Last Update 24 Jun 26

Fair value Increased 0.13%ULVR: Planned Foods Combination Will Support Future Upside Despite Lowered Price Expectations

Unilever's analyst price target has been revised lower to £37.00 from £43.00, as analysts balance slightly higher long term EPS assumptions with concerns that a valuation in line with U.S. peers may be difficult to justify.

Analyst Commentary

Recent research on Unilever shows a mix of optimism on earnings power and caution around how far the valuation can stretch, especially when compared with large U.S. consumer peers.

Bullish Takeaways

- Bullish analysts are reinstating and upgrading coverage, which signals renewed interest in Unilever's ability to execute on its long term plan.

- Some bullish analysts are comfortable assigning higher ratings even as price targets elsewhere are adjusted, suggesting confidence that execution can support a higher multiple over time.

- Upgrades point to scope for Unilever to improve growth consistency and operating performance, which, if delivered, could support a stronger earnings profile.

- Bullish views generally see room for the company to close part of the gap with U.S. peers if it delivers on growth and profitability initiatives.

Bearish Takeaways

- Bearish analysts have reduced price targets to £37.00 and 3,700 GBp, questioning whether a valuation similar to U.S. consumer stocks is justified at current execution levels.

- Even with EPS assumptions for FY26 to FY28 raised by about 3%, some remain cautious that earnings upgrades alone may not support U.S. peer level valuations.

- Lowered targets highlight concern that investors might be paying too much upfront for expected improvement in growth and margins if delivery is slower than hoped.

- The split between upgrades and target cuts underlines uncertainty over how much of Unilever's potential earnings improvement is already reflected in the share price.

What’s in the News for Unilever

- Unilever plans a new Global Innovation Center in New Haven, Connecticut, focused on personal care, beauty and wellbeing R&D. The center will use AI and emerging quantum capabilities, employ around 300 people, and involve a long-term investment of $270 million, including $50 million in capital expenditure. (Company announcement, Wall Street Journal)

- The New Haven hub is set to become Unilever’s global center for skin care and cleansing and will consolidate formulation, fragrance creation, packaging design and consumer insights under one roof. The aim is to speed up development of new beauty and personal care products. (Company announcement)

- Unilever partnered with Accenture to scale AI enabled digital twins across more than 40 factories over the next 18 months. Existing deployments already support lower waste, energy consumption and quality defects at sites in the US, India, Poland and Vietnam. (Company announcement)

- Dove Men+Care, part of Unilever’s personal care portfolio, launched a global “Care for Your Skin Like You Care for the Game” campaign as an Official Sponsor of the FIFA World Cup 2026. The campaign ties product marketing to fan rituals, ticket promotions and on the ground activations in key host cities. (Company announcement)

- Unilever announced plans to combine its Foods business with McCormick in a Reverse Morris Trust transaction. Under the proposed structure, Unilever and its shareholders are expected to hold 65% of the combined company and Unilever would receive $15.7 billion in cash, as part of a move that would leave Unilever focused on Beauty, Wellbeing, Personal Care and Home Care. (Company announcement)

Valuation Changes for Unilever

- Fair Value, £51.08 updated to £51.15, a very small upward adjustment to the modelled estimate.

- Discount Rate, 8.11% updated to 8.11%, reflecting a minimal recalibration of the implied risk level applied to Unilever.

- Revenue Growth, 3.07% updated to 3.07%, with the projected growth rate essentially unchanged in the latest assumptions.

- Net Profit Margin, 13.14% updated to 13.14%, indicating only a fractional tweak to the long term profitability outlook.

- Future P/E, 22.41x updated to 22.48x, a slight increase in the multiple assumed for Unilever’s earnings further out.

Key Takeaways

- Shifting focus to premium, science-led products and divesting non-core brands is streamlining operations, boosting margins, and enhancing long-term profitability.

- Emphasis on digital expansion, emerging markets, and brand investment is fueling sustained revenue growth and stronger competitive positioning.

- Intensifying competition, regional underperformance, input cost pressures, portfolio streamlining, and elevated regulatory scrutiny threaten sustainable revenue growth, margin expansion, and brand stability.

Catalysts

About Unilever- Operates as a fast-moving consumer goods company in the Asia Pacific, Africa, the Americas, and Europe.

- Acceleration of volume growth in key emerging markets (India, China, Indonesia), supported by rising disposable incomes, urbanization, and rapid expansion in digital/e-commerce channels, is expected to drive sustained top-line revenue growth as these markets recover and Unilever gains market share.

- Portfolio transformation with a sharper focus on premium and science-led Personal Care and Beauty & Wellbeing products, coupled with bolt-on acquisitions of fast-growing digitally native brands, is increasing exposure to higher-margin categories and supporting long-term margin and earnings expansion.

- Strategic divestitures, including the demerger of Ice Cream and continued disposal of non-core food brands, are simplifying the business model and structurally raising the gross and operating margin profile of the remaining company, directly improving profitability and ROIC.

- Improved productivity via supply chain digitization, procurement efficiencies, and disciplined cost management (targeted cost savings of €650 million in 2025) are enhancing gross margins, providing additional fuel for competitive brand investment, and supporting higher sustainable earnings growth.

- Increased investment in brand marketing (15–16% of revenue, notably in Power Brands and digital commerce) is driving innovation, strengthening brand equity, and enabling Unilever to better capture evolving consumer demand in wellness, health, and premiumization, likely resulting in higher revenue growth and maintained or expanded market share.

Unilever Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- Analysts are assuming Unilever's revenue will grow by 3.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 11.3% today to 13.1% in 3 years time.

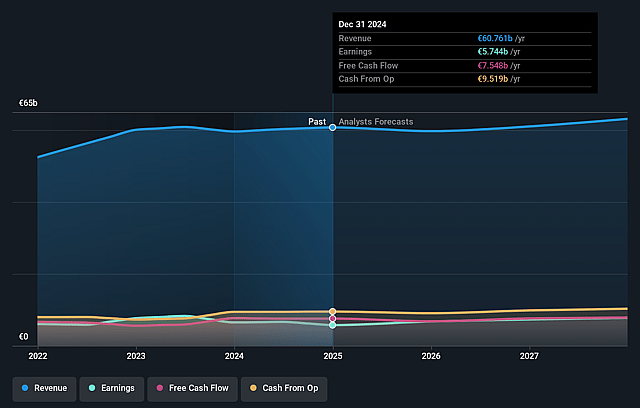

- Analysts expect earnings to reach €7.3 billion (and earnings per share of €3.41) by about June 2029, up from €5.7 billion today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 22.5x on those 2029 earnings, up from 19.7x today. This future PE is greater than the current PE for the US Personal Products industry at 15.7x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.11%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Intensifying competition from private label and local/niche brands-especially in personal care and food-in key markets like the US and Europe threatens Unilever's long-term pricing power and could erode market share, undermining revenue growth and margin expansion.

- Weak emerging market performance, particularly chronic volume declines in Latin America and flat or negative trends in China and Indonesia, exposes the company to ongoing regional underperformance, creating persistent drag on group revenue and structural headwinds for growth.

- Ongoing input cost inflation (commodities, packaging, transport) and adverse currency movements, especially pronounced in 2025, have pressured operating margins and led to reliance on price increases that may not be sustainable, risking future profitability and earnings.

- The company's continuing portfolio rationalization-including divestitures like the Ice Cream unit and underperforming food brands-could reduce overall scale benefits and increase business concentration, potentially leading to revenue volatility, reduced diversification, and uneven margin trajectory if not offset by sufficient growth in premium categories.

- Heightened regulatory, environmental, and consumer scrutiny around sustainability, ingredient transparency, and global tax regimes-increasing compliance costs and reputational risks-may constrain long-term margin improvement and require ongoing heavy investment to maintain brand equity and customer trust.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of £51.15 for Unilever based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £58.95, and the most bearish reporting a price target of just £37.03.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be €55.3 billion, earnings will come to €7.3 billion, and it would be trading on a PE ratio of 22.5x, assuming you use a discount rate of 8.1%.

- Given the current share price of £44.53, the analyst price target of £51.15 is 12.9% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Unilever?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.