Last Update 03 May 26

Fair value Decreased 0.37%GQG: Softer Outlook As Fund Outflows And Margins Reshape Future P/E Expectations

Analysts have trimmed their price target on GQG Partners to A$1.85, reflecting updated views on softer revenue growth, lower profit margins, and a higher expected future P/E following recent fund outflows and weaker fund performance.

Analyst Commentary

Recent Street research points to a more cautious stance on GQG Partners, with bearish analysts flagging concerns around fund flows, recent fund performance, and what that could mean for valuation and execution risk.

A key move has been the downgrade to Neutral from Buy at Goldman Sachs, paired with a revised A$1.85 price target. This ties directly to concerns about accelerating outflows and weaker recent returns in the underlying funds.

Bearish Takeaways

- The shift to a Neutral rating indicates that bearish analysts see a more balanced risk or reward profile. They express less confidence that current pricing sufficiently reflects pressures from recent fund outflows.

- The A$1.85 price target reflects assumptions about softer revenue growth and lower profit margins, raising questions about how efficiently GQG Partners can convert its asset base into earnings.

- Reference to accelerating outflows and weaker fund performance highlights execution risk, as it suggests challenges in retaining and attracting client capital at a pace needed to support earlier expectations.

- The expectation of a higher future P/E multiple relative to more stable peers indicates that bearish analysts see elevated valuation risk if fund performance and flows do not stabilise.

For investors, the consistent message across these research updates is that GQG Partners is perceived as carrying more visible execution and growth risk than previously assumed, with the stock price and target of A$1.85 being reassessed in that context.

What's in the News

- The Board of Directors declared a fourth-quarter 2025 dividend of US$0.0365 per share, stated as 90% of fourth-quarter distributable earnings (Key Developments).

- The ex-dividend date for the fourth-quarter 2025 dividend is 18 February 2026, setting the cutoff for eligibility (Key Developments).

- The record date for shareholders to qualify for the fourth-quarter 2025 dividend is 19 February 2026 (Key Developments).

- The payment date for the fourth-quarter 2025 dividend is scheduled for 26 March 2026, when eligible shareholders are due to receive cash distributions (Key Developments).

Valuation Changes

- Fair Value: A$1.55 has been adjusted slightly to A$1.54, indicating a small downward revision in the modelled intrinsic value per share.

- Discount Rate: The rate has edged down from 7.87% to 7.85%, a modest change that slightly alters the present value of future cash flows.

- Revenue Growth: The long term revenue growth assumption has shifted from an 8.14% decline to a 9.03% decline, indicating a more cautious view on future revenue trends.

- Net Profit Margin: The margin assumption has eased from 52.59% to 51.94%, reflecting a small reduction in expected earnings efficiency on each dollar of revenue.

- Future P/E: The assumed future P/E multiple has moved from 12.28x to 13.07x, indicating that investors are expected to pay a slightly higher multiple for GQG Partners earnings than previously modelled.

Key Takeaways

- Fee and revenue growth are threatened by shifts toward passive investing, regulatory pressures, and technological disruption reducing the appeal of active management.

- Heavy reliance on a key leader and concentration in few strategies heighten business risks and potential for client outflows affecting future earnings.

- Strong global client demand, scalable expansion into new channels, and disciplined financial management position GQG Partners for sustainable growth, resilient revenue, and robust shareholder returns.

Catalysts

About GQG Partners- Operates as a boutique asset management company worldwide.

- Accelerating adoption of passive investing and exchange-traded funds is likely to erode demand for active management and continue to put downward pressure on management fees, which currently account for over ninety-six percent of GQG's net revenue. This structural shift is expected to constrain both revenue growth and net margins going forward.

- Intensifying regulatory scrutiny and the resulting increase in global compliance costs threaten to reduce GQG's operating leverage and hamper its ability to expand profitably, ultimately impacting long-term earnings and margin expansion.

- GQG remains highly reliant on the reputation and continued presence of its key investment leader, Rajiv Jain, which represents a significant succession risk. Any change or departure could quickly drive client outflows, reduce assets under management, and sharply compress future fee-based revenues.

- The firm's focus on only a handful of core investment strategies creates a vulnerability such that sustained underperformance in any flagship product could prompt outsized client redemptions. This amplifies instability in both assets under management and future fee income, threatening overall earnings power.

- Growing technological disruption, particularly from robo-advisors and algorithmically driven portfolio solutions, is expected to further disintermediate traditional active managers. As a result, GQG's addressable market is poised to shrink, putting continued pressure on future revenue and margin potential.

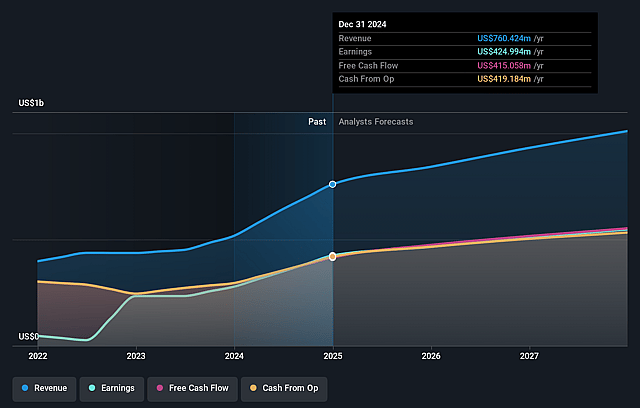

GQG Partners Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on GQG Partners compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming GQG Partners's revenue will decrease by 9.0% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 56.5% today to 51.9% in 3 years time.

- The bearish analysts expect earnings to reach $316.1 million (and earnings per share of $0.11) by about May 2029, down from $457.0 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $523.1 million.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 13.1x on those 2029 earnings, up from 7.8x today. This future PE is lower than the current PE for the AU Capital Markets industry at 18.5x.

- The bearish analysts expect the number of shares outstanding to grow by 0.09% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.85%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- Record growth in funds under management, reaching over $172 billion and driven by $8 billion in net inflows, demonstrates strong client demand and asset growth that can underpin long-term revenue and earnings expansion.

- Persistent long-term outperformance by key strategies, recognized by top quintile Morningstar ratings and risk-adjusted alpha, fortifies GQG's reputation and supports both the retention of client assets and attraction of new mandates, which benefits fee-based revenue stability.

- Expansion into fast-growing channels such as separately managed accounts and active ETFs, accomplished without significant capital investment or increased cost base, opens scalable new growth paths, enhancing operating leverage and future margin expansion.

- Diversified, global distribution and wide institutional and sub-advisory support, including deep relationships with major asset consultants and platforms, provides resilience against isolated outflows and broadens the base for recurring and sticky management fee income.

- Continued investment in operational infrastructure, disciplined expense control yielding high operating margins, and a debt-free balance sheet with strong cash generation and high dividend payout capacity all position the company for robust long-term earnings and shareholder returns.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for GQG Partners is A$1.54, which represents up to two standard deviations below the consensus price target of A$1.9. This valuation is based on what can be assumed as the expectations of GQG Partners's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$2.69, and the most bearish reporting a price target of just A$1.54.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be $608.5 million, earnings will come to $316.1 million, and it would be trading on a PE ratio of 13.1x, assuming you use a discount rate of 7.8%.

- Given the current share price of A$1.67, the analyst price target of A$1.54 is 8.0% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on GQG Partners?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.