Last Update 22 Nov 25

Fair value Increased 2.19%NTCT: Future Performance Will Depend On AI Market Execution

NetScout Systems' analyst price target has increased from $33.00 to $35.00. This reflects analysts' confidence in the company's positioning within key growth markets and its improving profit margin outlook.

Analyst Commentary

Recent analyst activity reflects a growing optimism about NetScout Systems' prospects, while also highlighting certain factors for investors to consider. The following points summarize both the optimistic and cautious views surrounding the stock's outlook and valuation.

Bullish Takeaways

- Bullish analysts have increased their price targets, citing confidence in NetScout's ability to execute following solid quarterly performance.

- NetScout's positioning within key growth markets, including the emerging applications of artificial intelligence, is seen as a significant long-term driver for revenue and margin expansion.

- Recent coverage reinitiation and Buy ratings suggest that the company's strategic markets and product offerings are attracting renewed investor interest.

- The recent pullback in NetScout's share price is viewed as a potential buying opportunity for investors, especially as the company addresses multiple attractive growth sectors.

Bearish Takeaways

- Bearish analysts note that, despite positive outlooks, consistent execution in penetrating new growth markets remains essential for valuation justification.

- The company must continue to demonstrate improvement in profitability and market share to sustain the current momentum in its stock price.

- Uncertainties around the pace of adoption of artificial intelligence-driven solutions could present risks to medium-term revenue growth expectations.

What's in the News

- NetScout Systems updated its earnings guidance for the third quarter of 2025, projecting revenue between $230 million and $240 million. (Key Developments)

- The company has completed the repurchase of 3,478,951 shares since May 2022, totaling $73.48 million or 4.84% of outstanding shares. (Key Developments)

- NetScout raised its fiscal year 2026 guidance, now expecting revenue between $830 million and $870 million and GAAP diluted net income per share between $1.13 and $1.23. (Key Developments)

- The company introduced Omnis KlearSight Sensor for Kubernetes, which provides deep observability and actionable insights for complex cloud environments, particularly in multi-cluster Kubernetes deployments. (Key Developments)

- NetScout published research on the evolving DDoS attack landscape, noting over 8 million attacks globally in the first half of 2025 with increased precision, scale, and involvement of hacktivist groups. (Key Developments)

Valuation Changes

- Fair Value has increased slightly from $30.42 to $31.09, reflecting a modest revision in forecasted intrinsic worth.

- Discount Rate has decreased minimally from 8.10% to 8.03%, indicating a slightly lower perceived risk profile.

- Revenue Growth projection has fallen from 2.58% to 1.94%, showing a tempered outlook for top-line expansion.

- Net Profit Margin estimate has risen slightly from 9.83% to 10.01%, suggesting expectations for improved profitability.

- Future P/E ratio has increased marginally from 30.66x to 31.27x, indicating a subtle upward adjustment in the company's expected earnings multiple.

Key Takeaways

- Investor optimism hinges on NetScout's AI-driven cybersecurity growth and momentum in enterprise and federal segments, fueling high expectations for sustained revenue and margin expansion.

- Risks from cloud migration and IT stack consolidation may be underestimated, potentially threatening long-term stability of legacy products and current margin expectations.

- Strong cybersecurity growth, expanding AI-driven solutions, customer diversification, robust financial health, and favorable industry trends position NetScout for sustained revenue and profit gains.

Catalysts

About NetScout Systems- Provides service assurance and cybersecurity solutions to protect digital business services against disruptions in the United States, Europe, Asia, and internationally.

- Market optimism appears to be driven by strong recent growth in NetScout's cybersecurity segment, underpinned by customers prioritizing spending to counter increasingly complex and expanding cyber threats, which could lead investors to expect above-trend long-term revenue and earnings growth.

- There is a narrative that NetScout's integration of AI-driven capabilities (like Omnis AI Insights and AI-backed enhancements in DDoS defense) positions the company as a differentiated leader in an expanding observability and cybersecurity market, potentially prompting unrealistic expectations for sustained margin expansion and premium revenue multiples.

- Investors seem to be extrapolating robust enterprise and federal segment momentum (with double-digit growth and early large deal wins) as a sign the business can offset declining service provider verticals indefinitely, driving presumptions of consistent top-line stability and EPS growth.

- Expectations may be embedded that NetScout will fully capitalize on proliferation of 5G, AIOps, and ongoing digital transformations-assuming the company can maintain technological leadership and capture a disproportionate share of incremental network monitoring and security spend, causing upward pressure on valuation multiples.

- The market could be underappreciating the risk from continued migration to cloud-native architectures and consolidation of IT/security stacks, overestimating NetScout's ability to mitigate potential long-term pressure on legacy products, thus supporting inflated forecasts for revenue quality and sustainable net margins.

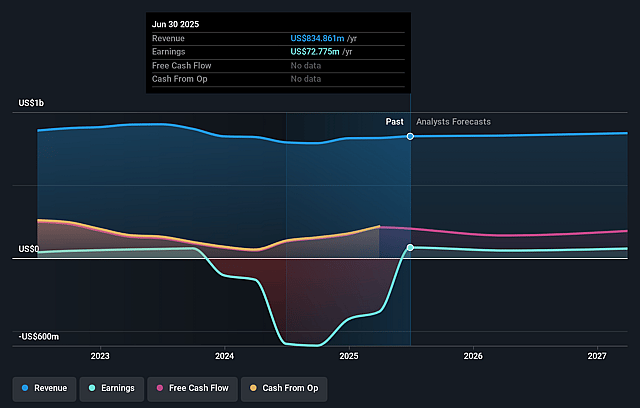

NetScout Systems Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming NetScout Systems's revenue will grow by 2.8% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 8.7% today to 5.5% in 3 years time.

- Analysts expect earnings to reach $49.6 million (and earnings per share of $0.72) by about September 2028, down from $72.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 47.1x on those 2028 earnings, up from 24.4x today. This future PE is greater than the current PE for the US Communications industry at 25.6x.

- Analysts expect the number of shares outstanding to grow by 0.22% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.89%, as per the Simply Wall St company report.

NetScout Systems Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- NetScout is experiencing strong growth in its cybersecurity product line (18% year-over-year revenue growth), ongoing enterprise demand for service assurance, and traction with large deals-including a high 7-figure government order and competitive displacement wins-which indicates its solutions are highly valued by customers navigating growing cybersecurity complexity, supporting the potential for sustained revenue and earnings growth.

- AI-driven innovation is expanding NetScout's addressable market, as highlighted by their Omnis AI Insights and AI-powered DDoS protections; these enhance product differentiation and create upsell opportunities as enterprise customers invest in digital transformation and network observability, which could drive higher average contract values and increase long-term margins.

- The company is successfully diversifying its customer base, with no single customer accounting for more than 10% of revenue, and a healthy split between U.S. (54%) and international markets (46%), which reduces revenue volatility risk and supports a more predictable top-line trajectory.

- NetScout is generating robust free cash flow ($71.7 million in Q1), has a strong liquidity position (over $540 million in cash and investments, no debt), and is actively repurchasing shares, all of which can support further investment in R&D, accretive acquisitions, or additional share buybacks-positively impacting earnings per share and shareholder value.

- The company continues to capture value from long-term secular trends such as rising global network complexity, growth in 5G and cloud adoption, and heightened regulatory and cybersecurity requirements, positioning it to benefit from increasing demand for sophisticated network monitoring and security solutions-translating to potential sustained revenue and profit growth in the future.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of $25.817 for NetScout Systems based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $33.0, and the most bearish reporting a price target of just $21.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $905.7 million, earnings will come to $49.6 million, and it would be trading on a PE ratio of 47.1x, assuming you use a discount rate of 7.9%.

- Given the current share price of $24.73, the analyst price target of $25.82 is 4.2% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.