Last Update 30 Apr 26

Fair value Decreased 22%UPST: Bank Charter Pursuit And GenAI Underwriting Are Expected To Drive Upside

Analysts have trimmed their average price target for Upstart Holdings, with fair value estimates moving from about $56.64 to $43.93 as several firms cut targets by $4 to $15 while highlighting mixed views on funding risk, earnings potential, and the impact of the company's bank charter ambitions.

Analyst Commentary

Recent research on Upstart shows a split between analysts who see improving risk and earnings potential and those who remain cautious on funding, macro sensitivity, and valuation. Price target changes have clustered around US$30 to US$49, with several firms adjusting ratings alongside target revisions.

Bullish Takeaways

- Bullish analysts see the bank charter application as a potential way to reduce reliance on external funding, which they view as a key overhang on the business and its valuation.

- Some expect that, if the bank charter is successful, it could address what they see as downside risk tied to private credit exposure, which they link directly to earnings durability and capital access.

- One bullish research note highlighted what it called 60% earnings upside, arguing that the current share price does not reflect any benefit from a possible bank charter approval or reduced funding risk.

- Upgrades from Sell to Neutral and from Neutral to Buy signal that a group of analysts see the risk or valuation gap as more balanced than before, especially relative to the company’s long term ambitions.

Bearish Takeaways

- Bearish analysts have trimmed price targets by US$4 to US$15, pointing to a more uncertain macro backdrop and lower market multiples that, in their view, justify a lower fair value for consumer finance names, including Upstart.

- Some research flags concern that funding sources could still be pressured, which they see as a core execution risk and a reason to stay cautious on how quickly the business can scale at an attractive return.

- There is skepticism around the company’s outlook through fiscal 2028, described by one firm as ambitious, with the implication that execution would need to be strong for the current valuation to look attractive.

- Downgrades and target cuts from larger firms such as JPMorgan, as well as from other cautious analysts, indicate concern that macro sensitivity and funding dependence could restrict earnings progress relative to prior expectations.

What's in the News

- Pomerantz LLP filed a class action lawsuit in the Southern District of New York alleging materially false and misleading statements around Upstart's Model 22 AI underwriting performance and 2025 revenue guidance, with the case seeking damages under Sections 10(b) and 20(a) of the Exchange Act (Key Developments).

- Upstart plans to apply to the OCC and FDIC to establish Upstart Bank, N.A., and to the Federal Reserve to become a bank holding company, with the goal of placing lending activities under a federal prudential framework and accessing deposit funding directly (Key Developments).

- Co founder and CTO Paul Gu is set to become CEO on May 1, 2026. Co founder Dave Girouard will remain Executive Chairman and special advisor, and Andrea Blankmeyer is joining as CFO. Former CFO Sanjay Datta is moving into the role of President and Chief Capital Officer (Key Developments).

- Upstart issued 2026 guidance for total revenue of approximately US$1.4b and provided a 2025 to 2028 outlook that targets a compound annual growth rate of about 35% for total revenue (Key Developments).

- DuPage Credit Union and Harborstone Credit Union each partnered with Upstart to use its AI powered platform and referral network for personal loans, expanding Upstart's reach among credit union members in Illinois and other regions (Key Developments).

Valuation Changes

- Fair Value: Trimmed from $56.64 to $43.93, a reduction of about 22% in the updated model output.

- Discount Rate: Risen slightly from 8.94% to 9.03%, implying a modestly higher required return in the updated assumptions.

- Revenue Growth: Increased from 19.74% to 29.91%, indicating a higher modeled top line growth rate in the new inputs.

- Net Profit Margin: Adjusted from 16.90% to 16.53%, a small reduction in expected profitability on each $ of revenue.

- Future P/E: Lowered from 27.33x to 15.63x, resulting in a meaningfully lower valuation multiple in the revised framework.

Key Takeaways

- Improvements in underwriting, automation, and personalization enhance loan approval rates, lower costs, and reduce default risks, positively impacting revenue and net margins.

- Strategic HELOC growth, backed by strong banking relationships, alongside expanded borrower base, sets stage for future revenue growth and earnings support.

- High default rates and macroeconomic volatility threaten revenue stability, while maintaining model accuracy and managing profitability amid these conditions are critical challenges.

Catalysts

About Upstart Holdings- Operates a cloud-based artificial intelligence (AI) lending platform in the United States.

- The implementation of Model 19, featuring the Payment Transition Model (PTM), has improved underwriting accuracy, which is likely to enhance loan approval rates and reduce default risks, positively impacting revenue and net margins.

- Upstart's HELOC product growth, driven by conversion improvements, cross-selling, and state expansion, positions it well for future revenue growth and margins with the potential to leverage its strong relationships with banks and credit unions for cost-effective funding.

- Improvements in small dollar relief loans, such as reduced origination costs, have expanded Upstart's borrower base and are expected to contribute to revenue growth, while the integration of small dollar repayment data will enhance the accuracy of underwriting models.

- Increased automation and personalization in servicing operations have reduced costs and improved borrower outcomes, which will likely improve net margins through operational efficiencies and lower default rates.

- Enhanced lending partner confidence, due to strong platform performance and capital market engagements, strengthens funding capabilities and sets the stage for increased origination volume, supporting earnings growth in the medium term.

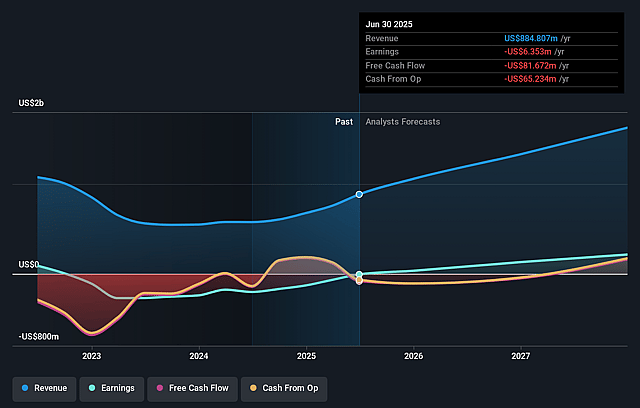

Upstart Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Upstart Holdings's revenue will grow by 29.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from 5.0% today to 16.5% in 3 years time.

- Analysts expect earnings to reach $389.8 million (and earnings per share of $3.13) by about April 2029, up from $53.6 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $558.3 million.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 15.7x on those 2029 earnings, down from 54.4x today. This future PE is greater than the current PE for the US Consumer Finance industry at 9.7x.

- Analysts expect the number of shares outstanding to grow by 3.07% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.03%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company has faced periods of underperformance due to high default rates during macroeconomic volatility, potentially impacting future revenue and profit stability.

- There are concerns about maintaining consistent model accuracy, which is crucial for managing risk and ensuring profitability, due to potential gaps between predicted and actual default rates.

- The company's profitability is sensitive to macroeconomic changes, such as interest rate movements and macro indices (e.g., the Upstart Macro Index), which could affect earnings and net margins if conditions worsen.

- Although the company plans to reduce loans on its balance sheet, potential funding constraints could delay these efforts, affecting liquidity and net income.

- Investments in new product categories and marketing could pressure operating margins and net income if not managed properly against growth expectations.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $43.93 for Upstart Holdings based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $80.0, and the most bearish reporting a price target of just $20.0.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be $2.4 billion, earnings will come to $389.8 million, and it would be trading on a PE ratio of 15.7x, assuming you use a discount rate of 9.0%.

- Given the current share price of $30.48, the analyst price target of $43.93 is 30.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Upstart Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.