Last Update 19 May 26

Fair value Increased 43%NTCT: Higher Earnings Efficiency And AI Expansion Will Drive Bullish Repricing

Analysts have lifted their fair value estimate for NetScout Systems from $35.00 to $50.00, citing updated assumptions for revenue growth, profit margins, and future P/E that align with recent Street research price target revisions.

Analyst Commentary

Bullish analysts are pointing to the higher fair value estimate as a sign that updated assumptions on revenue, margins, and future P/E are more in line with current Street thinking on NetScout Systems.

Recent research, including a price target adjustment that lifted the target by US$9, supports the view that prior expectations may have been too conservative relative to how other analysts are framing the stock.

Bullish Takeaways

- The US$9 price target increase is being used by bullish analysts as a reference point to justify a higher fair value range. This suggests that recent work on the model supports a stronger long term earnings profile than previously reflected.

- These analysts are emphasizing execution on revenue and profit margin assumptions as key reasons to lean into higher valuation multiples. They argue that the updated P/E input better reflects current Street thinking.

- Bullish commentary highlights that fair value and target moves are now more consistent with recent research, which reduces the gap between prior internal assumptions and the valuations applied across the Street.

- Overall, the tone from bullish analysts frames NetScout Systems as a stock where refreshed estimates and a higher target level are tied closely to clearer expectations around growth, profitability, and the multiple investors are prepared to pay.

What's in the News

- Updated buyback activity shows NetScout Systems repurchased 1,000,000 shares between January 1, 2026 and March 31, 2026 for US$29.23 million, bringing total repurchases under the May 5, 2022 program to 4,478,951 shares for US$102.71 million, representing 6.23% of shares (company filing)

- The company issued Fiscal Year 2027 guidance, with revenue expected in a range of US$885.0 million to US$915.0 million, GAAP diluted EPS projected between US$1.55 and US$1.70, and GAAP net income expected between approximately US$115 million and approximately US$126 million (company guidance)

- NetScout Systems announced an extension of its Omnis AI Insights solution to communications service providers, aiming to make raw network data AI ready for use in customer experience, predictive maintenance, and network security use cases (company announcement)

- The Omnis AI Sensor and AI Streamer products are positioned to help service providers curate high fidelity, real time network data into smaller, more actionable data streams for external AI agents and analytics platforms (company announcement)

Valuation Changes

- Fair Value: Updated estimate has risen from $35.00 to $50.00, representing a sizeable reset in the modeled value per share.

- Discount Rate: The assumed discount rate has increased slightly from 8.17% to 8.56%, implying a marginally higher required return in the model.

- Revenue Growth: The long term revenue growth assumption has moved from 3.41% to 4.51%, indicating a higher expected top line trajectory in the forecast.

- Net Profit Margin: The modeled profit margin has shifted from 9.71% to 12.56%, reflecting an assumption of stronger earnings efficiency on each dollar of revenue.

- Future P/E: The future P/E input has edged up from 35.44x to 36.34x, suggesting a slightly higher valuation multiple applied to projected earnings.

Key Takeaways

- Accelerated demand for AI-driven cybersecurity and observability tools positions the company for sustained growth and potential market leadership as digital transformation intensifies.

- Increasing high-value contracts, strong financial health, and strategic capital deployment point to greater revenue predictability and enhanced long-term profitability.

- Shifting industry trends, technological challenges, and overdependence on volatile contracts threaten NetScout's growth prospects, profitability, and ability to compete in a rapidly evolving market.

Catalysts

About NetScout Systems- Provides service assurance and cybersecurity solutions to protect digital business services against disruptions in the United States, Europe, Asia, and internationally.

- While analyst consensus points to growth in cybersecurity and service assurance driven by new AI and edge offerings, this likely understates NETSCOUT's positioning as customers rapidly expand digital transformation and AI initiatives, which could lead to sustained double-digit revenue growth in both service assurance and cybersecurity for multiple years as NETSCOUT's integrated solutions become core infrastructure.

- Analysts broadly agree that AI innovation in cybersecurity will drive product differentiation and margin expansion, but the scale of AI adoption and cyber threat evolution suggests NETSCOUT's AI-driven platform could vault it to category leadership, enabling premium pricing, taking share from competitors, and significantly lifting both gross and operating margins above historical norms.

- The expansion of cloud, 5G, and IoT with ever-increasing network complexity is likely to accelerate demand for NETSCOUT's observability and assurance tools at a faster-than-expected pace, potentially doubling its total addressable market over the next decade and boosting long-term top-line growth.

- NETSCOUT's strong traction across enterprise and federal government verticals-including multi-solution wins and earlier-than-expected large deals-signals that recurring, high-value contracts are becoming more frequent, which could drive a shift toward higher-quality, increasingly predictable subscription-based revenues and higher operating leverage.

- With a pristine balance sheet, robust free cash flow, and active share repurchases alongside no debt, the company is positioned for outsized earnings per share growth through a combination of strategic capital deployment and the ability to seize M&A opportunities that can further accelerate top-line and bottom-line expansion.

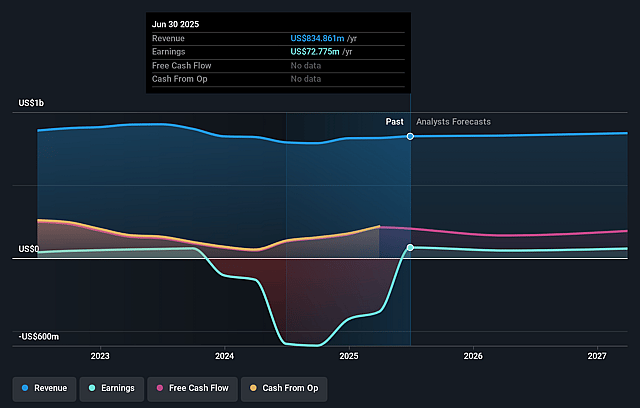

NetScout Systems Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more optimistic perspective on NetScout Systems compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming NetScout Systems's revenue will grow by 4.5% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 11.1% today to 12.6% in 3 years time.

- The bullish analysts expect earnings to reach $123.2 million (and earnings per share of $1.64) by about May 2029, up from $95.5 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 36.5x on those 2029 earnings, up from 29.1x today. This future PE is greater than the current PE for the US Communications industry at 30.8x.

- The bullish analysts expect the number of shares outstanding to decline by 0.53% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.56%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- NetScout faces long-term headwinds as more enterprises shift to cloud-native architectures and build in-house observability, which could shrink demand for traditional network monitoring tools, leading to pressure on future revenues and limiting addressable market growth.

- The proliferation of encrypted network traffic is making deep packet inspection less effective, undermining a foundational technology for NetScout's products and threatening to erode the competitive edge of its legacy offerings, with negative implications for product revenue and gross margins.

- While cybersecurity is driving current growth, heavy reliance on large, lumpy government and service provider contracts introduces risk of revenue volatility if these customers scale back or shift spending to diversified competitors or internal solutions in the future.

- NetScout's service provider business is showing signs of stagnation, with first quarter service provider revenue declining over five percent, and carrier investment in technology moving at a "measured pace"-this trend could translate to prolonged periods of flat or shrinking earnings as telecom partners increasingly adopt their own tools or delay infrastructure upgrades.

- The company's product portfolio has historically been slow to transition to recurring subscription or as-a-service models; as industry valuation multiples reward recurring revenue streams, this lag could drag on net margins and depress future earnings multiples in a changing investor climate.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for NetScout Systems is $50.0, which represents up to two standard deviations above the consensus price target of $41.71. This valuation is based on what can be assumed as the expectations of NetScout Systems's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $50.0, and the most bearish reporting a price target of just $37.13.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2029, revenues will be $981.1 million, earnings will come to $123.2 million, and it would be trading on a PE ratio of 36.5x, assuming you use a discount rate of 8.6%.

- Given the current share price of $38.94, the analyst price target of $50.0 is 22.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on NetScout Systems?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.