as market opportunities evolve; this bodes well for future revenue visibility and capital efficiency.

- Strengthened cost position through low all-in cash mining costs ($36,000/Bitcoin) and access to low-cost, renewable power ($0.035/kWh), puts IREN at an advantage in a consolidating industry, supporting robust net margins and sustainable earnings even as weaker miners exit post-halving.

- Strong institutional partnerships and designation as an NVIDIA preferred partner unlock access to next-generation GPU supply and broaden IREN's customer pipeline, positioning the company to benefit from greater institutional adoption of digital assets and advanced computing-supporting both topline growth and long-term competitiveness.

- Successful and capital-efficient financing strategies (e.g., 100% non-dilutive GPU financings at low rates, robust cash reserves), enable IREN to scale AI and data center business lines without undue leverage, securing the required capital for expansion and reducing future risk to net margins and cash flow.

IREN Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

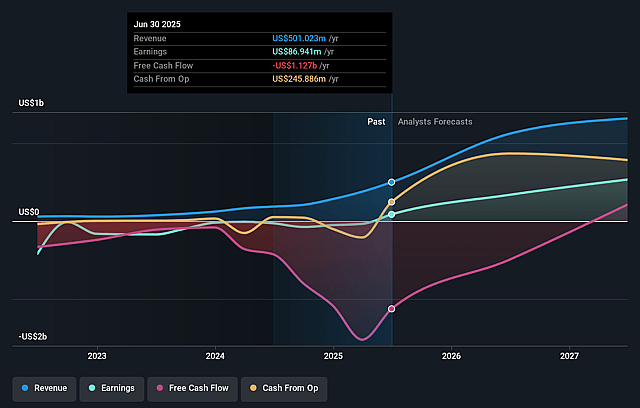

- Analysts are assuming IREN's revenue will grow by 85.7% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 51.5% today to 1.6% in 3 years time.

- Analysts expect earnings to reach $78.3 million (and earnings per share of -$0.89) by about April 2029, down from $389.7 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting $138.3 million in earnings, and the most bearish expecting $-2.1 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 512.3x on those 2029 earnings, up from 29.2x today. This future PE is greater than the current PE for the US Software industry at 29.4x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.99%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- IREN's heavy capital expenditures for rapid data center and GPU expansion, funded by significant debt and lease financing, risk outpacing operating cash flows-potentially leading to higher leverage, reduced free cash flow, and downward pressure on net margins if market conditions become less favorable.

- The company's revenues remain highly reliant on Bitcoin mining and, increasingly, short-term AI cloud contracts; continued earnings stability may be threatened by Bitcoin price volatility, future block reward halvings, and the relatively short contract duration for AI compute services, impacting revenue predictability and long-term cash flow.

- Rising global energy prices and potential scarcity or cost volatility in key energy markets (e.g., West Texas and British Columbia) could drive higher operating expenses and erode IREN's low-cost advantage, negatively affecting gross and net margins over time.

- The introduction of new, more efficient GPUs and ASICs from competitors, coupled with increasing customer demand for more flexible or lower-density rack configurations, could materially shorten equipment life cycles and raise the ongoing capital intensity of IREN's infrastructure, pressuring profit margins and necessitating continual high investment.

- The rapid scaling and geographic concentration of data center assets increase exposure to regulatory, environmental, and permitting risks (including ESG pressures on energy use and emissions), which may result in added compliance costs or restrictions-ultimately reducing profitability and increasing execution risk on planned expansions.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $76.14 for IREN based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $125.0, and the most bearish reporting a price target of just $26.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $4.8 billion, earnings will come to $78.3 million, and it would be trading on a PE ratio of 512.3x, assuming you use a discount rate of 9.0%.

- Given the current share price of $34.28, the analyst price target of $76.14 is 55.0% higher. Despite analysts expecting the underlying business to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on IREN?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives