Last Update 21 Jan 26

Fair value Increased 2.22%IPGP: Business Recovery In Welding And Micromachining Will Support Higher Future Multiple

Analysts have nudged their price expectations for IPG Photonics higher, with our fair value estimate moving from about $94 to roughly $96, citing recent target increases and upgrades that highlight improving demand trends and a slightly richer assumed future P/E multiple.

Analyst Commentary

Bullish Takeaways

- Bullish analysts point to the recent upgrade and higher price target of US$105, up from US$68, as support for a higher assumed P/E. They view this as reflecting improved confidence in execution.

- The shift from a Sell to a Buy stance following the Q3 report is framed as evidence that recent revenue performance, after 12 consecutive quarters of year over year declines, may help reset expectations for future growth.

- Improving demand for welding and micromachining is seen as a key factor that could support a more constructive view on the company’s core franchises and justify a richer valuation multiple.

- Positive year over year revenue growth in Q3, following a long period of declines, is being used by bullish analysts as a sign that business recovery efforts are gaining traction.

Bearish Takeaways

- Bearish analysts may focus on the fact that the company experienced 12 consecutive quarters of year over year revenue declines, which can limit how much confidence investors place in a single quarter of improved results.

- The higher fair value estimate and increased external price targets rely on an assumption of better demand trends. These could be at risk if welding and micromachining orders soften from current levels.

- The richer assumed future P/E multiple leaves less room for error on execution, so any slip in revenue momentum or margins could have an outsized effect on valuation.

- Some investors may see the rapid shift from a Sell to a Buy stance as a sign that sentiment can turn quickly again if the recovery pace does not match current expectations.

What's in the News

- IPG Photonics plans to showcase a wide range of new laser solutions at the 2026 SPIE Photonics West Exhibition in San Francisco, including high power cleaning, welding, cutting, micro machining and directed energy products, along with thought leader presentations on laser technologies and industry topics (Key Developments).

- The company is highlighting new nanosecond laser products for cleaning applications, such as a 3 kilowatt high power laser source in an ultra compact form factor and a 650 watt air cooled high pulse energy laser module, aimed at non contact, chemical free surface preparation (Key Developments).

- For precision micro machining, IPG Photonics plans to show a 10 W pulsed Deep UV laser module at a 266 nanometer wavelength and a Femto COMB laser at mid IR wavelengths, positioned for applications like semiconductor manufacturing and advanced spectroscopy and metrology (Key Developments).

- In high power and directed energy, the company will display rack integrated single mode lasers up to 60 kilowatts, along with an 8 kilowatt ultra compact rack system and a 4 kilowatt narrow band amplifier, targeting mission critical defense applications and industrial materials processing (Key Developments).

- IPG Photonics announced the grand opening of a new 14,000 square foot office and manufacturing facility in Huntsville, Alabama, which will serve as the headquarters for the new IPG Defense business focused on laser defense solutions for military and civilian use, with on site customer experience and collaborative workspaces (Key Developments).

Valuation Changes

- The fair value estimate has edged up from about US$94.00 to roughly US$96.08.

- The discount rate is slightly higher, moving from about 8.39% to around 8.41%.

- The revenue growth assumption is essentially unchanged, at about 9.82% both before and after the update.

- The net profit margin assumption is marginally higher, moving from roughly 9.97% to about 9.97% on the updated figures.

- The future P/E multiple has risen slightly, from about 37.65x to roughly 38.50x.

Key Takeaways

- Expanding applications in automation, electric vehicles, and new verticals like medical and defense are driving diversified growth and increasing IPG's long-term revenue potential.

- Operational efficiencies, flexible manufacturing, and innovative product launches are expected to further support margin expansion and stronger profitability.

- Rising geopolitical and competitive pressures, combined with core business softness and high investment risk in emerging segments, threaten IPG's revenue stability, margins, and earnings growth.

Catalysts

About IPG Photonics- Develops, manufactures, and sells various high-performance fiber lasers, fiber amplifiers, and diode lasers used in materials processing, medical, and advanced applications worldwide.

- Demand for advanced lasers is expected to rise as manufacturers globally accelerate automation and reshore production, leading to increased local investment in IPG's offerings and creating a runway for future revenue growth.

- The rapid transition to electric vehicles and battery production, especially in China and other major markets, is already driving increased adoption of welding, cutting, and micromachining lasers-expanding IPG's addressable market and positioning the company for continued top-line growth.

- New growth initiatives in medical (e.g., thulium lasers for urology), semiconductor, and micromachining end-markets are gaining early traction, diversifying revenue streams and supporting higher margins over time as these higher-value verticals scale.

- Recent product innovations like the CROSSBOW directed energy system-validated with multiple unit deliveries and key partnerships (e.g., Lockheed Martin)-open up opportunities in defense and critical infrastructure, supporting both revenue acceleration and improved operating leverage.

- The company's flexibility to shift manufacturing across regions to mitigate tariffs, combined with operational improvements and cost reduction actions, should drive margin expansion and eventually boost both net income and free cash flow as revenues ramp.

IPG Photonics Future Earnings and Revenue Growth

Assumptions

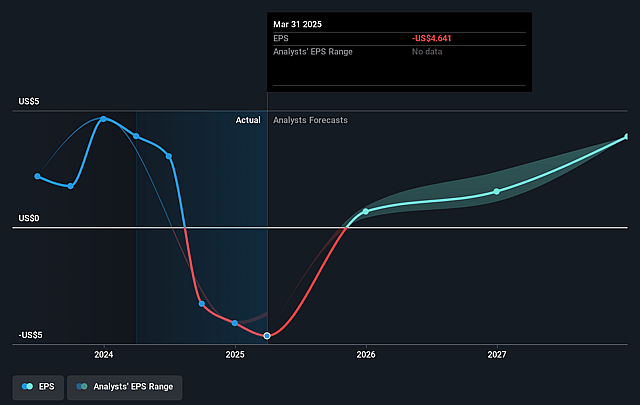

How have these above catalysts been quantified?- Analysts are assuming IPG Photonics's revenue will grow by 8.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from -22.8% today to 11.2% in 3 years time.

- Analysts expect earnings to reach $133.9 million (and earnings per share of $3.15) by about September 2028, up from $-215.4 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 29.6x on those 2028 earnings, up from -16.1x today. This future PE is greater than the current PE for the US Electronic industry at 23.9x.

- Analysts expect the number of shares outstanding to decline by 2.38% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.16%, as per the Simply Wall St company report.

IPG Photonics Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Ongoing tariff pressures and geopolitical uncertainties-especially new tariffs and long customs processing in key markets-create a volatile demand environment that management themselves characterize as having only cautious optimism, potentially leading to unpredictable revenues and reduced gross margins.

- Materials processing revenue, which has historically been IPG's core business, declined 6% year-over-year (factoring out divestitures), with management noting softness in cutting, welding, and additive manufacturing in several regions-exposing the company to the risk of long-term revenue stagnation if core markets do not recover robustly.

- Elevated operating expenses driven by heavy R&D spend, high CapEx ($100 million forecast for 2025), strategic M&A, and expansion of the organization could suppress free cash flow and net margins if new initiatives do not achieve strong growth or encounter slower-than-anticipated market adoption.

- While innovative advanced applications (e.g., medical, micromachining, defense) are showing growth, these markets are described as nascent and hard to size; over-reliance on new, unproven segments brings execution risk and may not offset margin erosion or declines in legacy businesses, impacting long-term earnings stability.

- Competitive forces-from low-cost Asian manufacturers, potential commoditization of fiber lasers, and alternative technological advances-threaten IPG's pricing power and market share in both legacy and emerging applications, with possible downward pressure on long-term gross margins and the sustainability of earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $80.2 for IPG Photonics based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $97.0, and the most bearish reporting a price target of just $65.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $1.2 billion, earnings will come to $133.9 million, and it would be trading on a PE ratio of 29.6x, assuming you use a discount rate of 8.2%.

- Given the current share price of $81.93, the analyst price target of $80.2 is 2.2% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on IPG Photonics?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.