Last Update 25 Jun 26

Fair value Decreased 3.37%PDD: Heavy Supply Chain And Brand Investments Will Drive Long-Term Upside

The analyst price target for PDD Holdings has been revised lower to reflect a fair value estimate of $115.81, reduced from $119.85, as analysts factor in weaker sector sentiment, recent earnings disappointments, and increased regulatory and investment uncertainties highlighted in recent research.

Analyst Commentary

Recent research on PDD Holdings has turned more cautious, with several firms revising ratings and price targets lower while reassessing the company’s execution, investment plans, and regulatory exposure. The discussion now centers on how PDD balances long term ecosystem investments with nearer term earnings visibility and valuation support.

Bullish Takeaways

- Bullish analysts see current valuation as increasingly attractive after the pullback, with some describing it as compelling even as they acknowledge recent earnings disappointments.

- Several reports highlight that PDD Holdings is prioritizing ecosystem health, supply chain investment, and first party brand development, which, if executed well, could support product quality and long term growth in both domestic and Temu related businesses.

- Some bullish analysts agree with PDD’s decision to keep investing in merchant subsidies and infrastructure, arguing that this could strengthen the platform’s competitiveness even though it weighs on near term profitability.

- Where price targets remain above the revised fair value estimate, the spread reflects confidence that PDD can eventually translate its current investment cycle into sustainable monetization, provided execution stays on track.

Bearish Takeaways

- Bearish analysts point to recent Q1 results, including a Q1 revenue miss, lower non GAAP net margin and what some describe as mediocre outcomes, as signs that PDD Holdings is facing pressure on monetization and earnings quality.

- Several reports cite decelerating China revenue and weaker order related metrics, alongside comments that key events like the 2026 6.18 shopping festival were a negative surprise, which they see as evidence of softer consumer demand in e commerce.

- There is concern that PDD’s increased supply chain spending, merchant subsidies, and push into private label products could cap near term earnings and create friction with merchants, limiting the company’s flexibility to improve margins quickly.

- Bearish analysts also flag a tougher macro backdrop, tightening regulations, and scaled back national trade in support in China as constraints on sector growth, which in their view justifies lower price targets and more neutral or cautious ratings on the stock.

What’s in the News for PDD Holdings

- PDD Holdings reported Q1 2026 results with revenue up 11% year over year and operating profit up 22%, but net income attributable to shareholders fell about 15% versus the prior year and earnings missed analyst estimates, triggering an initial share price drop of nearly 11% and further weakness in subsequent days (source: Q1 2026 earnings coverage).

- Management outlined a large investment plan for brand development and supply chain expansion, including an initial RMB 15b cash injection into a new first party brand business and a planned RMB 100b spend over three years on rural logistics, agricultural and industrial hubs, and ecosystem partnerships in China’s mature e commerce market (source: Q1 2026 earnings coverage).

- Temu, PDD Holdings’ international platform, was fined €200m by the European Commission for selling unsafe products and failing to prevent the spread of illegal items, with Temu required to submit a corrective action plan, while PDD also faces a CNY 3.6b fine from Chinese authorities, ongoing European Commission investigations, and U.S. state level litigation tied to Temu (sources: regulatory coverage, EU fine reports).

- On June 15–16, 2026, BNP Paribas initiated coverage on PDD Holdings with an Underperform rating and a US$89.00 price target, citing complex global and domestic regulatory challenges, rising operational costs, aggressive investment, and the decision not to pursue a more aggressive shareholder return strategy, alongside revised revenue and profit forecasts from Bank of America and a recent 3.17% share price decline (source: BNP Paribas initiation reports).

- PDD Holdings set up a wholly owned tech subsidiary, Pinduoduo Information Technology Services (Xiong'an) Co., Ltd., in Xiong'an New Area with an initial RMB 500m investment, focusing on big data processing, digital operations and maintenance, and cloud platform services, and launched a recruitment program targeting more than 5,000 hires, with about 150 employees already onboarded and an average hiring pace near 30 people per working day (source: Xiong'an subsidiary announcements).

Valuation Changes for PDD Holdings

- Fair Value: Revised lower from $119.85 to $115.81, a reduction of about 3.4% in the updated model for PDD Holdings.

- Discount Rate: Adjusted slightly higher from 9.36% to 9.37%, which implies a modestly higher required return in the valuation framework.

- CN¥ Revenue Growth: Trimmed marginally from 10.15% to 10.11%, which reflects a small change in the assumed growth rate for PDD Holdings.

- CN¥ Net Profit Margin: Eased from 22.93% to 22.82%, which indicates a slightly lower profitability assumption in the latest update.

- Future P/E: Moved down from 11.16x to 10.91x, which suggests that the valuation model now applies a somewhat lower earnings multiple to PDD Holdings.

Key Takeaways

- Investments in ecosystem development, supply chain efficiency, and international expansion are diversifying revenue streams and strengthening PDD's ability to capture e-commerce growth globally.

- Focus on affordability, digitalization, and AI-driven operations is enhancing user acquisition, repeat purchases, and long-term margin improvement amid shifting consumer and macroeconomic trends.

- Aggressive investment, rising competition, and early-stage global expansion risk prolonged margin compression and weaker profitability if ecosystem and diversification efforts fail to deliver returns.

Catalysts

About PDD Holdings- A multinational commerce group that owns and operates a portfolio of businesses.

- PDD Holdings' ongoing and substantial ecosystem investments, including fee reductions, logistics upgrades, and targeted support for SME merchants, are positioning the company to capture a larger share of e-commerce growth both in established regions and underserved remote markets; these efforts are likely to drive higher long-term revenue and enhance user acquisition as overall digital adoption accelerates globally.

- The company is leveraging its Consumer-to-Manufacturer (C2M) model and advancements in supply chain/process digitalization to help manufacturers move up the value chain, increase product innovation, and address consumer needs more efficiently; these improvements are expected to support higher gross margins and net margins over time as scaling and cost efficiency gains materialize.

- PDD's commitment to international expansion, particularly through investment in Temu and global supply chain localization, is enabling penetration into new and rapidly growing consumer markets outside China, diversifying revenue streams and enhancing future topline growth potential as emerging market disposable incomes rise.

- Investments in logistics, agritech, and AI-driven operations-such as broader application of smart agriculture technologies and personalized recommendation engines-should reduce operational frictions, lower delivery costs, and drive repeat purchasing behavior, supporting higher conversion rates and improved operational margins in the medium to long term.

- The company's focus on affordability and value-driven consumption, backed by large-scale consumer giveback and discounting programs, aligns with macro trends favoring budget platforms during economic uncertainty, positioning PDD for market share gains, increased customer lifetime value, and resilient long-term revenue growth.

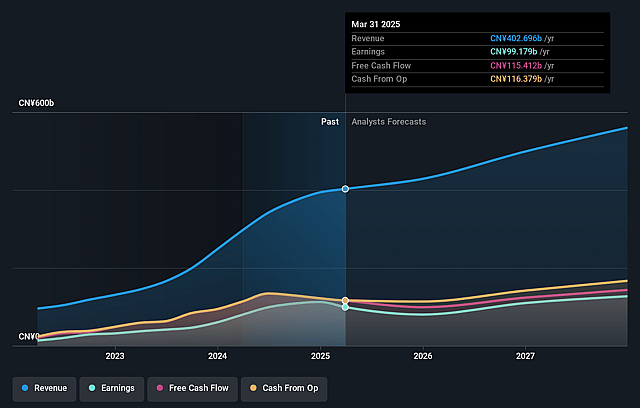

PDD Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming PDD Holdings's revenue will grow by 10.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 21.6% today to 22.8% in 3 years time.

- Analysts expect earnings to reach CN¥134.8 billion (and earnings per share of CN¥93.09) by about June 2029, up from CN¥95.6 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting CN¥176.0 billion in earnings, and the most bearish expecting CN¥89.1 billion.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 10.9x on those 2029 earnings, up from 7.7x today. This future PE is lower than the current PE for the US Multiline Retail industry at 16.9x.

- Analysts expect the number of shares outstanding to grow by 0.5% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.37%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- The company is making historically large, ongoing investments in merchant and consumer support programs (such as the RMB 100 billion support program), which have already resulted in slower revenue growth and a year-over-year decline in operating profit. Management explicitly signals a willingness to sacrifice profit margins for an extended period, increasing the risk of sustained net margin and earnings pressure if investments do not yield the intended ecosystem improvements.

- Competitive intensity is escalating, with both traditional e-commerce players and new content/platform entrants heavily investing in innovation and new business models. As revenue growth slows and PDD's lead over peers narrows, the company may be forced to continually ramp up spending to compete for customers and retain merchants, posing a risk to long-term profitability and revenue growth.

- There is heightened exposure to investment-return mismatch, as management acknowledges a potentially prolonged lag between the timing of heavy ecosystem investments and future financial returns. If these cyclical or structural investments fail to translate into sustainable customer/merchant loyalty or higher monetization, revenue and net income could underperform for an extended period.

- The ongoing pivot towards global expansion and new business lines (such as Duo Duo Grocery), which management admits are at an early stage and require significant, continuing capital outlays, risks either limited revenue diversification or persistent losses abroad. Failure to execute effectively in international markets or inefficient scaling could depress consolidated profit margins and earnings.

- Intensifying industry headwinds such as pricing pressure from subsidies, fee reductions, and commission cuts-implemented as competitive responses-may become entrenched, leading to a structurally lower gross margin environment that could weigh on long-term operating profits and free cash flow generation.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of $115.81 for PDD Holdings based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $169.69, and the most bearish reporting a price target of just $79.79.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be CN¥590.6 billion, earnings will come to CN¥134.8 billion, and it would be trading on a PE ratio of 10.9x, assuming you use a discount rate of 9.4%.

- Given the current share price of $75.74, the analyst price target of $115.81 is 34.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on PDD Holdings?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.