Last Update 29 Apr 26

Fair value Decreased 17%BYIT: Flat 2027 Profit Guidance And Cost Reset Will Underpin Extended Recovery Timeline

Analysts have trimmed their price target on Bytes Technology Group, cutting fair value by roughly £0.78 per share as they reset assumptions around discount rates, long term revenue growth, profit margins and future P/E multiples following the latest research updates.

Analyst Commentary

Bullish Takeaways

- Bullish analysts still see scope for value creation if Bytes Technology Group can deliver consistent execution against revised growth and margin assumptions that now feed into a lower fair value range.

- The reset in discount rates and long term revenue growth expectations is viewed by some as a cleaner starting point for future forecasts, which can reduce the risk of further sharp valuation adjustments if conditions remain broadly similar.

- Supportive views highlight that a lower assumed future P/E multiple can leave room for upside if the company achieves steady earnings delivery relative to the new, more conservative benchmarks.

- Some bullish analysts argue that expectations embedded in the latest research updates now better reflect execution risk, which can make the risk or reward trade off more balanced for long term holders.

Bearish Takeaways

- Bearish analysts focus on the reduced fair value per share, which reflects concern that previous assumptions on growth, profitability and valuation multiples were too optimistic relative to the latest information.

- The downgrade referenced in recent research captures caution around Bytes Technology Group’s ability to sustain prior revenue and margin profiles, a shift that feeds into lower earnings power in analysts’ models.

- There is also unease that the company could face pressure to justify even the revised P/E assumptions, particularly if execution slips or if end market demand does not support prior volume expectations.

- Some bearish analysts flag that the combination of higher discount rates and moderated long term growth leaves less room for error, which can keep a cap on valuation until there is clearer evidence on delivery against these updated forecasts.

What's in the News

- Bytes Technology Group issued earnings guidance for 2027, indicating operating profit is expected to be broadly flat. (Key Developments)

- The group plans to absorb about £4.5m of cost normalisation in 2027, tied to higher technology costs after completing major projects and a return to regular bonus levels. (Key Developments)

- Guidance also factors in continued headcount investment for growth, which is included in the cost base the company expects to carry while keeping operating profit broadly flat. (Key Developments)

Valuation Changes

- Fair value reduced from £4.59 to £3.81 per share, a cut of around 17%.

- Discount rate adjusted slightly from 8.89% to 8.86%.

- Revenue growth now assumed at 7.69% versus 7.49% previously, a small uplift in top line expectations.

- Profit margin nudged up from 22.00% to 22.50% in the revised model.

- Future P/E moved down from 23.0x to 19.0x, implying a lower valuation multiple applied to earnings.

Key Takeaways

- Strategic investment in AI and cloud technologies positions Bytes Technology Group for significant revenue growth as demand increases.

- Expansion in cybersecurity offerings aims to capture market share, benefiting from higher-margin services to enhance net margins.

- Economic uncertainty and reliance on low-margin public contracts pressure net margins, while strategic alignment on Microsoft priorities and upselling are critical for future growth.

Catalysts

About Bytes Technology Group- Offers software, IT security, hardware, and cloud services in the United Kingdom, rest of Europe, and internationally.

- Bytes Technology Group's investment in new enterprise-grade systems and office environments is set to support future growth. This can lead to increased operational efficiency and the ability to scale, potentially boosting earnings.

- The expansion of their cloud base in public and corporate sectors and strategic focus on AI-powered software products suggests potential for significant revenue growth as demand for these technologies increases.

- Continued investment in cybersecurity offerings and expertise positions the company to capture a larger portion of the cybersecurity market, which can enhance net margins due to the higher-margin profile of cybersecurity services.

- Hiring more technical and sales staff aligns with the company's growth strategy and can drive future revenue growth by increasing sales capacity and improving the quality of customer service and technical support.

- Development of a customer-facing marketplace portal and internal order processing platform is expected to launch by the second half of FY '26, which could simplify transactions, improve user experience, and boost revenue by facilitating access to a broader range of products.

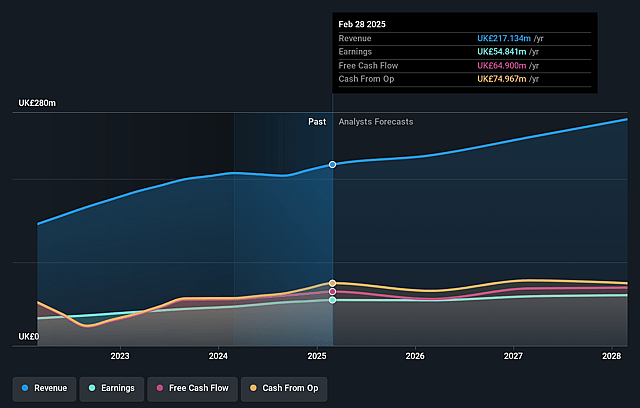

Bytes Technology Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Bytes Technology Group's revenue will grow by 7.7% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 24.3% today to 22.5% in 3 years time.

- Analysts expect earnings to reach £61.7 million (and earnings per share of £0.25) by about April 2029, up from £53.4 million today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 19.0x on those 2029 earnings, up from 13.4x today. This future PE is lower than the current PE for the GB Software industry at 28.6x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.86%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The recent snap general election in the U.K. has brought about economic and political uncertainty, which may result in more cautious decision-making and delayed investment by corporate customers, potentially impacting future revenue growth.

- A shift in product sales focus towards public sector contracts, which are often won at lower margins, has been observed. This could pressure net margins if not offset by sufficient volume or higher-margin services.

- The reliance on growth from technical headcount and regional office expansions presents execution risk. If these investments do not translate into increased revenues and earnings, they may affect profitability and net margins.

- The changes in Microsoft's vendor rebate programs require adaptation and alignment with strategic priorities such as Azure, security, and AI. Misalignment or failure to capitalize on these priorities could impact Bytes' future gross profit from Microsoft rebates.

- A significant portion of Bytes' gross profit relies on renewals and upselling to existing public sector contracts. Any slowdown in these extensions or upselling opportunities could affect revenue momentum and overall financial performance.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of £3.81 for Bytes Technology Group based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £4.7, and the most bearish reporting a price target of just £2.56.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be £274.5 million, earnings will come to £61.7 million, and it would be trading on a PE ratio of 19.0x, assuming you use a discount rate of 8.9%.

- Given the current share price of £3.02, the analyst price target of £3.81 is 20.7% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Bytes Technology Group?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.